Fact-checked by the onlinepaydaynews.com editorial team

Quick Answer

To qualify for short-term loans after a job change, you need to document income continuity, not employer loyalty. Most short-term lenders require at least one pay stub or a verified offer letter, and keeping your debt-to-income ratio below 43% matters far more than how long you have been at your new job. Same-industry moves with equal or higher pay are rarely a problem.

Getting a short-term loan after changing jobs is achievable for most borrowers, and the process is far less punishing than conventional wisdom suggests. Unlike mortgage underwriters who scrutinize two-year employment histories under frameworks like Fannie Mae’s income documentation standards, short-term lenders focus on your current income, your debt-to-income ratio, and whether your earning trajectory is plausible, not whether you have spent years with the same employer. If you understand what signals lenders are actually reading, a recent job change becomes a manageable obstacle rather than a disqualifying one. This guide covers short-term loans and job change documentation as a standalone topic, separate from mortgage underwriting logic that dominates most competing advice.

The timing matters more than most borrowers realize., 22% of U.S. wage and salary workers had one year or less of tenure with their current employer, according to the Bureau of Labor Statistics Employee Tenure Summary (2024). Lenders know this. At the same time, the Federal Reserve Bank of New York’s 2024 Credit Access Survey found a 21% rejection rate among credit applicants, meaning nearly one in five people who apply gets turned down. Knowing how to position a job change correctly is the difference between joining that rejected group or not.

This guide is for anyone who has recently changed employers, is in the first months at a new job, or is about to start a new role and needs short-term financing now. By the end, you will know exactly which documents to gather, which loan types are most forgiving, and when it makes more sense to wait than to apply immediately.

Key Takeaways

- The median job tenure for U.S. workers is 3.9 years, the lowest since 2002, meaning lenders are increasingly accustomed to borrowers with short time at a current employer, per the BLS Employee Tenure Summary (2024).

- Short-term personal loans typically run 12 to 60 months, which means a lender needs income to hold for a fraction of the time a mortgage underwriter requires, a structural advantage for recent job-changers.

- The CFPB’s Appendix Q to Regulation Z explicitly allows projected income to qualify if a borrower is starting a new job within 60 days of closing under a guaranteed, non-revocable employment contract.

- Average personal loan APRs hit 19.8% in Q1 2024, up from 17.9% the prior year, per TransUnion data via Self Financial, making it critical to time your application well to avoid the highest-risk rate tier.

- Commission, bonus, and gig income after a job change faces a two-year documentation requirement at most lenders, while salaried base pay at a new employer can often be verified with a single pay stub or offer letter.

- Among all U.S. adults who applied for credit in 2024, one-third were denied or received less than requested, up 5 percentage points from 2021, according to the Federal Reserve’s 2024 Household Economics Report, reinforcing that documentation quality is a genuine differentiator.

In This Guide

- Why does changing jobs make it harder to get a loan?

- How do short-term lenders actually evaluate my employment after a job change?

- What documents can I use to prove income if I just started a new job?

- What factors can compensate for short job tenure when applying for a loan?

- Which types of short-term loans are most forgiving after a job change?

- Which job-change scenarios hurt my loan application most?

- What practical steps should I take before applying for a loan after changing jobs?

- Frequently Asked Questions

Step 1: Why Does Changing Jobs Make It Harder to Get a Loan?

Lenders are concerned about income continuity, not employer loyalty. A job change introduces uncertainty about whether current income will persist long enough to cover the loan repayment schedule, and that uncertainty shows up in how underwriters read your application.

How to Understand the Lender’s Core Concern

The fundamental question a short-term lender asks is not “how long have you worked there?” but rather “can you reliably repay this debt from your current income?” Those two questions often lead to very different conclusions. A borrower who changed jobs three months ago but earns a higher base salary in the same field poses a structurally lower risk than the underwriting narrative around job changes typically suggests.

Most competing content on short-term loans and job changes applies mortgage underwriting logic to a completely different product category. Fannie Mae’s guidelines, which require lenders to document income as “stable, with a history of receipt, and reasonably expected to continue,” are designed for 30-year home loans, not personal installment loans that are repaid in one to five years. A short-term lender extending a 24-month personal loan only needs your income to hold for 24 months, not 360. That shorter horizon genuinely changes the risk calculation.

What to Watch Out For

The most common mistake is assuming that because mortgage lenders scrutinize job changes intensely, all lenders do. They do not. A credit union underwriter reviewing a $5,000 personal loan application has far more flexibility than a mortgage processor following secondary-market guidelines. Setting false expectations in either direction, assuming approval is guaranteed or that rejection is inevitable, leads borrowers to skip documentation that would have helped or to give up on applications they would have won.

The CFPB’s Ability-to-Repay rule explicitly states that “stability of income takes precedence over stability of employment”, meaning a job change within the same field with advances in pay may actually be viewed favorably under federal underwriting standards, not treated as a red flag.

Step 2: How Do Short-Term Lenders Actually Evaluate My Employment After a Job Change?

Short-term lenders evaluate four specific signals when a borrower has recently changed jobs: income type, new-job tenure, industry continuity, and whether a probationary period is still active. Understanding each one tells you exactly where your application is strong and where it needs support.

The Four Signals Lenders Read

Income type is the most consequential variable. Salaried W-2 income at a new employer is the easiest to document and most readily accepted, often with a single pay stub. Hourly pay is nearly as straightforward. Commission-heavy or gig income after a job change is the hardest: most lenders require two years of documented variable earnings before they count it toward qualifying income. A borrower who moved from a salaried role to a commission-based one faces a specific documentation wall that does not apply to their salaried counterparts.

New-job tenure matters in a narrow but important way. Many lenders want to see at least one pay stub, which typically means at least two to four weeks on the job. Some online lenders will accept a verified offer letter with a confirmed start date, but that flexibility is not universal.

Industry continuity is arguably the most underappreciated factor. A lateral move from one company to another within the same field, even at a higher salary, is treated by most underwriters as a sign of career progression, not instability. Prior W-2s and tax returns establish the industry history that contextualizes the recent move. The FHA’s own employment guidelines under HUD 4155.1 instruct lenders to favorably consider borrowers who change jobs frequently within the same line of work if they continue to advance in income or benefits.

Probationary status is the factor most overlooked by borrowers. Many employers impose a 90-day or 180-day probationary period during which employment can be terminated with little notice. Lenders treat active probation as a period of uncertain employment status, and some will decline or defer an unsecured loan until it ends. However, if your offer letter explicitly waives probation, a detail many new hires do not read carefully, you are in a materially stronger position than someone whose letter is silent on the subject.

What to Watch Out For

There is a specific timing problem that almost no competing content addresses: the notice-period documentation gap. During the window between leaving your old job and receiving your first paycheck from your new employer, you may have no current pay documentation at all. Your most recent pay stub reflects the old employer, your new employer has not yet issued one, and income verification stalls. If you anticipate this gap, plan around it. Apply before you give notice, or wait until after your first paycheck clears.

If you switched from W-2 employment to 1099 contract or freelance work at your new job, most lenders will not count that income for qualifying purposes until you have two years of tax returns documenting it. This is the steepest cliff a job-changer can walk off, and it applies even if your gross earnings are substantially higher than before.

Step 3: What Documents Can I Use to Prove Income If I Just Started a New Job?

The right documentation package can substitute for time on the job. A signed offer letter, your first pay stub, employer verification of employment, and prior-year W-2s work together to tell a lender that your income is real, consistent with your history, and likely to continue.

The Core Documentation Bundle

Start with your signed offer letter. It should include your salary or hourly rate, your start date, the employing entity’s name, and any probation terms. This document alone can satisfy an initial income check at many online lenders. According to the CFPB’s Appendix Q guidelines, projected income is acceptable for qualifying purposes when a borrower is scheduled to start a new job within 60 days under a guaranteed, non-revocable employment contract, provided they have sufficient reserves to cover obligations until employment begins.

Add your first pay stub as soon as it is available. Even one pay stub shifts you from “projected income” to “verified income” in a lender’s system, which meaningfully reduces underwriting uncertainty. Some lenders who would decline based solely on an offer letter will approve once a single pay stub is in hand.

Your prior employer’s W-2s or tax returns for the most recent one to two years are the documents that establish industry continuity. They show a lender that your current role is not a leap into the unknown but a continuation of an established earnings trajectory. Bring at least two years if you have them.

Finally, provide an employer verification of employment (VOE) contact, typically an HR email or phone number that a lender can call or write to confirm your position. Under Fannie Mae’s verbal VOE requirements, lenders must complete this verification within 10 business days of the loan’s note date; short-term lenders often mirror this practice informally.

What to Watch Out For

Some online lenders accept a confirmed start date up to 90 to 180 days out as qualifying documentation. Others require at least one pay stub before making any decision. Know which category your lender falls into before submitting an incomplete package, because an application held for missing documents can result in additional hard credit inquiries that lower your score at the moment you most need it high. If you are unsure, ask the lender directly before applying. Many are happy to tell you their minimum documentation threshold.

Submit your full documentation bundle upfront rather than waiting for the lender to request items one at a time. A complete package signals transparency, reduces back-and-forth, and can accelerate approval by several business days. If you are navigating the process for the first time, read our guide on how fast emergency funding actually arrives by source so you can match your timeline to the right lender type.

| Loan Situation | Minimum Documentation Typically Required | Typical Approval Timeline | Probation Impact |

|---|---|---|---|

| New salaried job, same industry | Offer letter + first pay stub + prior W-2s | 1–3 business days | Low if offer letter waives probation |

| New job, different industry | 2 pay stubs + prior W-2s + letter of explanation | 3–7 business days | Medium; lender may wait for probation end |

| W-2 to 1099 / freelance switch | Two years of tax returns (not yet available if recent) | 7–14 business days or decline | High; variable income wall applies |

| Not yet started new job (offer letter only) | Guaranteed offer letter + proof of reserves (3+ months) | 2–5 business days | High; reserves must cover obligations until start |

| Gig / commission-based new role | Two years prior 1099 earnings documentation | 5–14 business days or decline | Very high; variable income cannot be projected |

Step 4: What Factors Can Compensate for Short Job Tenure When Applying for a Loan?

Three compensating factors carry the most weight with short-term lenders: a strong credit score, a low debt-to-income ratio, and documented cash reserves. A borrower who scores well on all three can offset nearly any employment timeline concern for a short-term product.

Credit Score as a Partial Substitute for Tenure

A strong credit score demonstrates willingness to repay, which is the other half of the credit decision, separate from ability to repay. For unsecured short-term loans where income verification is lighter than for secured products, a score above 700 gives an underwriter meaningful confidence independent of how long you have been at your new job. This does not eliminate the employment review, but it raises the approval threshold that shorter tenure needs to meet.

If your score has taken any recent hits, now is the time to review your report before applying. The quiet credit score killers that drag scores down often go unnoticed until an application surfaces them.

Debt-to-Income Ratio: The Number Lenders Actually Run

Debt-to-income ratio (DTI) is the metric underwriters rely on most heavily in short-term loan decisions. Most lenders cap qualifying DTI at 43–45%, though some online lenders extend to 50% for borrowers with strong credit profiles. A higher salary at the new job directly improves this ratio, and that improvement can offset a lack of tenure. A borrower who jumped from $55,000 to $75,000 in annual salary may actually present a better DTI picture after the job change than before, which is a concrete, defensible reason why a same-industry pay increase can strengthen an application rather than complicate it.

Cash Reserves: The Compensating Factor Most Borrowers Forget to Mention

Disclosing savings balances and liquid assets is a step many borrowers skip. Several months of reserves demonstrate that even if the new role does not work out, the borrower can cover payments during a transition. For a 12-month personal loan, showing three months of reserves is often sufficient to satisfy underwriter concern about employment continuity. Bank statements covering the most recent two to three months are the typical documentation lenders request.

What to Watch Out For

Do not assume a high credit score alone will carry the application. Lenders use both a credit review and an income review, and a deficiency in one cannot always be resolved solely by strength in the other. The combination matters. Also, never inflate asset disclosures. Lenders verify bank statements independently, and a discrepancy during underwriting creates delays, or worse, a fraud flag.

Average personal loan APRs reached 19.8% in Q1 2024, up from 17.9% in Q1 2023, per TransUnion’s Unsecured Personal Lending Industry Insights Report. Borrowers who apply at peak risk, immediately after a job change with incomplete documentation, may face rates at the higher end of this range. Improving your compensating factors before applying is one of the few levers you directly control.

Step 5: Which Types of Short-Term Loans Are Most Forgiving After a Job Change?

Not all short-term loan products apply the same employment scrutiny. Online personal installment lenders, credit union payday-alternative loans, and cash advance apps each use different underwriting frameworks, and their flexibility for recent job-changers varies considerably.

Ranking Loan Types by Flexibility for New Employees

Online personal installment lenders like Upstart and SoFi tend to be the most accommodating for job-changers, particularly when the move represents career advancement. Upstart’s lending model explicitly considers non-traditional signals including field of study, job offer letters, and career trajectory, meaning a borrower entering a higher-earning profession after a job change may receive better terms through that model than a traditional credit-score-only review would suggest. This is an angle that almost no other borrower guidance discusses, and it is a meaningful advantage for white-collar or credential-based career transitions.

Credit union payday-alternative loans (PALs) are administered under National Credit Union Administration rules and typically involve the most human underwriting discretion. A loan officer who can ask follow-up questions about a career move and receive a coherent answer is more likely to approve than an automated system that simply flags “tenure less than 90 days.” If you are a credit union member, this is the channel worth prioritizing for a short-term need after a job change.

Cash advance apps like Earnin, Dave, or Brigit operate differently from installment lenders entirely. They typically require a pattern of recurring direct deposits into a connected bank account, not employment tenure or income documentation. A borrower who has been at their new job long enough to receive one or two direct deposits may qualify for a small cash advance through these apps even before a traditional lender would consider them. The tradeoff is that advance limits are modest, typically $50 to $750, which may not cover the full need. For a detailed comparison of this option against installment products, the breakdown in this guide to cash advance apps versus emergency personal loans is worth reviewing before deciding.

Traditional banks and credit cards from established issuers apply the most conservative employment verification, often requiring 30 to 90 days of employment history at a minimum and running more rigorous income documentation checks. They are the least forgiving option for someone in the first weeks of a new job.

Community Development Financial Institutions (CDFIs) and employer-sponsored loan programs are underused alternatives for new employees who cannot yet document stable income. CDFIs are mission-driven lenders designed to serve borrowers underserved by conventional institutions. If your employer offers an employee lending benefit through a provider like Salary Finance or TrueConnect, it draws on employment verification through payroll systems rather than external income checks, potentially a faster path for someone three weeks into a job than any external lender would offer.

What to Watch Out For

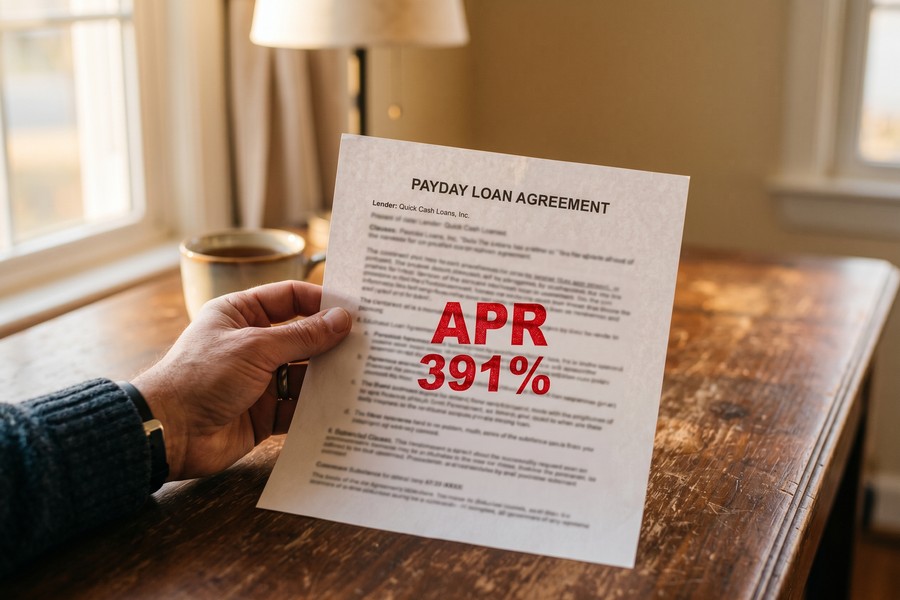

Payday loans, distinct from payday-alternative loans, carry extreme APRs and short repayment windows that are poorly suited to anyone with income uncertainty. They are not a suitable solution for a job-changer with documentation challenges. If you are weighing this option under financial pressure, see this comparison of paycheck advance apps versus traditional payday loans first, because the cost difference is substantial.

Step 6: Which Job-Change Scenarios Hurt My Loan Application Most?

Not all job changes read the same way to a lender. Some moves raise almost no concern; others create genuine approval barriers. Knowing where your situation falls helps you either apply with confidence or take targeted steps before submitting.

The High-Risk Moves

Switching from salaried W-2 employment to freelance or 1099 contract work is the single most damaging move for a loan application. Variable income at a new employer cannot be projected, and most lenders will not count it toward qualifying income without two years of documented earnings in that format. This gap is not a paperwork technicality, it is a structural limitation of how underwriting models handle unverified variable pay.

A complete industry pivot, leaving healthcare to work in construction, for example, also draws scrutiny, because prior W-2s and tax returns no longer establish continuity for the current role. Without industry history to contextualize the new job, the lender is assessing the role in relative isolation.

Accepting a new role with a low base salary and a large commission structure is the third high-risk category. Even if projected total compensation is higher, only the guaranteed base can be verified for underwriting purposes at the outset. A borrower earning $30,000 base with $40,000 in expected commissions looks, on paper, like a $30,000-a-year earner until two years of commission history accumulates.

The Low-Risk Moves

A same-industry lateral transfer or promotion at a new company, with equal or higher base salary, is treated as nearly a neutral event by most lenders. Prior employer W-2s establish the field, the new offer letter or pay stub confirms continuation and pay level, and the DTI calculation may actually improve if the salary went up. This scenario genuinely has minimal impact on a short-term loan application when documented correctly.

Recent graduates whose field of study directly matches their new role occupy a favorable position at lenders using alternative data models, including Upstart. The absence of prior W-2s in the field is expected for a first job out of school, and the degree itself functions as a career-continuity signal that traditional credit models miss entirely.

A Self-Assessment Framework

Run through three questions before you apply. First: does the new job pay a higher base salary than the old one? If yes, your DTI improves. Second: is the new role in the same general field or industry? If yes, prior W-2s establish continuity. Third: has your probationary period ended, or does your offer letter explicitly waive it? If yes to either, the lender’s primary concern about employment continuity is resolved. If you can answer yes to all three, your short-term loan application is in a strong position regardless of how recently you changed jobs.

If you have recently been denied a loan after a job change, review your denial notice carefully. Under the Fair Credit Reporting Act, you are entitled to know the specific reasons. Before reapplying, read about every next step available after an emergency loan denial, some fixes are faster than borrowers expect.

Step 7: What Practical Steps Should I Take Before Applying for a Loan After Changing Jobs?

Taking three to four focused steps before submitting an application significantly improves approval odds and can reduce the interest rate you are offered. The sequence matters as much as the actions themselves.

How to Prepare Your Application

First, time your application strategically. Waiting until after a probationary period ends, typically 90 to 180 days, removes the lender’s primary concern about income continuity for unsecured loans. If you have the flexibility to wait, this single decision often has the highest return. Completing probation typically costs nothing unless the financial need is urgent, and the reduction in perceived risk can translate to a meaningfully lower rate or higher approved amount.

That said, waiting is not always possible, and short-term loans carry a structural advantage that makes earlier applications more defensible than many borrowers realize. A lender extending a 12-month personal loan needs your income to hold for one year. A mortgage underwriter needs it to hold for thirty. That shorter horizon is a genuine, logical reason why job-changers have better odds with short-term products than the general advice on “job change and borrowing” implies.

Second, write a letter of explanation. This is a brief narrative, typically one paragraph, connecting your career move to your prior experience and income trajectory. An underwriter who reads that a software engineer left one employer for another at a $20,000 higher salary has a complete picture. One who only sees “six weeks at current employer” does not. The letter resolves questions before they become formal conditions or, worse, automated declines. Be direct and specific: include the previous employer’s name, years in the field, reason for the move, and current salary.

Third, shop lenders before applying. Hard credit inquiries from multiple applications can lower your score at the moment you need it highest. Use pre-qualification tools, which generate soft pulls that do not affect your score, to compare rates across lenders before committing to a full application. If you are not sure how different lenders present their offers, the guide on comparing short-term loan offers without getting fooled by low APR claims covers the specific traps to avoid.

Finally, check your credit report before any lender does. Errors on credit reports are common and can artificially depress your score. Reviewing your report through AnnualCreditReport.com before applying gives you the chance to dispute inaccuracies. If there are legitimate negative items, knowing about them in advance lets you address them in a letter of explanation rather than being blindsided during underwriting. For a fuller understanding of your dispute rights as a borrower, this guide to what most borrowers get wrong about their right to dispute a loan is a useful reference.

What to Watch Out For

Applying too early with an incomplete documentation package is the most common mistake. A lender who declines due to insufficient income verification may impose a waiting period before reconsidering, and the hard inquiry from that declined application affects your score. Better to spend three additional days gathering documents than to trigger a decline that follows you for six months.

Also consider whether a co-signer might solve the documentation problem entirely. If a creditworthy family member or partner is willing to co-sign, their stable employment history can substitute for yours in the underwriter’s income continuity analysis. The tradeoffs of this approach, including the risks to both parties, are covered in detail in this guide on short-term loans with a co-signer.

Quantify what waiting actually costs before you decide. If applying now results in a 23% APR on a $5,000 loan with a 24-month term, versus a 19% APR after waiting 90 days, the interest difference over the loan life is roughly $200 to $250. If the reason for borrowing is not urgent enough to justify that premium, waiting is the financially rational choice. If it is urgent, apply now with the best documentation package you can assemble.

Frequently Asked Questions

Can I get a short-term loan if I just started a new job and only have an offer letter?

Yes, some lenders will approve a short-term personal loan based on a confirmed offer letter alone, provided the letter is signed, specifies your salary and start date, and is non-revocable. The CFPB’s Appendix Q guidelines allow projected income to qualify if the start date falls within 60 days of loan closing. You will also typically need to show reserves covering several months of loan payments to demonstrate you can cover obligations until the first paycheck arrives. Not all lenders follow Appendix Q, ask directly before applying.

How long do I need to be at my new job before a lender will approve me?

Most short-term lenders require at least one pay stub, which means a minimum of two to four weeks on the job. Some online lenders with alternative data underwriting, including Upstart, may approve based on a verified offer letter before your first paycheck. Traditional banks and credit unions often prefer 30 to 90 days of employment history for unsecured personal loans. Completing your probationary period, typically 90 to 180 days, provides the strongest position and usually results in better rate offers.

Will switching from a salaried job to freelance work stop me from getting a loan?

Switching to freelance or 1099 work creates a serious short-term obstacle. Most lenders will not count variable self-employment income for qualifying purposes until you have two years of tax returns documenting it, regardless of how much you earn. During that window, you would need to qualify based on other factors, strong credit score, liquid reserves, or a co-signer with stable W-2 income. The situation is not permanent, but the two-year documentation requirement is a real ceiling that cannot be bypassed with a single pay stub or contract.

Does a same-industry job change hurt my loan application?

A same-industry move with equal or higher base pay has minimal impact on a short-term loan application when properly documented. Prior W-2s and tax returns establish your history in the field, and the new offer letter or pay stub confirms continuation. Under FHA employment guidelines and the CFPB’s ATR rule, income stability takes precedence over employer stability, meaning a career progression within the same field is explicitly supposed to be viewed favorably by underwriters.

What if I changed jobs and I am still in my probationary period?

Active probation raises a lender’s concern because employment during that window can typically be ended with minimal notice, making income continuity less certain. Some lenders will defer an unsecured loan approval until probation ends; others will proceed if the loan amount is modest and other compensating factors are strong. The most useful step is to check your offer letter for explicit language waiving probation, if it is there, include that document in your application package, because lenders treat a waived probationary period very differently from one that is still running.

Should I wait 90 days before applying for a short-term loan after starting a new job?

Waiting until after probation ends is the highest-leverage action most job-changers can take, but it only makes sense if the financial need is not urgent. Completing 90 days of employment removes the lender’s primary income-continuity concern and typically results in better rate offers and higher approved amounts. If you need funds immediately, apply with the strongest documentation package you can assemble, offer letter, any pay stubs received, prior W-2s, bank statements, and a letter of explanation, and understand that you may pay a modest rate premium for the timing.

Can a higher salary at my new job actually help my loan application?

Yes. A higher base salary directly improves your debt-to-income ratio, which is the primary metric lenders use in short-term loan decisions. If your monthly debt obligations stay the same but your income rises, your DTI drops, and a lower DTI can offset shorter tenure in the underwriter’s analysis. This is one of the genuinely underreported advantages of a job change with a pay increase: the borrower may qualify for a larger loan or a lower rate than they could have obtained at their previous salary, even with fewer days at the new employer.

What if I am denied a short-term loan right after a job change?

A denial is not permanent. Request the specific reasons in writing, lenders are required to provide them under the Equal Credit Opportunity Act. If the denial is documentation-related, gather the missing items and reapply after 30 to 60 days, or try a lender with different underwriting criteria. If your credit score contributed, avoid multiple rapid reapplications that add hard inquiries. For a structured approach to next steps, the guide on what to do after an emergency loan denial covers every recovery path in order of priority.

Are there short-term loan options that do not require employment verification at all?

Some cash advance apps, including Earnin, Dave, and Brigit, base eligibility on recurring direct deposit patterns rather than formal employment verification, which can help very new employees who have had at least one or two paychecks deposited. Secured loans backed by savings accounts or certificates of deposit also bypass income verification because the collateral covers the lender’s risk. Both options have meaningful limitations: advance amounts are typically small, and secured loans require pledging assets. Always verify a lender’s legitimacy before submitting any application, and use the CFPB complaint database to screen lenders in advance.

How do lenders verify my income at my new job if I do not have pay stubs yet?

Lenders can verify income through several channels when pay stubs are not yet available: a signed offer letter specifying salary, a verbal or written verification of employment (VOE) from your employer’s HR department, payroll account records through bank-linking services like Plaid, and prior employer W-2s that establish your earnings history. Some lenders use bank statement analysis as an alternative to traditional pay stubs, reviewing deposit history over 60 to 90 days to confirm income patterns. Ask your target lender which methods they accept before assuming pay stubs are the only path.

Sources

- U.S. Bureau of Labor Statistics, Employee Tenure Summary (2024)

- Federal Reserve Bank of New York, SCE Credit Access Survey (2024)

- Federal Reserve Board, Report on the Economic Well-Being of U.S. Households in 2024

- Consumer Financial Protection Bureau, Appendix Q to Regulation Z (12 CFR Part 1026)

- Consumer Financial Protection Bureau, ATR/QM Rule Small Entity Compliance Guide

- Fannie Mae Selling Guide, B3-3.2-01: Standards for Employment and Income Documentation

- Fannie Mae Selling Guide, B3-3.1-04: Verbal Verification of Employment

- FHA / HUD 4155.1, Employment and Income Documentation Requirements

- Self Financial, Personal Loan Statistics (TransUnion Unsecured Personal Lending Data, 2024)