Fact-checked by the onlinepaydaynews.com editorial team

Quick Answer

Teachers and other borrowers facing emergency funding with a frozen credit score can still access funds through credit unions, income-based personal loans, and hardship programs, even with a security freeze in place. Lifting a freeze temporarily takes as little as 15 minutes online through Equifax, Experian, or TransUnion.

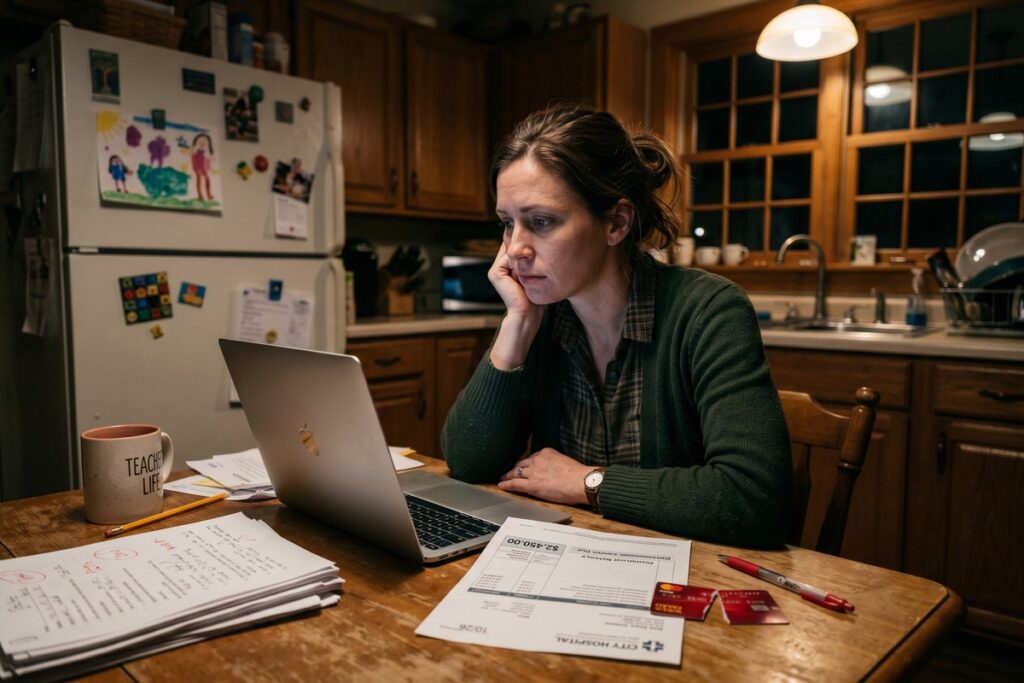

Emergency funding with a frozen credit score is possible, but only if you understand exactly which steps to take and in what order. According to the Consumer Financial Protection Bureau, a security freeze blocks new creditors from pulling your credit report, which can stop most conventional loan approvals cold. That single obstacle cost one California teacher nearly 72 hours of lost time during a $7,000 car and medical emergency, time she could not afford.

The good news: the same federal law that created free credit freezes also mandates that bureaus lift them within one business day of your request. Knowing that rule, and which lenders work around it, is the difference between a resolved crisis and a financial spiral.

Key Takeaways

- A security freeze blocks all new creditor inquiries at all three bureaus; most conventional lenders cannot approve a loan until the freeze is lifted, per the CFPB.

- A temporary freeze lift, not a full removal, opens your file to one specific creditor for a defined window, then automatically reinstates; it is free and available online at all three bureaus under the FTC’s 2018 freeze rules.

- Federal credit unions offer APRs between 9% and 14% for members with verifiable income, well below the national average personal loan APR of 21.57%, according to Credit Karma’s 2024 data.

- The FTC reported over 5.7 million identity theft reports filed in a single recent year, which is why many consumers carry active freezes they have forgotten about until a loan denial surfaces the issue.

- Per the Federal Reserve’s 2023 household financial wellness report, 37% of Americans could not cover a $400 unexpected expense without borrowing, a gap a small automatic savings habit directly addresses.

- Public-sector employees have a largely unknown option: many school districts and government agencies operate interest-free employee hardship advance programs repaid through payroll deduction, with no credit pull required.

What Is a Credit Freeze and Why Does It Block Emergency Loans?

A credit freeze, also called a security freeze, instructs the three major credit bureaus, Equifax, Experian, and TransUnion, to prevent new parties from accessing your credit file. Most traditional lenders require a hard inquiry to approve any loan. If your report is frozen, their request is rejected before a decision is even made.

Freezes became free nationwide in 2018 under the Economic Growth, Regulatory Relief, and Consumer Protection Act. They were designed to stop identity thieves from opening accounts in your name, a legitimate, widely used protection., the FTC reported over 5.7 million identity theft reports filed in the previous year, which explains why so many consumers now have active freezes without realizing how the restriction interacts with emergency borrowing.

The Difference Between a Freeze and a Fraud Alert

A fraud alert does not block lenders, it simply flags your file and asks creditors to verify your identity before opening new accounts. A freeze is a hard stop. Many borrowers, including the teacher in this scenario, placed a freeze after a data breach and forgot it was active until a loan denial triggered the discovery.

This distinction matters enormously in a time-sensitive situation. Borrowers who confuse the two tools can spend hours applying to lenders before realizing why every attempt is failing.

Worth understanding before any emergency: A credit freeze blocks all new creditor inquiries at all three bureaus simultaneously. Under the FTC’s 2018 freeze rules, lifting the freeze is free and can be done online in under 15 minutes per bureau, a critical first action in any emergency funding scenario.

How Did the Teacher Access Emergency Funding With a Frozen Credit Score?

She took four specific actions within 48 hours that collectively resolved the $7,000 shortfall, without a predatory payday loan and without waiting for a permanent unfreeze.

First, she contacted all three bureaus directly and requested a temporary lift, not a full removal, of her freeze. A temporary lift allows a specific creditor to pull your report within a defined window, typically 24 to 72 hours, after which the freeze automatically reinstates. This is a built-in federal feature most borrowers do not know exists. She then applied at her state employees’ credit union, which processed the inquiry and approved a $5,000 personal loan at 10.9% APR within 24 hours.

The remaining $2,000 gap was covered through her school district’s employee hardship fund, a program administered quietly by HR that provides interest-free advances repaid via payroll deduction. If you are a public-sector worker, this option is explored further in our guide on emergency funding options nonprofit and public-sector workers rarely know about.

The Sequence That Mattered

- Request a temporary freeze lift at Equifax, Experian, and TransUnion online or by phone.

- Apply at a credit union or community bank using income verification as the primary qualifier.

- Simultaneously contact HR or benefits administration about any employer hardship advance.

- Reinstate the freeze immediately after loan approval is confirmed.

One honest caveat about this approach: it works cleanly when you have existing membership at a credit union before the emergency hits. If you are not already a member, most federal credit unions have a brief enrollment process, but that adds time you may not have on day one of a crisis. Opening an account during a financial emergency is possible, though some unions require a small deposit and a waiting period before loan eligibility kicks in. For borrowers with no prior credit union relationship, a CDFI or employer hardship program may be a faster first move.

The temporary lift process itself also has a practical friction point. You will need the PIN or account credentials you set when the freeze was originally placed. Many people do not have these readily accessible, and account recovery through the bureaus can add several hours to an already stressful process.

The safest path to emergency funding with a frozen credit score is a targeted temporary freeze lift, not a full removal. Per NCUA guidelines, federal credit unions must disclose all loan options to members, including those with temporary credit restrictions, making them a top-tier first contact in a financial emergency.

Which Lenders Work Best for Emergency Funding in Frozen Credit Situations?

Not all lenders respond equally when a freeze is involved. The best options prioritize income verification and existing relationships over cold bureau pulls.

According to Credit Karma’s 2024 rate data, the average personal loan APR across all lender types is 21.57%. Credit unions consistently come in well below that average, often between 9% and 14%, for members with verifiable income, even when a freeze complicates the initial pull. Community Development Financial Institutions (CDFIs) offer similar flexibility and are specifically chartered to serve borrowers in financial distress.

For borrowers evaluating short-term options quickly, our comparison of credit union emergency loans vs. bank personal loans on payout speed breaks down exact processing timelines by lender type.

| Lender Type | Typical APR Range | Freeze Workaround Available |

|---|---|---|

| Federal Credit Union | 9% – 18% | Yes, temporary lift accepted |

| CDFI / Nonprofit Lender | 10% – 24% | Yes, income-based underwriting |

| Online Personal Loan (e.g., LightStream, Discover) | 7.99% – 28% | Partial, requires lift before application |

| Bank Personal Loan | 12% – 36% | Rarely, hard bureau pull required |

| Payday Lender | 300% – 664% APR | Yes, but at extreme cost |

Federal credit unions and CDFIs are the strongest emergency lenders for borrowers with frozen credit, offering APRs as low as 9% versus payday lenders that can exceed 300% APR. Always explore these before considering cash advance apps or high-cost short-term products.

What Mistakes Make Emergency Funding Situations Worse When Credit Is Frozen?

The most damaging mistake is applying to multiple lenders before lifting the freeze, generating a trail of soft denials that delay approval and waste critical hours. Each failed attempt with a frozen file can also trigger fraud flags at some institutions.

The second major error is fully removing the freeze rather than requesting a temporary lift. A full removal requires you to remember to reinstate it later, and most people do not. This exposes your credit file to risk during an already vulnerable period. The AnnualCreditReport.com portal managed by the three bureaus allows you to check the status of your freeze before applying anywhere, which takes under five minutes and prevents wasted attempts.

Third, borrowers in crisis often skip evaluating loan terms under pressure. Our guide on how to compare short-term loan offers without being misled by low APR claims is specifically designed for this scenario, when time is short but the cost of a wrong decision is high.

Signs You Are Looking at a Predatory Offer

- No freeze lift required, lender does not check credit at all

- APR disclosed only in fine print or after you apply

- Same-day funding with guaranteed approval regardless of income

- Fees structured as flat charges rather than expressed as APR

Removing a freeze permanently instead of requesting a temporary lift is a costly mistake during an emergency. The difference between predatory and fair lending often shows up in exactly these high-pressure moments, especially when lenders advertise no-credit-check approvals at triple-digit APRs.

How Can You Rebuild After Resolving an Emergency Funding With a Frozen Credit Situation?

Once the immediate crisis is resolved, two actions protect both your credit and your financial resilience going forward. The first is reinstating the freeze at all three bureaus immediately after the loan closes. The second is beginning to establish a small emergency reserve, even $25 per paycheck, which the Federal Reserve’s 2023 household financial wellness report found would have allowed 37% of Americans to cover a $400 unexpected expense without borrowing.

For borrowers who discovered during this process that their credit score needs rebuilding, adding positive tradelines is a powerful accelerant. Options such as rent reporting services and credit-builder loans are often overlooked. Our breakdown of unexpected ways to add positive accounts to your credit report covers several methods that do not require unfreezing your credit to get started.

Finally, document everything from the emergency: lender correspondence, freeze lift timestamps, and loan terms. If a lender behaved improperly during the process, the CFPB accepts complaints at no cost and has authority over most consumer lenders operating in the U.S.

After resolving a frozen-credit emergency, reinstate your freeze at all three bureaus immediately and begin a small automatic savings habit. Per the Federal Reserve’s 2023 data, just $400 in savings eliminates the need to borrow for the most common category of household emergencies.

Frequently Asked Questions

Can I get an emergency loan if my credit is frozen?

Yes. Request a temporary lift of your freeze at Equifax, Experian, and TransUnion before applying anywhere. A temporary lift is free, takes as little as 15 minutes per bureau online, and automatically reinstates your freeze after a set window, typically 24 to 72 hours. Federal credit unions and CDFIs are the most reliable lenders to approach once the lift is in place.

How long does it take to temporarily lift a credit freeze?

Online requests through each bureau’s website are typically processed within minutes. Phone requests must be completed within one business day under federal law. You will need your PIN or account credentials from when the freeze was originally placed, recovering those credentials can add time, so locate them before you are in crisis if possible.

What lenders approve loans with a frozen credit score?

Federal credit unions, CDFIs, and some online lenders will approve loans after a temporary freeze lift. Credit unions are the strongest first option, they offer the lowest rates and are most accustomed to working with members who have freeze-related complications during the inquiry process. Online lenders like LightStream and Discover can work as well, though they typically require the lift to be in place before you submit an application.

Does a credit freeze affect my existing accounts?

No. A freeze only blocks new inquiries from new creditors. Your existing credit cards, loans, and banking accounts continue to function normally. Current creditors can still access your file for account management purposes.

What is the difference between a temporary lift and removing a credit freeze?

A temporary lift opens your file to one specific creditor for a defined period, after which the freeze automatically restores. A full removal permanently unfreezes your file until you manually replace it. During a financial emergency, a temporary lift is always the safer choice, a full removal during a period of financial stress is precisely when identity thieves look for opportunity.

Can I get emergency funding with a frozen credit score and no savings?

Yes, but it requires a multi-step approach: lift the freeze temporarily, apply at a credit union or CDFI using income verification, and simultaneously check whether your employer offers a hardship advance or payroll loan. Combining these sources, as the teacher in this scenario did, can cover large gaps without resorting to high-cost products.

What if I don’t remember my credit freeze PIN?

Each bureau has an account recovery process through its website or by phone. Equifax, Experian, and TransUnion all allow identity verification through personal information on file, but recovery can take several hours. If you placed a freeze years ago after a data breach and have not logged in since, account recovery is likely the first practical obstacle you will face. Set aside that time before contacting lenders.

Is this approach realistic if I have a low credit score in addition to a frozen file?

It depends on the lender. A temporary lift gives a lender access to your file, but a very low score may still result in a denial or a high-rate offer. Credit unions and CDFIs are more flexible with credit scores than traditional banks, some CDFIs use income and employment history as the primary underwriting criteria rather than score alone. If your score is below 580, a hardship advance through your employer may be the most reliable path, since it typically involves no credit check at all.

Can a landlord or utility company see that my credit is frozen?

Potentially yes, and this matters in an emergency. If you need to establish new utility service or sign a lease quickly, a landlord or utility provider attempting a credit check will receive a frozen-file response rather than a score. You would need to place a temporary lift for those purposes as well, or provide alternative documentation of your payment history. This is a commonly overlooked scenario when people think only about loan applications.

Are there situations where this strategy does not work?

Yes. If you need funds within the same day, the temporary lift process, credit union application review, and funding disbursement may not clear in time, particularly on weekends or federal holidays when bureau phone lines have reduced hours. In those cases, an employer hardship advance or an existing personal line of credit (which is unaffected by a freeze) is a more realistic same-day option. The strategy outlined here works well within a 24-to-48-hour window; tighter timelines require different tools.