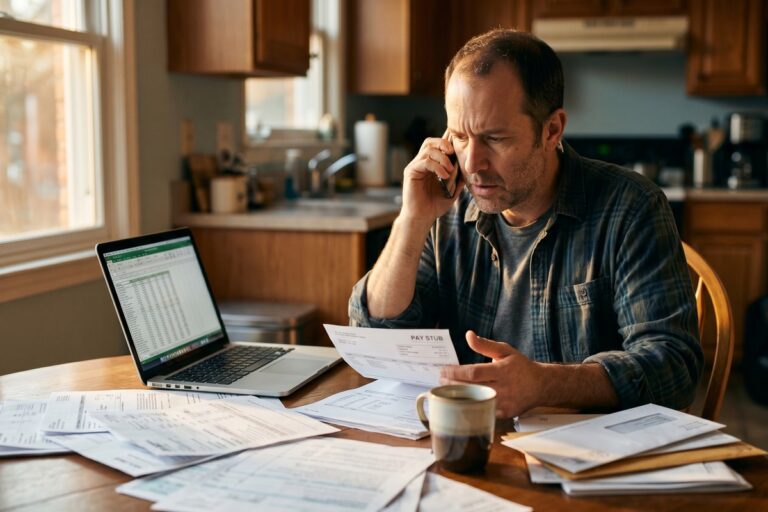

Payday Loan Debt Traps: Warning Signs Most Borrowers Miss Until It’s Too Late

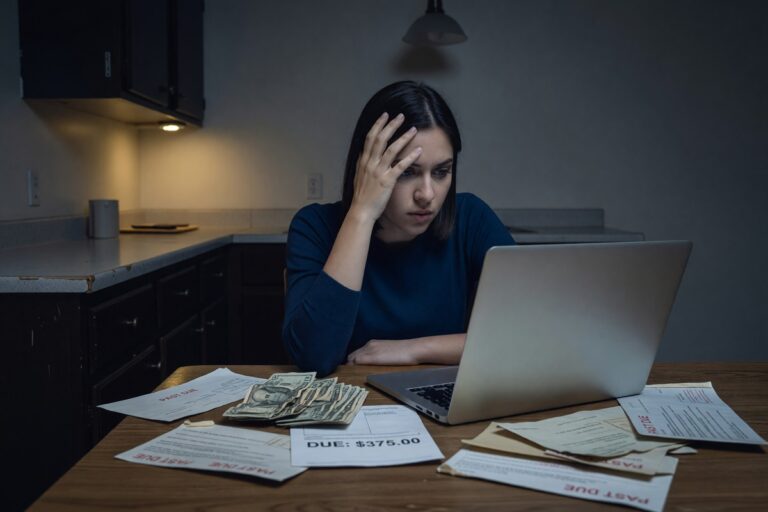

80% of payday loans are re-borrowed within 14 days, per CFPB data. Here are the warning signs that separate a one-time fix from a fee cycle lasting months.

80% of payday loans are re-borrowed within 14 days, per CFPB data. Here are the warning signs that separate a one-time fix from a fee cycle lasting months.

Learn about hidden loan fees. Discover the sneaky charges lenders bury in contracts—and how to spot them before they cost you hundreds.

Learn about mandatory arbitration clause loan agreements. Discover what rights you waive, hidden risks, and how to protect yourself before signing.

51.9 million immigrants live in the U.S., yet few know the ECOA and FDCPA protect all borrowers regardless of status. Here's how those rights actually work.

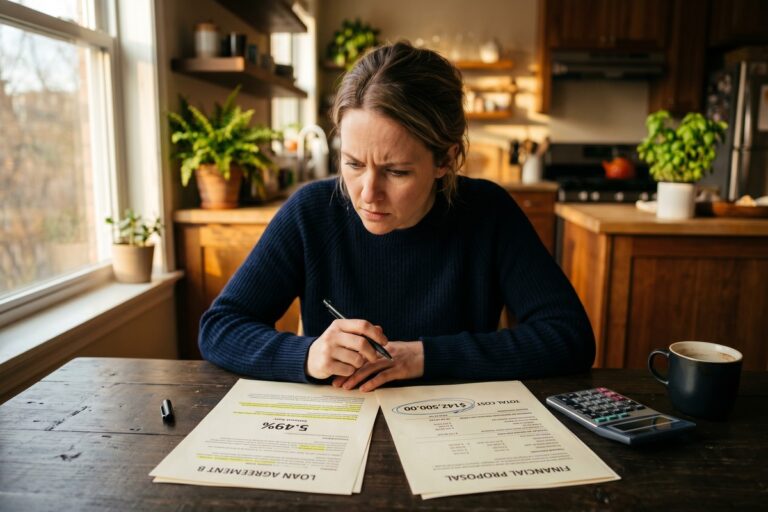

Learn about APR vs total loan cost. Discover why APR alone can mislead borrowers and how comparing the full cost of a loan could save you hundreds.

Federal law caps garnishment at 25% of disposable earnings, but borrowers who engage the legal process early can often reduce or eliminate that amount entirely.

Learn about debt collector harassment. Discover what tactics are illegal under the FDCPA and how to stop abusive collectors from violating your rights.

APRs above 400%, hidden fees, and mandatory arbitration clauses are among the five predatory loan red flags the CFPB warns borrowers to check before signing.

Banks have refunded over $6 billion in overdraft fees since 2022. See how one single mother used a CFPB complaint to get every unlawful charge returned within 60 days.

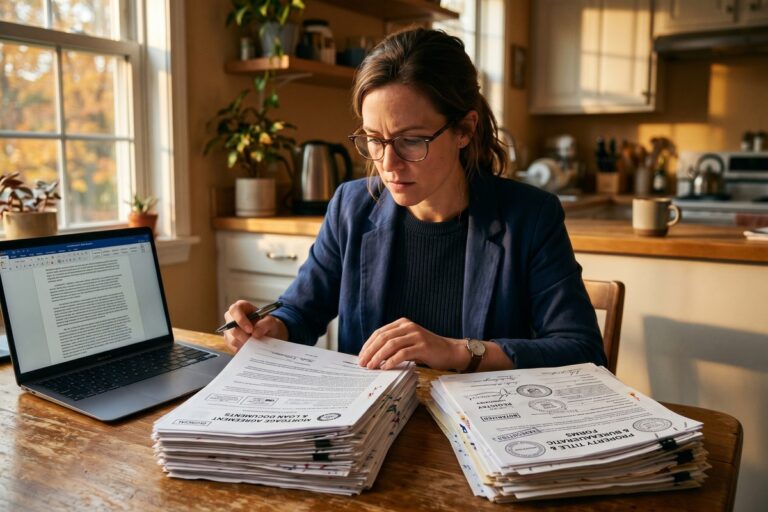

18 states plus D.C. have interest rate caps stricter than federal defaults. Here's how state and federal lending laws stack up—and which ones actually protect you.