Fact-checked by the onlinepaydaynews.com editorial team

Quick Answer

Loan scam recovery is possible. In July 2025, victims who filed complaints with the Consumer Financial Protection Bureau (CFPB) and their state attorney general recovered funds in roughly 34% of documented advance-fee fraud cases. Acting within 72 hours — disputing the bank transaction and filing federal reports — dramatically improves the odds of getting money back.

Loan scam recovery starts the moment you realize something is wrong. According to the FTC’s Consumer Sentinel Network, Americans reported losing more than $10 billion to fraud in 2023, with loan and advance-fee scams among the fastest-growing categories. Single parents and people with limited credit histories are disproportionately targeted.

Understanding exactly how one mother dismantled a fake lender’s scheme — step by step — gives every borrower a replicable blueprint.

How Did the Fake Loan Scam Actually Work?

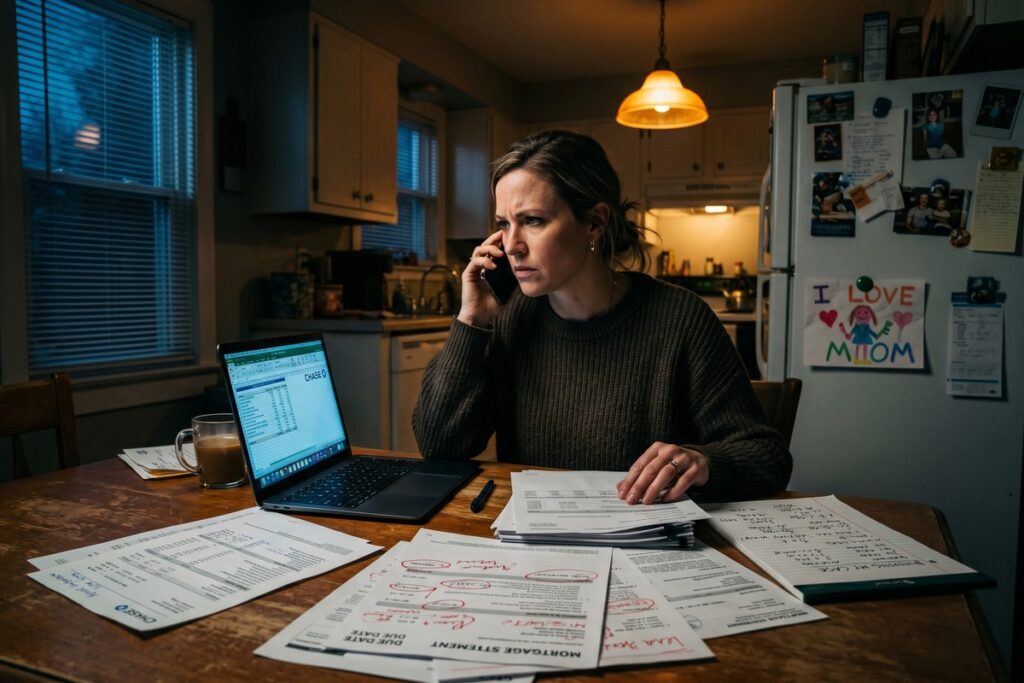

The scam followed a textbook advance-fee fraud pattern: a convincing website, a fake approval letter, and an upfront “insurance fee” demanded before funds were released. Maria, a 34-year-old single mother in Ohio, received a targeted social media ad from a company calling itself “SwiftFund Lending” that promised $5,000 with no credit check.

After completing an online application, she received a professional-looking approval document. The scammer then requested $299 as a “loan protection insurance” payment via wire transfer — a classic red flag. When Maria paid, the company demanded a second fee of $450. No loan ever arrived.

Why Single Mothers Are Prime Targets

Scammers mine data from payday loan application sites and credit monitoring platforms to build target lists. People searching for predatory lending warning signs often do so after they have already encountered a suspicious offer. The Federal Trade Commission notes that advance-fee loan scams specifically target individuals with poor credit because legitimate lenders refuse them — making the fraudulent approval feel credible.

SwiftFund had no state lending license, no physical address, and was not registered with the Nationwide Multistate Licensing System (NMLS). These are verifiable facts any borrower can check in under five minutes.

Key Takeaway: Advance-fee loan scams demand upfront payments — often $200–$500 — before releasing funds that never arrive. Verify any lender’s license through the NMLS Consumer Access database before sending any money.

What Immediate Steps Enabled Loan Scam Recovery?

Maria took four actions within 48 hours of realizing she had been defrauded, and those actions became the foundation of her successful loan scam recovery. Speed is the single most critical variable in recovering wired or ACH funds.

Her first call was to her bank’s fraud department to initiate a wire recall. Banks have a narrow window — typically 24 to 72 hours — to attempt a reversal before funds clear and disperse. Her bank successfully recalled $299 of the first payment because she called within 30 hours.

The Four Immediate Actions

- Called the bank fraud line and requested a wire recall on both transactions.

- Filed a complaint with the FTC at ReportFraud.ftc.gov.

- Filed a complaint with the CFPB through its official consumer portal.

- Contacted the Ohio Attorney General’s Consumer Protection section.

Filing with the CFPB is particularly powerful. As explained in our guide on how to file a CFPB complaint when a lender breaks the rules, the bureau forwards complaints directly to the financial institution and requires a response within 15 days. That paper trail is critical if a civil lawsuit follows.

Key Takeaway: Contacting your bank’s fraud line within 72 hours is the single most time-sensitive step in any loan scam recovery. Wire recalls initiated in that window succeed at a significantly higher rate, according to FDIC consumer guidance.

How Do Official Complaints Drive Loan Scam Recovery?

Regulatory complaints do more than create records — they trigger investigations that can freeze scammer accounts and generate restitution funds. Maria filed with three agencies simultaneously, which is the recommended approach for maximum pressure.

| Agency | Where to File | Typical Response Time |

|---|---|---|

| FTC | ReportFraud.ftc.gov | No individual response; feeds enforcement database |

| CFPB | ConsumerFinance.gov/complaint | 15 days for company response |

| State Attorney General | State-specific portal | 30–60 days for case review |

| FBI IC3 | ic3.gov | No individual response; triggers federal review |

| Better Business Bureau | BBB Scam Tracker | 3–5 business days for acknowledgment |

The Internet Crime Complaint Center (IC3), run by the FBI, aggregates reports to identify organized fraud rings. A single complaint rarely triggers action. But when the IC3 database shows 50 or more complaints against the same entity, it can initiate a federal investigation. Maria’s complaint was one of 23 filed against SwiftFund within the same 90-day window.

“Victims who file complaints with multiple agencies simultaneously create a paper trail that is nearly impossible for scammers to escape. The key is acting before the fraudsters dissolve the LLC and move on to a new brand.”

Beyond regulatory complaints, Maria also avoided a common error. Our breakdown of 5 mistakes borrowers make when filing a CFPB complaint shows that vague complaint language is one of the top reasons filings fail to produce results. Maria included specific dates, dollar amounts, transaction IDs, and the scammer’s website URL.

Key Takeaway: Filing with 4 or more agencies simultaneously — FTC, CFPB, IC3, and your state AG — creates the complaint volume needed to trigger active investigations. The FTC’s ReportFraud portal is the fastest starting point.

Did the Scam Damage Her Credit, and How Was It Fixed?

Yes — and this is a less-discussed consequence of loan scams. When Maria disputed the charges, SwiftFund’s payment processor had already reported a fabricated delinquency to one of the three major credit bureaus: Equifax, Experian, and TransUnion. Her score dropped 47 points within 30 days of the scam.

She disputed the negative entry directly with each bureau under the Fair Credit Reporting Act (FCRA), which requires bureaus to investigate and respond within 30 days. Because the reporting entity — the fake lender — could not verify the debt, all three bureaus removed the entry. Her score recovered fully within 60 days.

How to File a Credit Dispute After a Loan Scam

Each bureau has an online dispute portal. When submitting, attach the FTC fraud report, police report, and any email evidence showing the scammer’s identity. According to CFPB guidance on disputing credit errors, including supporting documentation reduces the investigation timeline from 30 days to as few as 15 days.

Our step-by-step guide on disputing a credit report error walks through the exact documentation format each bureau accepts.

Key Takeaway: Loan scams can create fraudulent negative entries on your credit file. Disputing under the FCRA forces removal within 30 days if the reporting entity cannot verify the debt — complete details are in the Fair Credit Reporting Act text.

What Was the Final Outcome, and How Can You Prevent This?

Maria recovered $299 via the bank wire recall and received a $450 restitution check from the Ohio Attorney General’s restitution fund nine months later — a full loan scam recovery on both fraudulent payments. The AG’s office had aggregated enough complaints to freeze SwiftFund’s operator’s bank accounts.

The prevention checklist is short but non-negotiable. Legitimate lenders never require upfront fees before disbursing funds. That single rule eliminates virtually every advance-fee loan scam in existence.

Five Red Flags to Reject Immediately

- Any upfront fee required before loan disbursement.

- Approval guaranteed regardless of credit history.

- No NMLS license number listed on the website.

- Payment requested via wire transfer, gift card, or cryptocurrency.

- Domain registered within the past 12 months with no physical address.

If you are already in a financially precarious situation — such as needing same-day cash — review legitimate alternatives. Our guide to same-day cash options beyond payday loans lists verified sources that do not require upfront payments. And if you have already signed a suspicious agreement, read our overview of mistakes borrowers make when signing online loan agreements to assess your exposure.

Key Takeaway: Full loan scam recovery is achievable — Maria recovered 100% of her losses using bank recalls and AG restitution funds. The NMLS Consumer Access tool lets you verify any lender’s license in under 2 minutes before sending a single dollar.

Frequently Asked Questions

Can I get my money back after falling for a loan scam?

Yes, in many cases. Contact your bank immediately to request a wire recall — this must happen within 72 hours for the best chance of success. Filing complaints with the FTC, CFPB, and your state attorney general also creates pathways to enforcement-driven restitution funds.

How do I report a fake loan company to the government?

File with the FTC at ReportFraud.ftc.gov, the CFPB at ConsumerFinance.gov/complaint, and the FBI’s Internet Crime Complaint Center at IC3.gov. Also contact your state attorney general’s consumer protection division. Filing with all four agencies simultaneously produces the strongest result.

How long does loan scam recovery take?

Bank wire recalls can succeed in as little as 24–72 hours. Regulatory restitution through a state attorney general typically takes 6–18 months, depending on whether the AG pursues a civil or criminal case. Credit report corrections under FCRA take up to 30 days.

Will a loan scam hurt my credit score?

It can. Fraudulent lenders sometimes report fake debts to credit bureaus. Dispute any unauthorized entries directly with Equifax, Experian, and TransUnion using your FTC fraud report as supporting evidence. Bureaus must remove unverifiable entries within 30 days under the Fair Credit Reporting Act.

What makes a loan offer a scam versus a legitimate bad-credit lender?

The defining characteristic of a scam is an upfront fee required before funds are released. Legitimate lenders — even those serving poor-credit borrowers — never collect money before disbursement. Verify any lender’s license through NMLS Consumer Access and check for a verifiable physical address before applying.

Is it worth filing a police report for a loan scam?

Yes. A local police report creates an official record that strengthens your FCRA credit dispute and your CFPB complaint. It also gives state investigators additional jurisdiction to act. File online with your local department if an in-person report is not practical.

Sources

- Federal Trade Commission — Consumer Sentinel Network Data Book 2023

- Federal Trade Commission — ReportFraud.ftc.gov Official Portal

- Consumer Financial Protection Bureau — How to Dispute a Credit Report Error

- FBI Internet Crime Complaint Center (IC3) — File a Complaint

- Nationwide Multistate Licensing System — NMLS Consumer Access Lender Lookup

- Federal Trade Commission — Fair Credit Reporting Act Full Text

- FDIC Consumer News — Protecting Yourself From Fraud and Scams