Fact-checked by the onlinepaydaynews.com editorial team

Quick Answer

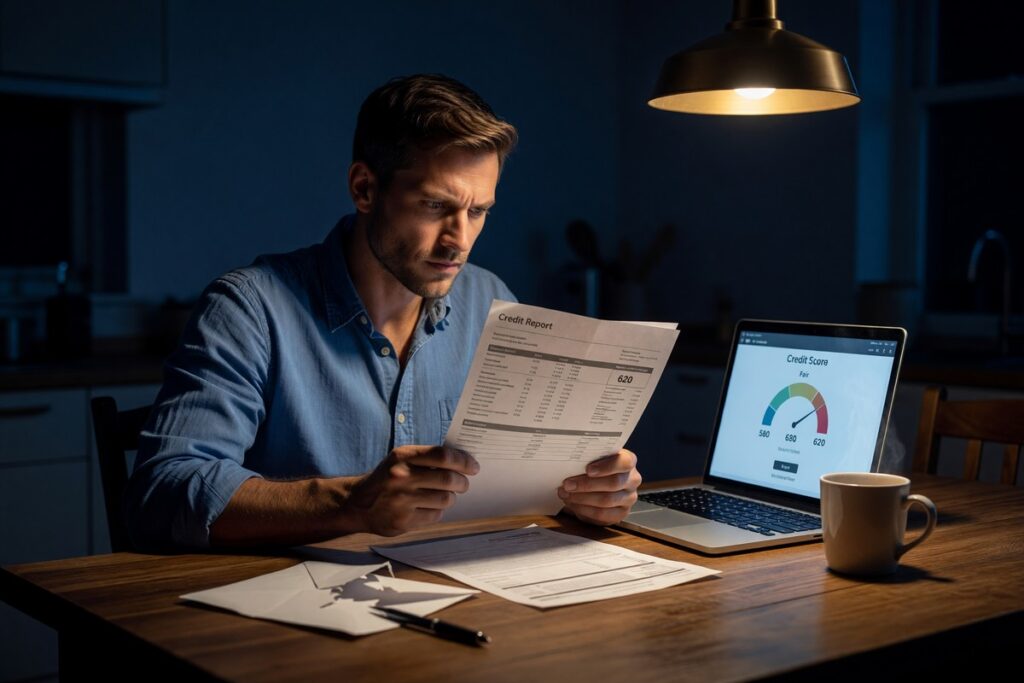

A 580 credit score cost can reach $5,000 or more annually through higher interest rates on loans, credit cards, auto financing, and insurance premiums. Borrowers with a 580 score pay interest rates 8–15 percentage points higher than those with good credit — a gap that compounds silently across every financial product they use.

The 580 credit score cost is not a single penalty. It is a layered tax applied across mortgages, auto loans, personal credit, and even your monthly insurance bill. According to the Consumer Financial Protection Bureau’s credit scoring resource, scores below 620 are typically classified as subprime, triggering the highest available rates from most lenders. A 580 score sits squarely in that danger zone.

What makes this costly is its invisibility. Most borrowers with a 580 score assume they are simply paying a little more. The actual annual loss, spread across multiple products, often exceeds what most people spend on groceries in two months.

Key Takeaways

- A 580 credit score costs borrowers an estimated $3,000 to $5,000 or more per year across loans, credit cards, and insurance, according to rate data from Experian and the Insurance Information Institute.

- Subprime personal loan APRs average 25% to 36%, versus 11–13% for borrowers above 720, per Experian’s lending data — a gap that adds more than $2,400 in extra interest on a single $10,000 loan.

- On a $250,000 mortgage, a 580-score borrower can pay $72,000 more in total interest over 30 years than a prime borrower, based on rate differentials tracked by Bankrate.

- Drivers with poor credit pay an average of 76% more for auto insurance than those with good credit, adding roughly $1,292 per year to premiums, per the Insurance Information Institute.

- Payment history accounts for 35% of a FICO Score, making consistent on-time payments the single highest-return action a 580-score borrower can take, according to myFICO.

- Conventional loans from Fannie Mae and Freddie Mac typically require a minimum 620 score, eliminating competitive pricing entirely for most 580-score mortgage applicants, per the CFPB mortgage resource.

What Does a 580 Credit Score Cost on Personal and Auto Loans?

Borrowers with a 580 credit score pay dramatically more for personal and auto loans than those in the “good” credit tier (670–739). The rate gap is not marginal. It is structural and persistent.

For personal loans, Experian’s lending data shows that borrowers with subprime scores (580–619) face average APRs between 25% and 36%, compared to roughly 11–13% for borrowers with scores above 720. On a $10,000 personal loan over 36 months, that difference adds up to more than $2,400 in extra interest.

Auto loans follow the same pattern. The average rate for a subprime auto borrower exceeds 14%, according to data tracked by the Federal Reserve’s consumer credit report. A prime borrower with a 750 score might secure the same loan at 6.5%. On a $25,000 vehicle financed over 60 months, that gap costs roughly $3,800 more in total interest.

The Compounding Effect Across Multiple Products

Most borrowers do not carry just one loan. They carry a car payment, a credit card balance, and possibly a personal loan simultaneously. Each of those products charges the subprime premium. The cumulative 580 credit score cost across all three can easily clear $4,000 to $5,000 per year.

There is another dimension here worth naming: rate fatigue. Borrowers paying subprime rates on multiple accounts often focus on making minimum payments rather than paying down principal, which is exactly what keeps the balances — and the interest charges — alive for years longer than necessary.

If you are already managing debt at these rates and considering short-term borrowing, understanding how short-term loan APR actually works is essential before signing any new agreement.

Key Takeaway: A 580 credit score adds an average of $3,800 or more in interest over the life of a typical auto loan compared to a prime borrower, according to Federal Reserve consumer credit data. That penalty repeats every time a new loan is opened.

How Does a 580 Credit Score Affect Mortgage Rates and Eligibility?

A 580 credit score severely limits mortgage options and inflates borrowing costs for the largest purchase most people ever make. The effect here is not measured in hundreds of dollars. It is measured in tens of thousands over a loan’s lifetime.

The Federal Housing Administration allows down payments as low as 3.5% for borrowers with scores at or above 580. Approval at that threshold, however, comes with mandatory mortgage insurance premiums and rates that are significantly higher than what a 700-plus borrower receives. A borrower with a 580 score taking a $250,000 FHA mortgage might pay an interest rate of 8.0–8.5%, while a borrower with a 760 score secures the same loan near 6.5%.

That 1.5 to 2 percentage point gap translates to roughly $220–$300 more per month in principal and interest. Over a 30-year loan, the 580 credit score cost on a single mortgage can exceed $72,000 in additional payments.

Conventional loans from Fannie Mae and Freddie Mac typically require a minimum score of 620, locking out most 580-score borrowers entirely from non-FHA products. That limited choice removes competitive pressure. When there is only one loan type available to you, lenders have little incentive to sharpen their pricing.

According to Bankrate’s analysis of credit scores and mortgage rates, the spread between subprime and prime mortgage rates has remained stubbornly wide, reflecting lenders’ persistent risk-based pricing at the lower end of the credit spectrum. That spread is not going to narrow simply because a borrower needs a home.

Key Takeaway: On a $250,000 mortgage, a 580 credit score can add $72,000 or more in total interest versus a prime borrower. Conventional loan programs from Fannie Mae and Freddie Mac typically require a minimum 620 score, eliminating rate competition for subprime applicants.

What Do Credit Cards Actually Cost at a 580 Score?

Credit cards available to 580-score borrowers carry the highest APRs in the consumer lending market. Most prime credit cards advertise rates between 20% and 24%, but those are rarely available to subprime applicants.

Borrowers with a 580 score are typically approved for secured cards, subprime unsecured cards, or store-branded products. These cards regularly charge APRs of 28% to 36%. Carrying an average balance of $3,000 at 30% APR costs $900 per year in interest alone, before a single new purchase is made.

Beyond the rate, 580-score cardholders face lower credit limits, which pushes up their credit utilization ratio. A high utilization ratio further suppresses the score, creating a self-reinforcing cycle that makes improvement harder. Understanding what your credit utilization ratio should be at every score range can help break that cycle.

| Credit Score Range | Typical Credit Card APR | Annual Interest on $3,000 Balance |

|---|---|---|

| 580–619 (Subprime) | 28%–36% | $840–$1,080 |

| 620–659 (Near-Prime) | 23%–27% | $690–$810 |

| 660–719 (Good) | 19%–22% | $570–$660 |

| 720–759 (Very Good) | 16%–19% | $480–$570 |

| 760+ (Exceptional) | 13%–16% | $390–$480 |

The annual difference between a 580-score cardholder and a 760-score cardholder carrying the same $3,000 balance can exceed $600 per year, just from the interest rate gap on one card.

Key Takeaway: A 580-score borrower carrying a $3,000 credit card balance pays up to $690 more per year in interest than a borrower with a 720+ score, based on typical APR ranges. Avoiding common credit-building mistakes is the fastest way to close that gap.

Does a 580 Credit Score Raise Insurance and Rental Costs Too?

Yes. The 580 credit score cost extends well beyond lending products. Insurance companies and landlords in most U.S. states use credit data to price risk and screen applicants.

Auto and homeowners insurance carriers use credit-based insurance scores, a related but distinct metric derived from your credit report. Drivers with poor credit pay an average of 76% more for auto insurance than drivers with good credit, according to the Insurance Information Institute. On a national average premium of roughly $1,700 per year, that means subprime-credit drivers pay approximately $1,292 more annually for the same coverage.

Rental housing adds another layer. Landlords running credit checks through TransUnion, Equifax, or Experian frequently reject applicants with scores below 620. When a 580-score applicant is accepted, they are often required to pay a larger security deposit, sometimes two months’ rent, locking up cash that earns nothing.

When rental options are limited and emergency costs hit simultaneously, borrowers often face pressure to turn to high-cost short-term products. Knowing how to distinguish predatory from fair lending before signing is critical in that moment.

Key Takeaway: Poor credit adds an average of $1,292 per year to auto insurance premiums, according to the Insurance Information Institute. That cost is invisible to most borrowers because it never appears on a loan statement.

What Else Gets More Expensive: Employment Checks and Utility Deposits

Most borrowers focus on the obvious costs — loan rates, insurance premiums, rental rejections. Two additional categories rarely make it into these conversations, and both hit borrowers below 620 consistently.

Employment Screening

Certain employers, particularly in finance, government contracting, and property management, run credit checks as part of background screening. A subprime credit profile does not guarantee rejection, but it can require additional documentation and explanation. For roles that involve handling money or sensitive client data, a 580-range score can become a deciding factor between two otherwise equal candidates.

The legal framework here is worth knowing. Under the Fair Credit Reporting Act, employers must obtain written consent before pulling a credit report, and they are required to provide a copy of the report and a summary of rights before taking adverse action based on it. That process takes time and creates friction that candidates with clean files simply do not face. For details on your rights in these situations, the CFPB’s credit reports and scores resource covers employer use of credit data directly.

Utility Deposits and Prepaid Service Requirements

Utility providers, including electric, gas, and telecommunications companies, routinely check credit before establishing service. Applicants with poor credit scores are frequently required to pay a security deposit ranging from one to three months of estimated billing. On a monthly electric bill of $150, that deposit can reach $450 paid upfront, held interest-free by the utility company for 12 months or longer.

Cell phone carriers impose the same logic. Postpaid contracts require credit approval. Applicants with a 580 score are often redirected toward prepaid plans, which typically cost more per month than the promotional contract rates available to prime-credit customers. This is a small per-unit cost, but across a 12-month period it is real money.

None of these charges appear as a line item labeled “credit penalty.” That is precisely why the total annual cost of a 580 score consistently surprises people when they add it up.

Why 580 Scores Persist: The Structural Traps

Understanding the mechanics of how a 580 score stays at 580 is as important as understanding what it costs. The score does not sit still by accident.

The Low-Limit Utilization Trap

Borrowers approved for cards at a 580 score typically receive credit limits between $300 and $500. Charging even a modest $200 in a billing cycle pushes utilization above 40%, which FICO’s model reads as elevated risk. The borrower may be paying on time every month and still watching their score stagnate or drop because the available credit ceiling is too low to demonstrate responsible usage at normal spending levels.

Credit utilization accounts for 30% of a FICO Score, per myFICO’s score education resource. A borrower with $300 in available credit and $150 in charges has 50% utilization regardless of their intentions. The only practical fix is to increase the credit limit or add a new account, both of which are harder to do when your score is already low.

The Collections Anchor

A single unpaid collection account can hold a FICO Score in the 500s for up to seven years from the original delinquency date. Many borrowers with scores around 580 have one or two collections that are years old but still active on the report. Even if the balance is relatively small, the presence of that entry signals recent or serious delinquency to scoring models.

Paying a collection does not always remove it from your report, though it will update its status to “paid.” The most reliable path to removal is a pay-for-delete agreement, which some smaller collectors will accept but larger debt buyers often will not. Disputing inaccurate collection entries through the bureaus is a separate, sometimes more productive strategy, particularly when the original debt has been sold multiple times and the documentation trail has gaps.

Hard Inquiry Accumulation

Borrowers with low scores often apply to multiple lenders to improve approval odds. Each application generates a hard inquiry. Multiple hard inquiries in a short window (outside of rate-shopping periods for mortgages or auto loans) reduce the score further, compounding the problem they were meant to solve. The irony is that the borrowers most likely to apply repeatedly are the ones least able to absorb additional score drops.

Key Takeaway: A subprime score does not just cost money directly. It creates conditions that make improvement structurally difficult, through low credit limits that inflate utilization, collection accounts that anchor the score down for years, and inquiry accumulation from repeated application attempts.

How Can You Realistically Reduce the 580 Credit Score Cost?

Moving from 580 to 670 is achievable in 12 to 24 months with disciplined, targeted action. The financial return is immediate once the score crosses key thresholds.

The most impactful short-term levers are payment history and credit utilization. Payment history accounts for 35% of a FICO Score, according to myFICO’s score education resource. A single missed payment can drop a 580 score by 60–80 points. Conversely, six consecutive on-time payments produce a measurable uptick for most borrowers.

Credit utilization, the ratio of balance to limit, accounts for 30% of a FICO Score. Keeping all cards below 30% utilization is the baseline. Below 10% is optimal. Adding a secured card or a credit-builder loan creates new positive history without requiring a high score to qualify. See the full comparison of secured cards versus credit-builder loans to determine which tool fits your situation.

Rent Reporting and Authorized User Status

Two underused strategies can accelerate improvement. Rent reporting services submit monthly rent payments to credit bureaus, adding positive tradeline history without new debt. Becoming an authorized user on a family member’s low-utilization card imports their positive history onto your report immediately.

These two strategies work best in combination with the basics. On-time payments and low utilization build the foundation. Rent reporting and authorized user status add breadth to a thin credit file that would otherwise take years to thicken on its own.

For renters specifically, rent reporting services remain one of the most overlooked credit-building tools available, particularly for those without traditional installment loan history.

Addressing Negative Items Directly

If collections are anchoring your score, identify which ones are within the dispute window and check for reporting errors first. Errors in collection accounts, including wrong balances, incorrect dates, or accounts that belong to someone else, are more common than most borrowers expect. The CFPB estimates that a meaningful percentage of credit reports contain errors material enough to affect scoring.

For accurate but damaging items, the timeline matters. A collection from six years ago carries less weight in FICO’s model than one from last year. Understanding which negative items are closest to falling off your report informs how aggressively to address each one versus simply waiting it out while building positive history in parallel.

Key Takeaway: Payment history drives 35% of a FICO Score, making on-time payments the single highest-ROI action a 580-score borrower can take. A 90-point gain over 12–18 months is realistic, according to myFICO’s credit education data.

What Changes Financially at 670: The Threshold Effect

The jump from 580 to 670 is not linear in its financial benefits. Crossing the 620 threshold opens access to conventional mortgage products, which introduces competitive pricing that subprime borrowers simply cannot access. Reaching 670 qualifies most borrowers for near-prime credit card offers, lowers auto insurance risk tiers, and substantially reduces personal loan APRs.

On the auto loan example used earlier, a borrower moving from a 580 to a 670 score might drop from a 14% rate to roughly 9–10%. On a $25,000 loan over 60 months, that change saves approximately $1,700 in total interest. The mortgage savings are larger still. Dropping from an 8.25% FHA rate to a 7.0% conventional rate on a $250,000 loan cuts the monthly payment by more than $200 and saves over $75,000 across the loan’s lifetime.

These are not aspirational numbers. They are the direct financial output of improving a credit score by roughly 90 points. That 90-point improvement requires no extraordinary income, no windfalls, and no loopholes. It requires consistent behavior across 12 to 24 months. The cost of not doing it, as this article has detailed, runs to several thousand dollars per year.

Frequently Asked Questions

How much more does a 580 credit score cost per year compared to a good score?

The total 580 credit score cost across loans, credit cards, and insurance typically ranges from $3,000 to $5,000 or more annually, depending on how many products a borrower carries. The largest single source of loss is usually an auto loan or mortgage, where rate differentials are widest.

Can I get a mortgage with a 580 credit score?

Yes, through FHA loans. FHA allows a 3.5% down payment at 580, but interest rates will be materially higher than prime-tier borrowers receive, and mandatory mortgage insurance premiums add further cost. Conventional loans from Fannie Mae typically require a minimum 620 score.

Does a 580 credit score affect my car insurance rate?

In most U.S. states, yes. Insurers use credit-based insurance scores, which are derived from your credit report. Drivers with poor credit pay an average of 76% more for auto insurance than those with good credit, according to the Insurance Information Institute. Only California, Hawaii, and Massachusetts prohibit the practice.

How long does it take to raise a 580 credit score to 670?

Most borrowers who address high utilization and maintain consistent on-time payments see a 60–90 point improvement within 12 to 24 months. The exact timeline depends on the negative items currently on the report. Collections, late payments, and high balances each require different strategies.

What credit cards are available at a 580 score?

Secured credit cards, credit-builder cards, and some store-branded cards are the primary options. These products typically carry APRs between 28% and 36% and lower credit limits. They are most useful as score-building tools when paid in full monthly, not as revolving credit lines.

Is a 580 credit score considered bad or just fair?

Under the FICO scoring model used by Equifax, TransUnion, and Experian, a 580 falls in the “poor” range (300–579 is poor; 580–669 is fair). Most lenders treat anything below 620 as subprime and apply subprime pricing, so the practical financial impact mirrors “bad credit” in terms of cost.

Do utility companies and employers check credit scores?

Many do. Utility providers routinely check credit before establishing service and may require security deposits from applicants with scores below 620. Certain employers, particularly in finance and government contracting, also run credit checks as part of background screening. Under the Fair Credit Reporting Act, employers must obtain written consent and follow specific procedures before taking adverse action based on credit data.