Predatory vs Fair Lending: How to Tell the Difference Before You Sign

The average payday loan carries a 400% APR, stripping billions from low-income borrowers yearly. Here's how to tell a predatory loan from a fair one before you sign.

The average payday loan carries a 400% APR, stripping billions from low-income borrowers yearly. Here's how to tell a predatory loan from a fair one before you sign.

Under the FDCPA, collectors can call your job—but must stop the moment you or your employer objects. Violations can cost them up to $1,000 per lawsuit.

18 states ban payday loan rollovers entirely, and where they're allowed, lenders must disclose all fees upfront. Here's exactly what they're required to tell you.

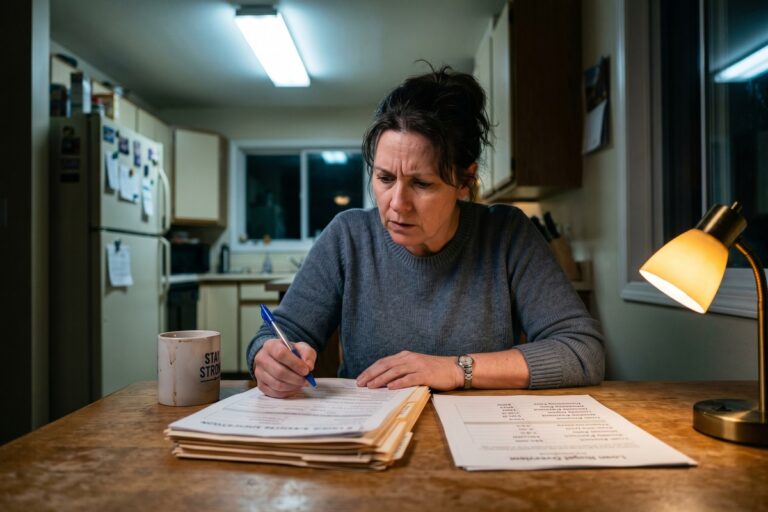

Older adults lose staggering sums to predatory lending schemes that exploit home equity and fixed incomes. Here's how lenders target seniors and what legal safeguards exist.

Seniors lose an estimated $3.4 billion annually to financial exploitation. Here's how predatory lenders identify older adults as targets—and the warning signs to catch it early.

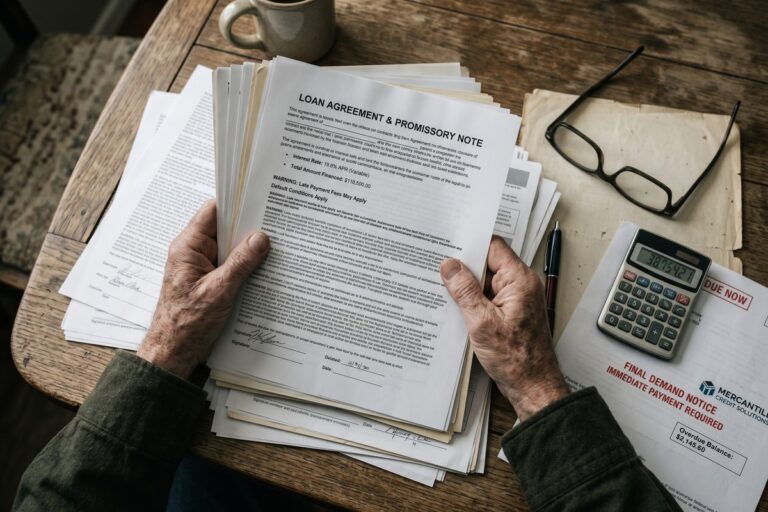

Loan sharks charge 300–700% APR with zero disclosure and no license. Here's exactly where the legal line falls between them and a regulated online lender.

The CFPB has handled over 4 million complaints since launch—file yours with the right federal and state agencies so your case gets resolved, not stalled.

Payday loan APRs can legally top 400% in states without rate caps — federal TILA rules require lenders to show that number in writing before you sign anything.

Tribal lenders can charge APRs above 400% and claim sovereign immunity from state laws. Here's what that means for your rights compared to licensed state lenders.

Undisclosed fees add $250–$500 to the average online personal loan, per the CFPB. Here's where those charges hide in your agreement and how to spot them.