Fact-checked by the onlinepaydaynews.com editorial team

Quick Answer

A divorced parent can access emergency cash after divorce through personal loans, credit union emergency programs, nonprofit assistance, and employer payroll advances — often within 24–48 hours. Solo borrowers with fair credit can qualify for personal loans between $1,000 and $10,000 without a co-signer or joint account.

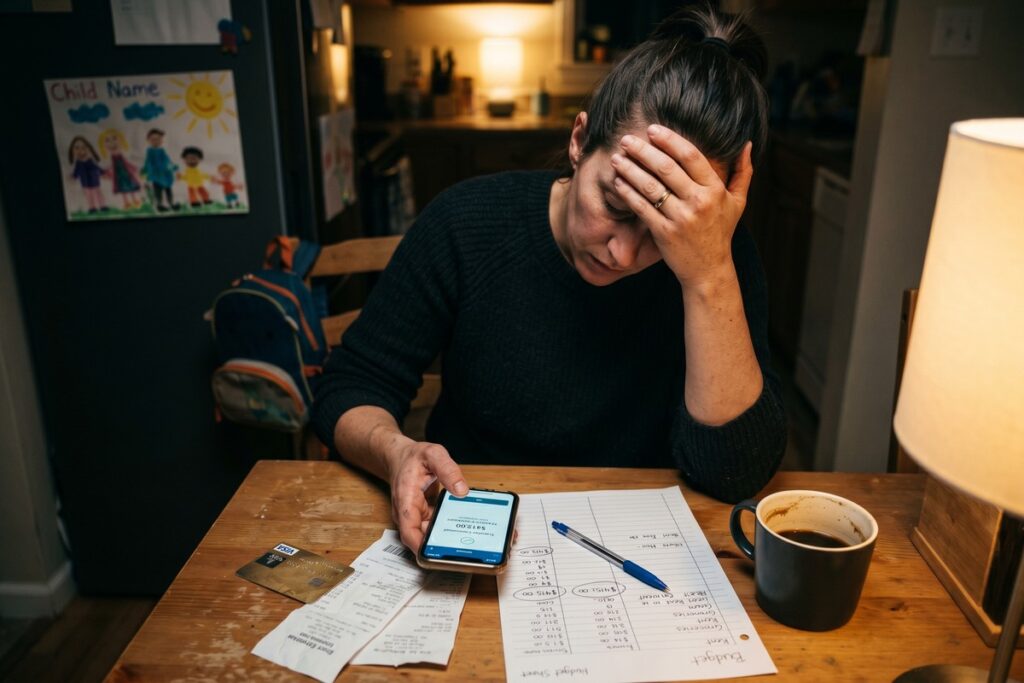

More than 15 million custodial single parents live in the United States, according to U.S. Census Bureau data, and a significant share report no emergency savings buffer after separation. Without a joint account, a co-signing spouse, or family support, a $4,500 emergency stops being a financial problem and becomes something that feels structurally unsolvable.

The reason it feels that way is partly real. Divorce severs financial infrastructure that took years to build. But the borrowing options available to newly single parents have expanded meaningfully. More lenders now underwrite on individual income, alternative data, and banking history rather than household income, which has opened up credit access that simply did not exist at this scale a few years ago.

This guide covers what actually works, how fast it works, and what to avoid when every day of delay costs money.

Key Takeaways

- Over 15 million custodial single parents live in the U.S., many with no emergency savings buffer after separation, per U.S. Census Bureau data.

- Newly single adults experience a sharp drop in liquid savings in the first 12 months post-separation, according to Urban Institute research.

- Credit union Payday Alternative Loans cap interest at 28% APR under NCUA rules, making them among the lowest-cost regulated emergency products available.

- A borrower with a thin credit file can become fully scoreable in as few as 3–6 months of reported payment activity, per Experian.

- Payday loans carry a national average of 400% APR, as documented by the CFPB — and more than 20% of title loan borrowers have their vehicle repossessed.

- The federal TANF program and CSBG-funded community agencies can provide emergency relief to qualifying single-parent households, often within 72 hours, through HHS program resources.

Why Does Divorce Break Your Emergency Financial Safety Net?

Divorce severs the financial infrastructure most couples take for granted. Joint accounts close, household income splits, and credit profiles that were once blended suddenly stand alone.

Research from the Urban Institute shows that newly single adults experience a sharp drop in liquid savings in the first 12 months post-separation. For the parent who retained primary custody, monthly expenses often stay near the pre-divorce level while income drops considerably. This gap is where emergencies — a car breakdown, a medical bill, a broken furnace — become crises rather than inconveniences.

The Credit Profile Problem

Many divorced individuals discover their solo credit history is thin. If the primary mortgage, auto loan, or credit card was held by the other spouse, a newly single parent may have a FICO score below 640 and a short individual credit file. Lenders use this profile when evaluating applications, which narrows options quickly. Understanding how to start building credit from absolute zero is often the first practical step a recently divorced parent must take.

The timing problem compounds everything. Credit-building takes months. Emergencies do not wait.

Key Takeaway: Divorce can reduce a single parent’s liquid savings access by as much as 50% within the first year, according to Urban Institute research. Thin solo credit files compound the problem, making pre-planned borrowing strategies essential before a crisis hits.

What Are the Fastest Emergency Cash Options After Divorce?

The fastest legitimate sources of emergency cash after divorce are personal installment loans, credit union payday alternative loans (PALs), and employer-based payroll advances — each reachable within one to three business days.

Personal installment loans from online lenders like Upstart, LightStream, or Avant are the most flexible option. Upstart uses education and employment data alongside credit scores, which benefits borrowers with thin files. Approval decisions can arrive within hours, with funds deposited the next business day.

Credit union PALs are federally regulated under NCUA guidelines and cap interest at 28% APR with loan amounts between $200 and $2,000. For a $4,500 need, a borrower would combine a PAL with a second source — but the rate savings are significant compared to payday products. Before taking any short-term loan, reviewing how to distinguish predatory from fair lending can prevent a costly mistake.

Employer Payroll Advances and Earned Wage Access

Apps like DailyPay and Rain (formerly Even) allow employees at participating employers to access earned wages before payday. These are not loans — no credit check is required, and fees are typically $1–$3 per transfer. For a parent who has already earned the funds, this is the lowest-cost bridge available. The catch is availability: the employer must participate, and not all do.

| Option | Speed | Max Amount | Approx. APR / Fee | Credit Check? |

|---|---|---|---|---|

| Personal Installment Loan | 1–2 business days | $10,000+ | 9%–36% APR | Yes (soft or hard) |

| Credit Union PAL | 1–3 business days | $2,000 | 28% APR max | Yes (membership req.) |

| Earned Wage Access App | Same day | 50% of earned wages | $1–$3 flat fee | No |

| Nonprofit Emergency Fund | 2–5 business days | $1,500 typical max | 0% (grant or 0% loan) | No |

| 401(k) Hardship Withdrawal | 3–7 business days | Plan-dependent | 10% penalty + taxes | No |

Key Takeaway: Credit union Payday Alternative Loans cap interest at 28% APR under NCUA rules, making them among the lowest-cost emergency options for divorced borrowers — but the $2,000 limit means they often must be paired with a second funding source to cover larger gaps like a $4,500 expense.

How Do You Actually Cover $4,500 When No Single Source Gets You There?

A $4,500 emergency rarely requires one single funding source to cover it entirely. In practice, most divorced parents who successfully bridge a gap this size do it by combining two or three sources, each handling a portion of the total.

A realistic stack might look like this: a credit union PAL covers $1,500 at 28% APR, a 211 emergency assistance referral covers $800 in utility or rent relief, and a personal installment loan from an online lender covers the remaining $2,200 at roughly 20–30% APR depending on the applicant’s profile. That distribution keeps the high-cost debt portion as small as possible while using zero-cost or low-cost resources for everything they will stretch to cover.

The 401(k) Option: When It Makes Sense and When It Does Not

A 401(k) hardship withdrawal is worth understanding clearly. The funds are yours — there is no credit check — but withdrawing before age 59½ typically triggers a 10% early withdrawal penalty plus ordinary income taxes on the amount taken. On a $4,500 withdrawal, a borrower in the 22% federal tax bracket could lose roughly $1,440 to taxes and penalties, meaning the real cost of accessing $4,500 is closer to $5,940.

A 401(k) loan (as opposed to a withdrawal) avoids the penalty if repaid within the plan’s required window, typically five years. However, if employment ends while the loan is outstanding, the balance often becomes immediately due. For a divorced parent whose job security may already feel uncertain, that contingency risk matters.

Use a 401(k) withdrawal as a last resort. Use it knowingly, not by default.

Negotiating Directly With the Creditor or Vendor

This step gets skipped constantly. Before borrowing anything, contact whoever is owed the $4,500 directly. Medical providers, repair shops, and landlords frequently accept payment plans with no interest. A hospital billing department will often reduce the balance for uninsured or underinsured patients who ask. A furnace repair company may defer payment 30 days with a signed agreement. These conversations cost nothing and can reduce the amount that actually needs to be borrowed.

Key Takeaway: Covering a $4,500 gap by combining a credit union PAL, nonprofit assistance, and a targeted personal loan keeps the highest-cost debt portion small. Direct negotiation with the creditor before borrowing can reduce the total needed — a step worth taking before submitting any loan application.

How Can a Divorced Parent Build Emergency Borrowing Power Quickly?

The single most effective move a newly divorced parent can make is to open a secured credit card or credit-builder loan immediately — before an emergency strikes. Each month of on-time payment adds positive data to a solo credit file.

According to Experian’s credit-building guidance, a borrower with a thin file can move from no score to a scoreable profile in as few as 3–6 months of reported payment activity. A secured card with a $200–$500 deposit, reported to all three bureaus — Equifax, TransUnion, and Experian — is the fastest on-ramp.

The National Foundation for Credit Counseling (NFCC) consistently advises newly separated individuals to prioritize independent credit establishment before focusing on debt payoff or savings goals. Their reasoning is straightforward: a person with no credit access and no savings is one event away from a predatory loan. A person with even a modest, scoreable credit file has more options. Information on their counseling resources is available at NFCC.org.

Rent reporting is another underused tool. Services like Experian RentBureau and Rental Kharma report monthly rent payments to the credit bureaus, adding positive tradelines at no cost or very low cost. For a divorced parent paying rent for the first time, this can meaningfully accelerate credit file growth. Learn more about how rent reporting services can boost credit for renters who are starting over.

Key Takeaway: A divorced parent who opens a secured card immediately after separation can become fully scoreable within 3–6 months, according to Experian — creating emergency borrowing access before the next crisis, not during it.

What Do Lenders Actually Look At for a Solo Applicant?

When a divorced parent applies for a personal loan individually for the first time, the underwriting process may feel unfamiliar. Knowing exactly what lenders evaluate removes some of the guesswork.

Most personal loan lenders weigh five factors: credit score, income, debt-to-income ratio, employment stability, and credit history length. A recently divorced borrower may score well on income and employment while scoring poorly on credit history length and debt-to-income ratio, particularly if they assumed any marital debt in the settlement. The combination matters more than any single number.

Debt-to-Income Ratio After Divorce

Debt-to-income (DTI) ratio — the percentage of gross monthly income consumed by debt payments — is often the variable that catches newly single borrowers off guard. A person who earned $80,000 jointly and now earns $45,000 individually, while retaining the same car payment, credit card balance, and student loan, may have a DTI above 45%. Most conventional personal loan lenders prefer DTI below 40%, and the better rates go to borrowers below 35%.

The practical implication: before applying for a personal loan, calculate your own DTI. Add up all monthly minimum debt payments, divide by gross monthly income, and multiply by 100. If the result is above 45%, prioritize paying down one revolving balance before applying, or look at lenders like Upstart and OneMain Financial that have more flexible DTI thresholds.

Soft Pull vs. Hard Pull Applications

Most online personal loan lenders now offer a pre-qualification process using a soft credit pull that does not affect your score. This matters for a divorced borrower who may be rate-shopping across multiple lenders. Submitting five full applications simultaneously can knock 15–25 points off a credit score through hard inquiries — a meaningful hit when the score is already thin. Always use pre-qualification tools first, then submit a formal application only with the lender whose offer is strongest.

Key Takeaway: Debt-to-income ratio frequently disqualifies recently divorced borrowers even when income is stable. Calculating DTI before applying — and using soft-pull pre-qualification tools to shop rates without score damage — gives a solo applicant a significant practical advantage.

What Nonprofit and Government Programs Cover Emergency Gaps After Divorce?

Nonprofit emergency funds and government assistance programs can cover a meaningful portion of a $4,500 gap — often with no repayment required. These are frequently overlooked because they are not marketed as “loans.”

The Temporary Assistance for Needy Families (TANF) program, administered by the U.S. Department of Health and Human Services, provides emergency cash assistance to qualifying single-parent households. Benefit levels vary by state but are available within days of an approved application.

Community action agencies, funded through the Community Services Block Grant (CSBG), offer emergency utility, rent, and food assistance that frees up cash for other urgent expenses. The 211 helpline (dialing 2-1-1) connects callers to local programs in under 60 seconds. For single parents also managing unexpected medical bills, the mistakes outlined in how to avoid common errors when covering medical bills apply directly to post-divorce emergencies.

Child Support Emergency Modifications

If the emergency directly affects the child, a family law attorney can file for an expedited child support modification in most states. Some jurisdictions process emergency modifications within 72 hours. This is not a loan — it is a legal mechanism, and it costs nothing to request through the state child support enforcement agency.

Organizational Emergency Funds Worth Knowing

Beyond TANF and CSBG, a number of nonprofit organizations provide direct emergency assistance to single parents. The Salvation Army and Catholic Charities USA both operate emergency financial aid programs in most major metros, covering utilities, rent arrears, and food. Faith-based organizations in many communities maintain discretionary emergency funds not widely advertised. Calling 211 surfaces these resources faster than any online search.

Some professional associations and labor unions also maintain hardship funds for members in acute financial distress. If you belong to a union or a professional organization, contact them directly — these funds often go unclaimed simply because members do not know they exist.

Key Takeaway: The federal TANF program and local CSBG-funded agencies provide emergency cash and in-kind relief to qualifying single-parent households, often within 72 hours. Calling 211 or visiting the HHS TANF portal is the fastest way to identify what is available by zip code.

What Borrowing Traps Should Divorced Parents Avoid?

Divorced parents under financial stress are a documented target market for predatory lenders. High-cost payday loans, rent-to-own agreements, and title loans can convert a $4,500 emergency into a $9,000 debt spiral within 90 days.

A payday loan carrying a 400% APR — the national average documented by the Consumer Financial Protection Bureau (CFPB) — on a $500 advance costs roughly $75 in fees per two-week cycle. Rolling that loan over just three times triples the original fee. Understanding the payday loan rollover rules lenders are required to disclose can prevent a borrower from being trapped without realizing it until the debt has already compounded.

Title loans carry similar risks. They use a vehicle as collateral — and for a custodial parent, losing a vehicle means losing the ability to get to work and transport children. The CFPB has found that more than 20% of title loan borrowers have their vehicle repossessed. That statistic deserves to sit on its own.

Installment Loan Red Flags

Not all installment loans are safe. Warning signs include prepayment penalties, mandatory arbitration clauses, and loan terms that bury the total repayment cost. A lender who is reluctant to show you the total cost of borrowing — not just the monthly payment — is worth walking away from. For context on evaluating any installment agreement, the most costly installment loan mistakes borrowers make provides a direct checklist before signing.

One specific trap worth naming: some online lenders advertise low monthly payments while quietly extending loan terms to 48 or 60 months on amounts that should be repaid in 12. A $3,000 loan at 29% APR over 48 months costs over $1,900 in interest. The same loan over 18 months costs about $700. The difference is not small, and the longer-term loan is often the default option presented first.

Key Takeaway: Payday loans averaging 400% APR, as documented by the CFPB, and title loans with a documented 20%+ repossession rate are the two borrowing products most likely to worsen a post-divorce financial emergency rather than resolve it.

What Comes After the Emergency: Rebuilding Financial Stability

Covering the immediate crisis is only part of the problem. A divorced parent who borrows $4,500 in an emergency and then does nothing differently is statistically likely to face the same situation again within 18 months. The structural gap — no buffer, thin credit, single income — does not close by itself.

Building a $1,000 emergency fund takes priority over almost everything else after the immediate debt is managed. It sounds modest, but research consistently shows that households with even $400–$500 in liquid savings are substantially less likely to miss bill payments, incur overdraft fees, or turn to high-cost credit in a subsequent emergency. The exact figure matters less than having something.

Setting Up a Separate Emergency Account

A high-yield savings account at an online bank, kept separate from the checking account used for daily expenses, creates both physical and psychological separation. Automatic transfers of even $25–$50 per paycheck compound over time. The account should be inconvenient to access — not impossible, but not a debit card sitting in your wallet. Friction reduces impulsive spending.

Monitoring Your Credit File After Divorce

Post-divorce credit monitoring is not optional for anyone rebuilding a solo file. Joint accounts that the other party was supposed to manage can appear delinquent on both credit reports. Authorized user accounts that the other party closes without notice can reduce your available credit and raise your utilization ratio overnight. Checking your reports at AnnualCreditReport.com every 90 days post-divorce catches these problems while they are still correctable.

Dispute errors directly with the bureaus — Equifax, TransUnion, and Experian each have an online dispute portal. Errors related to marital debt allocation are among the most common post-divorce credit report problems and among the most correctable, provided you act before the delinquency history deepens.

Key Takeaway: A $1,000 emergency fund and quarterly credit report checks are the two structural changes most likely to prevent a post-divorce emergency from repeating. Neither requires high income — both require consistency.

Frequently Asked Questions

Can I get an emergency loan right after my divorce is finalized?

Yes. Lenders evaluate individual applications — your marital status does not disqualify you. What matters is your solo income, credit score, and debt-to-income ratio. Online lenders can approve and fund emergency personal loans in as little as 24 hours after a finalized divorce.

How do I get emergency cash after divorce if my credit score is below 600?

Focus on credit union Payday Alternative Loans (PALs), earned wage access apps, nonprofit emergency funds, and TANF assistance first. These do not require a strong credit score. If you must borrow, look for lenders like Upstart or OneMain Financial that underwrite using income and employment data alongside credit scores.

Can a single parent get a personal loan without a co-signer?

Yes — most online personal loan lenders do not require co-signers. Approval is based on individual income, credit history, and employment status. A single parent with steady employment and a credit score above 620 will qualify with most major lenders without a co-signer.

What is the fastest way to get $4,500 in an emergency after divorce?

The fastest legal path is an online personal installment loan from a lender like Avant or LightStream, combined with a 211 emergency assistance referral for any portion the loan does not cover. Together, these can close a $4,500 gap within two business days without requiring a joint account or family guarantor.

Does divorce hurt my credit score?

Divorce itself does not appear on credit reports and does not directly lower your score. However, closing joint accounts, losing shared tradelines, and taking on individual debt can reduce your score indirectly. Monitoring your file through AnnualCreditReport.com every 90 days post-divorce helps catch any errors quickly.

Are there emergency grants for single parents that do not need to be repaid?

Yes. TANF, CSBG-funded community action agencies, and some nonprofit organizations — including the Salvation Army and Catholic Charities USA — offer non-repayable emergency assistance for qualifying single parents. Call 211 or visit your county’s social services office to apply. These programs are income-tested and vary by state.