Fact-checked by the onlinepaydaynews.com editorial team

Quick Answer

The CFPB complaint process typically generates a company response within 15 days, while State Attorney General offices can take 30–90 days but carry stronger enforcement authority. For fast lender responses, file with the CFPB first. For illegal conduct or systemic fraud, escalate to your State AG simultaneously.

The CFPB complaint process is the fastest route to a documented lender response. The Bureau requires companies to respond within 15 calendar days, according to the CFPB’s official complaint process page. That speed advantage matters when you are dealing with unauthorized charges, debt collection violations, or loan servicing errors on accounts held with large servicers — whether that’s a regional bank, a national lender like Chase, or a fintech like SoFi.

Speed does not always mean resolution, though. State Attorneys General hold independent enforcement power that the CFPB cannot replicate, and knowing which channel to use — or whether to use both — can determine whether your complaint gets a form letter or a refund check.

Key Takeaways

- The CFPB requires companies to respond within 15 calendar days of receiving a complaint, per the CFPB’s official complaint process page.

- The CFPB received over 1.3 million complaints in 2023, with approximately 98% forwarded to the named company for response, per the CFPB 2023 Consumer Response Annual Report.

- State Attorney General offices typically take 30–90 days for an initial response, but can pursue restitution settlements worth millions of dollars through direct litigation.

- Companies have a 60-day window to provide a final resolution through the CFPB complaint process; consumers who dispute an inadequate response within that window see higher rates of monetary relief.

- State AGs hold jurisdiction over lenders the CFPB cannot directly supervise, including certain payday lenders, auto dealers, and unlicensed operators that function primarily within state borders.

- Filing with both the CFPB and your State AG simultaneously is permitted, costs nothing, and creates parallel records under federal and state law — which is often the strongest approach when fraud or deception is involved.

How Does the CFPB Complaint Process Actually Work?

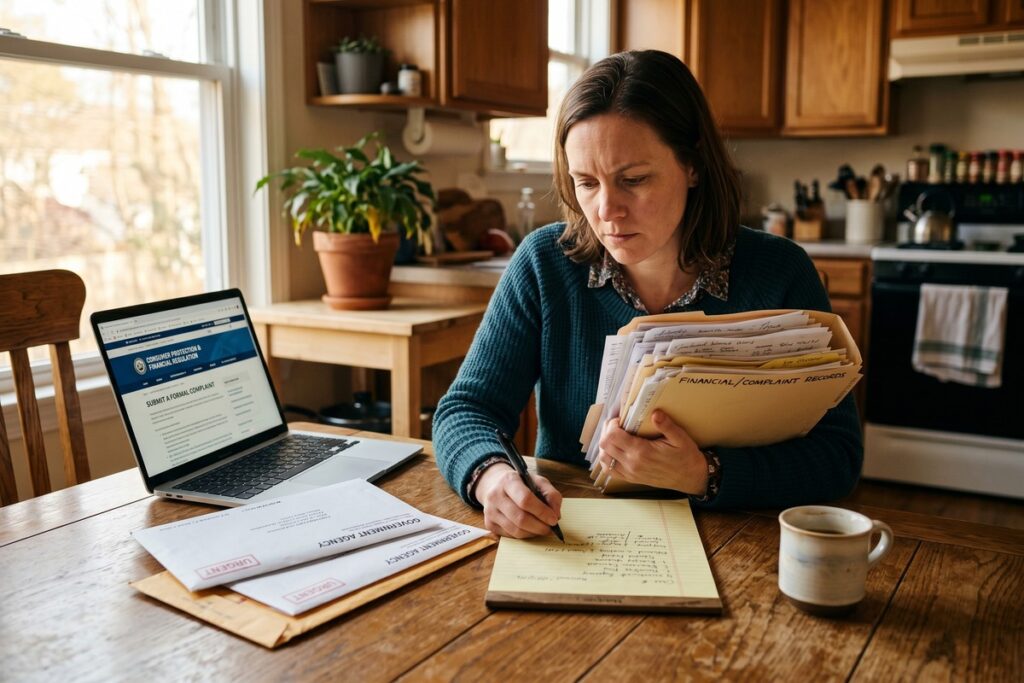

The CFPB complaint process is a structured, federal intake system that routes consumer complaints directly to regulated financial companies and requires a documented response. Consumers file online at ConsumerFinance.gov, and the company receives the complaint through a secure portal within days.

Once submitted, the company has 15 days to respond and 60 days to provide a final resolution. The CFPB publishes most responses in its Consumer Complaint Database, which creates public accountability pressure that many companies take seriously. This transparency factor accelerates lender responses compared to private dispute channels, because a poorly handled complaint becomes a permanent public record.

The CFPB covers a wide range of financial products: mortgages, credit cards, student loans, payday loans, debt collection, and credit reporting. That includes disputes over APR disclosures, FICO Score reporting errors on files maintained by bureaus like Experian, and unauthorized loan fees. If you have experienced illegal auto-renewal charges or unexpected loan fees, read how a gig worker successfully fought an illegal auto-renewal loan charge using similar consumer protection tools.

What the CFPB Cannot Do

The CFPB cannot represent you individually, award damages, or compel a company to accept your position. It facilitates and documents. Enforcement actions come separately, often months or years later, and frequently involve coordination with the Federal Trade Commission (FTC), the Federal Reserve, or the FDIC depending on what type of institution is under scrutiny. For immediate legal remedies, the State AG channel becomes critical.

Key Takeaway: The CFPB complaint process requires companies to respond within 15 days, with a final resolution due in 60 days. See the CFPB’s complaint timeline — this structured accountability is the Bureau’s primary advantage over informal dispute channels.

How Do State Attorney General Complaints Work?

State Attorney General offices accept consumer complaints and have independent authority to investigate, litigate, and impose civil penalties under state law. Unlike the CFPB, State AGs can file lawsuits, seek injunctions, and negotiate restitution agreements that directly return money to affected consumers.

Response timelines vary significantly by state. Smaller AG offices may take 30–90 days just to acknowledge a complaint, and full investigations can span 6–18 months. When a State AG does act, though, the outcomes are often larger in scale: multi-million dollar settlements with industry-wide implications, not just a single account adjustment.

State AGs also hold jurisdiction over lenders that operate primarily within state borders and may fall outside direct CFPB supervision. This includes certain payday lenders, rent-to-own companies, and auto dealers. If you suspect predatory versus fair lending practices, a State AG complaint creates a formal legal record that supports future litigation and can attract attention from other affected consumers who have filed similar grievances.

According to the National Association of Attorneys General, every state maintains a consumer protection division. Some, particularly in states with strong AG offices like California, New York, and Illinois, operate dedicated financial fraud units that coordinate directly with federal regulators, including the CFPB and the FTC.

Rather than attributing enforcement philosophy to any single official, the practical reality is this: state consumer protection statutes often go further than federal law. A lender charging an APR that violates a state rate cap may face no direct CFPB action if the Bureau lacks jurisdiction — but a State AG can sue under state statute, seek civil penalties, and demand borrower restitution in the same proceeding.

Key Takeaway: State AG complaints take 30–90 days for initial response but can yield restitution settlements worth millions. The National Association of Attorneys General directory connects consumers to their state office quickly — file there alongside any CFPB action for maximum leverage.

Which Gets Faster Results: CFPB or State AG?

For speed of initial response, the CFPB complaint process wins clearly: a mandatory 15-day company response versus weeks or months through a State AG office. For depth of outcome and enforcement power, the State AG wins in most scenarios involving fraud, deception, or systemic abuse.

| Factor | CFPB Complaint Process | State Attorney General |

|---|---|---|

| Initial Response Time | 15 days (mandatory) | 30–90 days (varies by state) |

| Final Resolution Window | 60 days | 6–18 months for investigations |

| Enforcement Authority | Federal; can refer for action | State law; can sue directly |

| Public Accountability | Complaint published in database | Case-by-case; press releases |

| Monetary Restitution | Indirect via enforcement actions | Direct via settlements |

| Best For | Individual billing errors, servicer disputes | Fraud, deceptive practices, systemic abuse |

| Filing Cost | Free | Free |

The most effective strategy is parallel filing. Submit your CFPB complaint first — it triggers the fastest documented response. Then file with your State AG to create an independent legal record. According to the CFPB’s 2023 Consumer Response Annual Report, the Bureau received over 1.3 million complaints in 2023, with approximately 98% of complaints sent to companies for response — demonstrating the system’s near-universal reach.

Before you file, review the 5 mistakes borrowers make when filing a CFPB complaint to avoid common errors that delay resolution or weaken your case.

Key Takeaway: Filing with both agencies simultaneously is the strongest approach. The CFPB generated over 1.3 million complaints in 2023 with a 98% send-to-company rate, per the CFPB 2023 Annual Report — making it the highest-volume consumer complaint channel in the U.S.

What Does the Data Show About Complaint Outcomes?

Volume alone does not tell the whole story. The CFPB’s Consumer Complaint Database shows clear patterns in which complaint types produce monetary relief versus closed explanations.

Credit reporting and debt collection complaints dominate the database by volume — and they also show the highest rates of consumers receiving some form of monetary relief when they follow up actively. Complaints involving Experian, for example, frequently involve disputed tradelines, outdated derogatory marks, or mixed-file errors that affect a borrower’s FICO Score and, in turn, their access to credit at reasonable APR terms.

Mortgage servicing complaints tell a different story. Large servicers, including units of institutions supervised by the Federal Reserve and the FDIC, often respond to CFPB complaints with form-letter explanations rather than substantive corrections. That is where State AG pressure adds real weight. Several state AG offices have negotiated mortgage servicing consent orders that produced direct borrower restitution, something the CFPB complaint process alone rarely achieves for individual filers.

How Complaint Volume Affects Company Behavior

Companies that accumulate high complaint volumes in the CFPB database face a form of reputational risk that shapes their internal dispute resolution behavior. Publicly traded lenders and fintechs, including companies like SoFi, are aware that complaint trends appear in investor-facing regulatory filings and press coverage. That creates a structural incentive to resolve complaints before they become patterns.

Smaller lenders, particularly unlicensed or loosely regulated operators in the payday lending space, face less market pressure from CFPB database exposure. For those lenders, State AG enforcement is often the only mechanism with real teeth — because a lawsuit carries consequences that a public database entry does not.

When Should You Use Each Channel?

Use the CFPB complaint process when you need a fast, documented company response for issues like incorrect credit reporting, unauthorized fees, or debt collection harassment. Use your State AG when conduct appears criminal, deceptive, or part of a pattern affecting multiple consumers.

Debt collection violations are a strong use case for both channels simultaneously. If a collector is calling your workplace or making threats, the Fair Debt Collection Practices Act (FDCPA) provides federal protection, and both the CFPB and the Federal Trade Commission (FTC) take these complaints. Understand exactly what is and is not allowed by reading about debt collector workplace call rules and your legal rights.

Situations That Warrant State AG Priority

- A lender is operating without a state license

- A company has violated state-specific interest rate caps

- Deceptive advertising or contract terms are involved

- You have evidence that multiple consumers are affected

- The lender falls outside CFPB jurisdiction (e.g., certain auto dealers)

Payday loan borrowers should also check their state’s specific rollover rules. Violations of payday loan rollover disclosure requirements are a direct trigger for State AG complaints, since these rules are typically state-law obligations, not federal ones.

Key Takeaway: The CFPB handles billing errors fastest — within 60 days total. State AGs are better suited for fraud and state-law violations. The FTC Bureau of Consumer Protection is a third option worth filing with when deceptive marketing is involved.

How the CFPB and State AGs Coordinate on Financial Enforcement

These two channels do not operate in silos. The CFPB and State AG offices frequently share complaint data, particularly when complaint patterns suggest systemic violations rather than isolated disputes. That coordination matters for consumers because a complaint filed at one level can inform enforcement activity at the other.

Under the Dodd-Frank Act, State AGs have express authority to enforce certain federal consumer financial laws, including provisions the CFPB itself enforces. This means a State AG can bring a federal CFPB-statute claim without waiting for the Bureau to act. In practice, multi-state coalitions of AGs have pursued actions against mortgage servicers, for-profit education lenders, and payday loan operators — coordinating enforcement timelines and settlement terms across dozens of states simultaneously.

The FDIC and the Federal Reserve separately supervise depository institutions — commercial banks, savings associations, and their subsidiaries. When a complaint involves a nationally chartered bank, CFPB jurisdiction is direct. For state-chartered institutions supervised by the FDIC or the Federal Reserve, the regulatory picture is more complex, and a State AG complaint may reach the responsible supervisor more efficiently than the CFPB channel alone.

When the FTC Steps In

The FTC is a separate federal consumer protection authority with jurisdiction over deceptive and unfair business practices across many industries. In financial services, the FTC focuses on debt collectors, credit repair organizations, and lenders that engage in deceptive advertising — for instance, misrepresenting a loan’s true APR or burying fee disclosures in fine print. Filing with the FTC Bureau of Consumer Protection adds a third institutional record to your complaint, which is worth doing if deceptive marketing practices are central to your dispute.

How Complaints Intersect with Credit Reporting and DTI Calculations

One underappreciated reason to file quickly is the effect an unresolved dispute can have on your credit profile. A servicer error that goes unchallenged can result in a derogatory mark on your credit report that lowers your FICO Score, raises your effective APR on future credit applications, and distorts your debt-to-income (DTI) ratio by inflating reported balances.

Filing a CFPB complaint creates a timestamped record that a dispute was raised. That record can support a separate credit bureau dispute with Experian, Equifax, or TransUnion under the Fair Credit Reporting Act (FCRA). The two processes are independent but reinforce each other: CFPB complaint data identifies the originating lender’s error, while the FCRA dispute targets the bureau’s tradeline directly.

If your DTI has been artificially inflated by a reporting error — say, a balance shown as delinquent that was actually paid — the practical cost is real. Lenders use DTI thresholds to approve mortgages, auto loans, and personal credit lines. An error that pushes your DTI above a lender’s cutoff can cost you a loan approval or force you into a higher APR tier. Resolving that error through a coordinated CFPB complaint and FCRA dispute is the fastest documented path to correction.

How Do You Strengthen Either Complaint for Maximum Impact?

A well-documented complaint dramatically increases your chance of a meaningful response, regardless of which channel you use. Both the CFPB and State AG offices prioritize complaints that include specific dates, dollar amounts, account numbers, and copies of communications.

Keep a paper trail before you file. Save every statement, email, letter, and call log with timestamps. When submitting through the CFPB complaint process, attach supporting documents directly to your submission. Vague complaints citing general dissatisfaction rarely trigger escalated responses. Specificity signals that you are an informed consumer who is not easily dismissed.

After filing, monitor your CFPB complaint status through your online account portal. If the company’s response is inadequate, you have 60 days to dispute it directly within the CFPB system. According to CFPB consumer response data, consumers who actively dispute inadequate responses have a meaningfully higher rate of receiving monetary relief than those who do not follow up.

Document the Financial Impact Specifically

Vague harm descriptions (“I was overcharged”) are less effective than precise ones. State the dollar amount at issue, the date the charge appeared, the account number, and the specific fee or rate that you believe was applied in error. If the error affects your FICO Score or your reported DTI, say so and explain how. Regulators and company compliance teams treat financially quantified complaints differently from general grievances — the former requires a specific response, and the latter often gets a template.

For State AG complaints, include any documentation showing that other consumers may be affected. A pattern allegation carries more investigative weight than an isolated claim. If you have found online reviews, court records, or news coverage of similar complaints against the same lender, attach or reference that material. State AG offices look for patterns when deciding which cases to prioritize for formal investigation.

Key Takeaway: Consumers who dispute an inadequate CFPB response within the 60-day window see higher rates of monetary relief, per CFPB complaint database research. Attaching supporting documents at the time of filing is the single most effective step to improve your complaint outcome.

What Should You Expect After You File?

Filing a CFPB complaint does not guarantee a refund, and filing a State AG complaint does not guarantee an investigation. Understanding the realistic sequence of events helps you avoid frustration and keep pressure on the right points.

After a CFPB complaint is submitted, you receive an email confirmation with a tracking number. The named company is notified through the secure portal, typically within one to two business days. Within 15 days, the company submits an initial response — which may be a substantive answer, a request for more time, or a claim that the matter is outside CFPB jurisdiction. You receive a notification and can review the response in your online account.

If the company claims the account is under litigation or arbitration, the CFPB may close the complaint without further action. That is a signal to escalate to your State AG or consult a consumer law attorney. Many FDCPA and FCRA violations carry statutory damages that private attorneys pursue on contingency, meaning no upfront cost to you.

State AG timelines are less predictable. Some offices send an acknowledgment letter within two weeks; others take the full 90 days. If your complaint is selected for investigation, you may be contacted for additional documentation. If it is not, you will usually receive a letter explaining that the office could not take individual action but that your complaint has been recorded for pattern analysis. That outcome feels unsatisfying, but it is not meaningless: AG offices use complaint records to identify which lenders to target in future enforcement sweeps.

Frequently Asked Questions

How long does the CFPB complaint process take to get a response?

Companies must respond to CFPB complaints within 15 calendar days of receiving the complaint, with a final resolution required within 60 days. The CFPB notifies you by email at each stage, and you can track status in your online account.

Does filing a CFPB complaint actually do anything?

Yes. The CFPB complaint process creates a formal record that companies must respond to publicly. The CFPB received over 1.3 million complaints in 2023, and approximately 98% were forwarded to the named company. Many consumers receive account corrections, fee reversals, or written explanations they would not have received otherwise.

Can I file a complaint with both the CFPB and my State Attorney General at the same time?

Yes, and it is often advisable to do so. Filing with both agencies simultaneously creates parallel records under federal and state law. There is no prohibition on dual filing, and State AG offices frequently coordinate with the CFPB on cases involving pattern violations.

What types of complaints does the State Attorney General handle that the CFPB does not?

State AGs handle complaints involving state-specific consumer protection laws, unlicensed lenders, deceptive advertising under state statutes, and entities outside CFPB jurisdiction — such as certain auto dealers and real estate firms. They also prosecute criminal fraud, which the CFPB cannot do directly.

What should I include in a CFPB complaint to get the best result?

Include the company name, specific dates, dollar amounts involved, account numbers, and a chronological narrative of events. Attach copies of statements, contracts, or correspondence. Avoid vague language — specificity triggers more substantive company responses and makes your complaint more useful for CFPB enforcement analysis.

Is there a fee to file a CFPB complaint or a State AG complaint?

No. Filing with the CFPB at ConsumerFinance.gov is completely free. State Attorney General complaint portals are also free to use. Be cautious of any third-party service claiming to file complaints on your behalf for a fee — this is unnecessary.