Consumer Protection Laws That Changed in 2026 and What They Mean for Borrowers

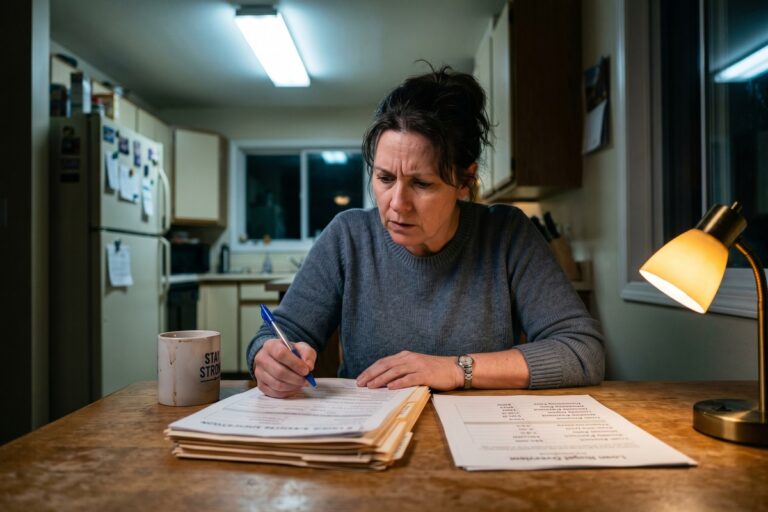

Lenders now face $50,000-per-violation fines and borrowers get 60-day BNPL dispute windows under 2026's biggest regulatory overhaul since Dodd-Frank.

Lenders now face $50,000-per-violation fines and borrowers get 60-day BNPL dispute windows under 2026's biggest regulatory overhaul since Dodd-Frank.

Federal law protects 12 characteristics from lender questioning—including race, religion, and family plans. Here's what creditors cannot legally ask and how to report violations.

Learn about loan scams seniors face daily. Discover the top tactics fraudsters use and proven steps older adults can take to protect their finances.

Collectors who call before 8 a.m. or text your debt details to third parties can face $1,000 fines per lawsuit. Here's what the FDCPA actually prohibits.

A certified-mail FCRA dispute beats the online portal form — and patients in 15 states plus nonprofit hospital borrowers have enforceable rights most never invoke.

The CFPB has recovered $1.6B from predatory lenders since 2011. Here's how one gig worker documented an unauthorized renewal fee and got a full refund in under 90 days.

Over 6 million CFPB complaints filed — yet many go unresolved because borrowers skip critical steps like attaching documents or naming the right company. Here's what to fix.

The average payday loan carries a 400% APR, stripping billions from low-income borrowers yearly. Here's how to tell a predatory loan from a fair one before you sign.

Getting utilization below 30% can add 50–75 points alone. Here's how one truck driver recovered from three years of credit gaps to break the 680 threshold.

Under the FDCPA, collectors can call your job—but must stop the moment you or your employer objects. Violations can cost them up to $1,000 per lawsuit.