Fact-checked by the onlinepaydaynews.com editorial team

Quick Answer

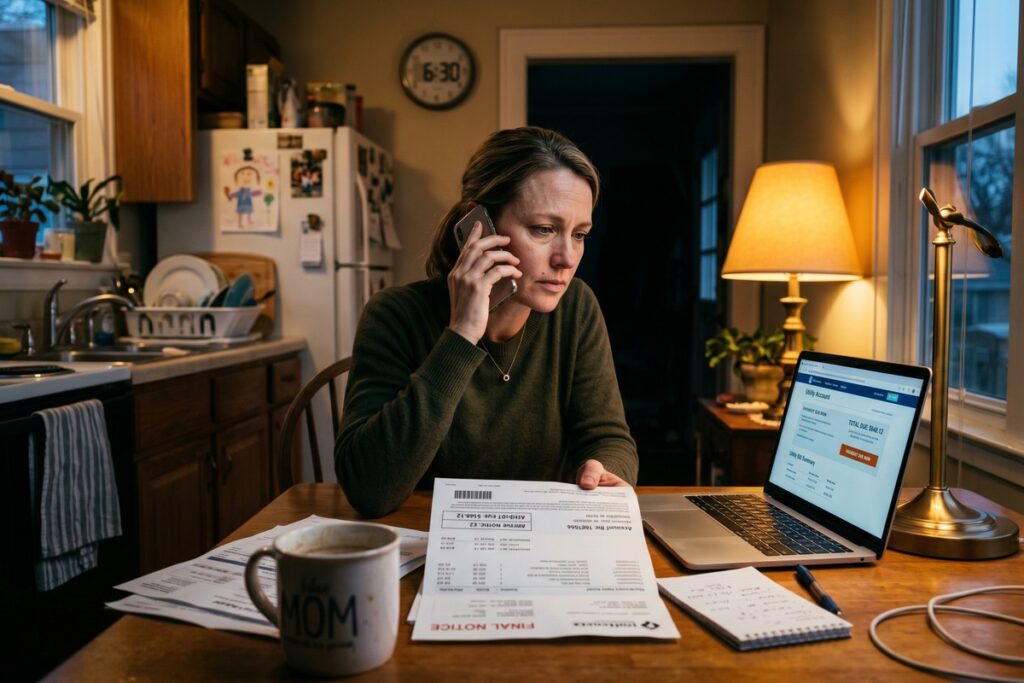

If you are facing a utility shutoff emergency, contact your utility provider immediately to request a payment plan or 30-day extension, then apply for LIHEAP, which distributes over $4 billion annually to low-income households for energy costs. Most states also have additional local programs that can halt a shutoff within 24–48 hours.

More than 37 million households qualify for federal energy assistance each year, according to the U.S. Department of Energy’s LIHEAP program overview, yet millions never apply. Acting within the first 24 hours of receiving a shutoff notice is what separates a recoverable situation from a full disconnection with reconnection fees stacked on top.

Rising energy costs and stretched household budgets have made utility crises more common. Knowing exactly where to turn and what to say can keep your power, water, or gas on even when your account is past due.

Key Takeaways

- 37 million households qualify for LIHEAP energy assistance annually, per the U.S. Department of Energy, yet millions never apply.

- 150% of the Federal Poverty Level is the standard LIHEAP income threshold, a family of four can earn roughly $46,800 annually and still qualify.

- Most states require utilities to provide a written disconnection notice at least 10 to 30 days in advance, giving households a critical window to negotiate or apply for aid.

- The United Way’s 2-1-1 network handled over 17 million contacts in 2023 and remains the fastest single path to local emergency utility funds in most ZIP codes.

- Post-disconnection reconnection fees run $25 to $200, depending on the state and utility provider, making pre-shutoff negotiation a clear financial advantage.

- A utility shutoff does not appear directly on your Experian, Equifax, or TransUnion credit file, but an unpaid balance sent to collections can damage your FICO Score significantly.

What Exactly Qualifies as Utility Shutoff Emergency Help?

Utility shutoff emergency help refers to any formal program, negotiation, or assistance that prevents or reverses a disconnection of essential services, electricity, gas, or water, due to nonpayment. These include federal programs, state-run funds, nonprofit relief, and utility company hardship policies.

Most utility companies are legally required to send a written shutoff notice at least 10 to 30 days before disconnection, depending on the state. That window is your first and most powerful opportunity to act. Calling your utility’s billing department and using the words “financial hardship” opens a set of internal options most representatives will not volunteer on their own.

Protections vary widely by state. Many states prohibit winter shutoffs entirely for households below a certain income threshold. The National Consumer Law Center’s Surviving Debt guide outlines these state-by-state protections in detail and is a critical resource for anyone in a shutoff emergency.

Key Takeaway: Utility shutoff emergency help begins the moment you receive a disconnection notice. Most states mandate a 10–30 day notice period, use it immediately to contact your utility and request hardship options before the shutoff date. See NCLC’s state-by-state guide for specific protections in your area.

How Does LIHEAP Work and Who Qualifies?

The Low Income Home Energy Assistance Program (LIHEAP), administered by the U.S. Department of Health and Human Services, is the largest federal source of utility shutoff emergency help in the country. It provides direct payments to utility companies on behalf of eligible households, bypassing the borrower entirely.

To qualify, your household income generally must be at or below 150% of the Federal Poverty Level, though states retain some flexibility to set their own thresholds. A family of four can earn up to approximately $46,800 annually and still qualify under current federal guidelines. Benefits average between $400 and $600 per year per household, though crisis assistance awards can be higher.

How to Apply for LIHEAP

Applications go through your state or local LIHEAP administering agency, not through a federal portal. Use the Benefits.gov LIHEAP locator to find your state’s specific intake office. Processing times vary, but many agencies offer same-week crisis appointments when a shutoff notice is present.

Bring your shutoff notice, a recent utility bill, proof of income, and government-issued ID to your appointment. Having these documents ready cuts processing time significantly.

Key Takeaway: LIHEAP serves more than 6 million households annually and can pay your utility directly. Income eligibility is up to 150% of the Federal Poverty Level. Find your local office through Benefits.gov’s LIHEAP locator and bring your shutoff notice to the appointment.

| Program | Who Administers It | Typical Benefit Amount | Turnaround Time |

|---|---|---|---|

| LIHEAP (Federal) | State/local agencies via HHS | $400–$600 (crisis awards higher) | 2–7 business days |

| Utility Company Hardship Fund | Individual utility provider | $100–$500 credit | 1–3 business days |

| State Energy Assistance | State public utility commission | $150–$800 | 3–10 business days |

| Salvation Army EFSP | Local Salvation Army chapter | $50–$300 one-time | Same day to 48 hours |

| 2-1-1 Referral Network | United Way / local nonprofits | Referral-based (varies by fund) | Same day referral |

What Can You Negotiate Directly With Your Utility Company?

Most utility companies maintain internal assistance programs that are rarely advertised. Calling and asking specifically for a budget billing plan, deferred payment agreement, or hardship fund can stop a shutoff without involving any government agency.

Budget billing spreads your annual usage cost into equal monthly payments, preventing the seasonal spikes that trigger delinquency. Deferred payment agreements let you pay your past-due balance over 3 to 12 months while keeping current service active. These are standard tools at major providers including Duke Energy, Con Edison, and Pacific Gas and Electric (PG&E), but you must ask for them explicitly. Providers will not offer them unprompted.

According to the National Energy Assistance Directors’ Association (NEADA), customers who contact their utility before a shutoff are significantly more likely to reach a workable agreement. Once a disconnection order is issued, the options narrow and reconnection fees apply on top of the balance owed.

Reconnection fees typically run $25 to $200 depending on the utility and state. That cost compounds an already strained budget, which is why pre-shutoff negotiation is the far better financial outcome. If you find yourself considering high-cost borrowing to cover a utility bill, first read our guide on predatory vs. fair lending before signing anything.

Key Takeaway: Call your utility before the shutoff date and specifically request a deferred payment agreement, most major providers offer 3–12 month repayment terms. Post-disconnection reconnection fees of $25–$200 make negotiating early a clear financial advantage. See NEADA’s utility assistance resources for program details by state.

What Nonprofit and Local Resources Can Stop a Shutoff Fast?

Beyond federal programs, a strong network of nonprofit organizations provides rapid utility shutoff emergency help, sometimes same-day. These include the Salvation Army, Catholic Charities USA, St. Vincent de Paul Society, and local community action agencies.

Dialing 2-1-1 (available in all 50 states) connects you to a local specialist who can identify active emergency utility funds in your ZIP code. The United Way’s 2-1-1 network handled over 17 million contacts in 2023, many of them utility crisis calls. This is one of the fastest ways to locate money that has not yet been claimed from local emergency funds.

Church and Community Emergency Funds

Local congregations often maintain discretionary funds for household emergencies. Unlike government programs, these typically require no income documentation and can issue a utility payment within 24 to 48 hours. Call local churches, mosques, and synagogues directly and ask for their emergency assistance coordinator.

Community action agencies, funded partly under the Community Services Block Grant (CSBG) program, also hold emergency utility funds. Use the Community Action Partnership agency locator to find the office nearest you.

If you are also dealing with broader financial pressure, unexpected medical costs or income disruption, resources on same-day cash alternatives beyond payday loans and guidance on avoiding costly mistakes with unexpected bills can help you manage the full picture without taking on harmful debt.

Key Takeaway: Calling 2-1-1 connects you to local emergency utility funds in minutes. The United Way’s 2-1-1 network handled 17 million contacts in 2023. The Community Action Partnership locator also finds nearby agencies with CSBG-funded emergency utility assistance.

What Are Your Legal Rights During a Utility Shutoff Emergency?

You have enforceable legal rights during a utility shutoff emergency. Public Utility Commissions (PUCs) in every state regulate disconnection rules, and many provide meaningful consumer protections that utility companies are required to follow.

Common protections include prohibition on shutoffs on Fridays, weekends, or holidays; mandatory notice periods of at least 10 days; and moratoriums on winter disconnections for households with children, elderly members, or serious medical conditions. California’s Public Utilities Commission Rule 12 and New York’s Home Energy Fair Practices Act are two examples of strong state-level protections. Check your state’s rules before assuming any particular protection applies to you.

If your utility violates these rules, you can file a formal complaint with your state PUC. You may also be able to file a complaint with the Consumer Financial Protection Bureau (CFPB) if a third-party debt collector is involved in pursuing the past-due balance. Read about common mistakes to avoid when filing a CFPB complaint to make sure your complaint is handled properly.

Medical baseline programs are another layer of protection worth knowing about. If anyone in your household requires electricity for medical equipment such as a ventilator or oxygen concentrator, register as a medical baseline customer with your utility immediately. This designation delays disconnection and may also qualify you for reduced rates under your utility’s tariff structure.

Key Takeaway: Every state PUC mandates at least a 10-day written notice before disconnection, and many prohibit shutoffs on weekends or during winter months. Register as a medical baseline customer if anyone in your home uses life-sustaining equipment. File complaints at your state Public Utility Commission if rules are violated.

Frequently Asked Questions

What do I do if my electricity is shut off and I have no money?

Call 2-1-1 immediately to connect with local emergency utility assistance funds. At the same time, contact your utility’s hardship line to request reconnection under a deferred payment agreement. Same-day reconnection is possible in many areas when a payment arrangement is confirmed.

How quickly can LIHEAP stop a utility shutoff?

LIHEAP crisis assistance can be processed in as little as 24 to 72 hours when a shutoff notice is presented. Contact your local LIHEAP administering agency directly, not the federal website, and explain that a disconnection is imminent. Many agencies maintain a dedicated crisis intake line for exactly this situation.

Can a utility company legally shut off my power in winter?

In many states, utilities are prohibited from disconnecting residential customers during winter months, especially for households with elderly residents, children under 18, or documented medical conditions. Rules vary significantly by state. Contact your state Public Utility Commission to confirm the protections in your area before assuming you are covered.

Will a utility shutoff hurt my credit score?

A utility shutoff itself does not directly appear on your credit report. However, if the past-due balance is sent to a collections agency, it can be reported to Equifax, Experian, and TransUnion and damage your FICO Score significantly. Resolving the debt before it reaches collections is critical. You can also explore rent reporting services to build positive credit history while managing utility costs.

What is the fastest way to get utility shutoff emergency help today?

Dial 2-1-1 for an immediate referral to local emergency funds. For federal assistance, apply directly through your state LIHEAP agency with your shutoff notice in hand. Same-day appointments are often available for crisis cases.

Can I use a short-term loan to pay a utility bill before shutoff?

A short-term loan can bridge the gap, but only after exhausting free assistance programs first. Before borrowing, read about the real costs of using short-term loans for essential bills to make sure you are not trading one crisis for a worse one. High-APR products can trap low-income households in a debt cycle that makes future shutoffs more likely, not less.