Installment Loans vs Line of Credit: Which One Actually Fits a Cash Crisis?

Installment loans average 11–36% APR for one-time crises; lines of credit work better for recurring shortfalls. Compare costs and terms to pick the right fit.

Installment loans average 11–36% APR for one-time crises; lines of credit work better for recurring shortfalls. Compare costs and terms to pick the right fit.

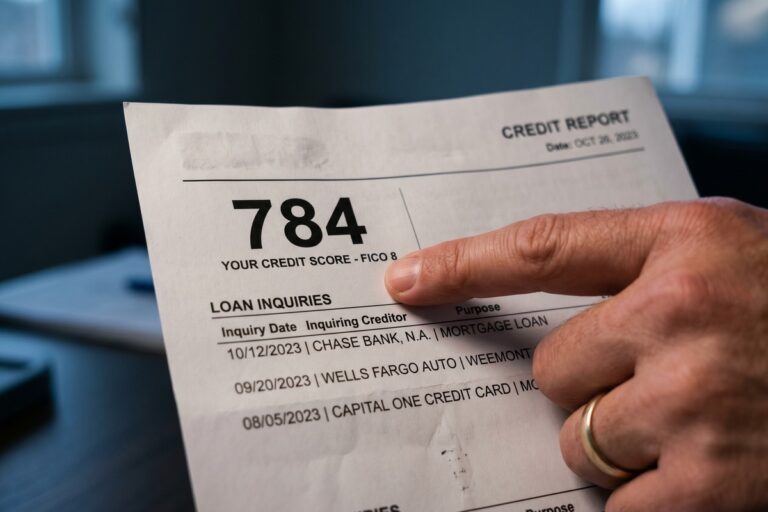

Only 33% of laid-off adults stayed financially stable, per the Fed's 2024 SHED. If your solo DTI stays under 43%, a credit union PAL or fintech loan may bridge the gap—here's the math.

Campus short-term loans can hit 400% APR — but school emergency programs often lend up to $1,500 at 0%. Here's what lenders skip over before you sign.

Learn about missed short-term loan payment consequences. See exactly what happens week by week — from late fees to collections — and how to protect yourself.

SBA microloans average $13,000 at 8–13% APR for business needs. Payday loans average $375 at triple-digit APR for personal emergencies. These two products serve completely different borrowers.

16.3% of Americans have scores below 600. See how no-credit-check loans really work and what hidden trade-offs replace that promised protection.

Learn about payday loans vs rent-to-own. Compare true costs, APRs, and hidden fees to find out which financing option drains your wallet faster.

Carrying multiple open accounts won't automatically sink your application — but a DTI above 43–50% will. Here's what lenders actually measure and why it matters.

Learn about short-term loans teachers can use. Discover borrowing options designed for educators facing irregular summer pay gaps and seasonal income challenges.

Payday loans average 391% APR while credit union alternatives cap at 28%. Here's how first-time short-term loan borrowers compare total costs and avoid debt spirals.