Predatory Lending Tactics That Spiked in 2026: What Regulators Are Watching

CFPB complaints tied to deceptive loan terms jumped 34% in 2026, with 12 states now investigating high-cost digital credit products targeting low-income and gig workers.

CFPB complaints tied to deceptive loan terms jumped 34% in 2026, with 12 states now investigating high-cost digital credit products targeting low-income and gig workers.

Debt settlement companies charge 15–25% of enrolled debt, while self-negotiation costs nothing. See which approach fits your situation before you enroll anywhere.

Consumers can sue illegal debt collectors for up to $1,000 under the FDCPA. See how one single mother documented violations, filed complaints, and stopped the harassment.

Learn about arbitration clause loan agreements. Discover what you waive when you sign, how it affects your legal rights, and what borrowers should know.

Learn about credit repair company vs self. Discover when to hire help or DIY dispute errors to save money and fix your credit faster.

Learn about illegal debt collection scripts. Discover what collectors cannot legally say under the FDCPA and how to protect your consumer rights.

BNPL users carry 3.8 active loans on average while payday APRs top 400%—here's how each product traps borrowers differently and which poses the greater danger.

Learn about Military Lending Act fees. See how one veteran recovered $900 in illegal loan charges and how you can fight back against predatory lenders.

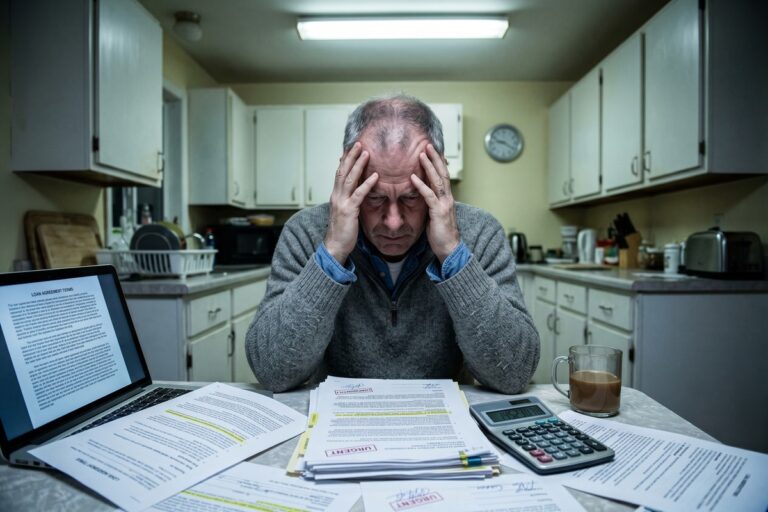

Seniors lose over $3 billion annually to financial exploitation. Here's how to recognize payday loan traps, reverse mortgage scams, and equity-stripping schemes before they strike.

The CFPB gets a lender response in 15 days; your State AG takes 30–90 but hits harder on fraud. Here's when to use each — and when to file both at once.