Fact-checked by the onlinepaydaynews.com editorial team

Quick Answer

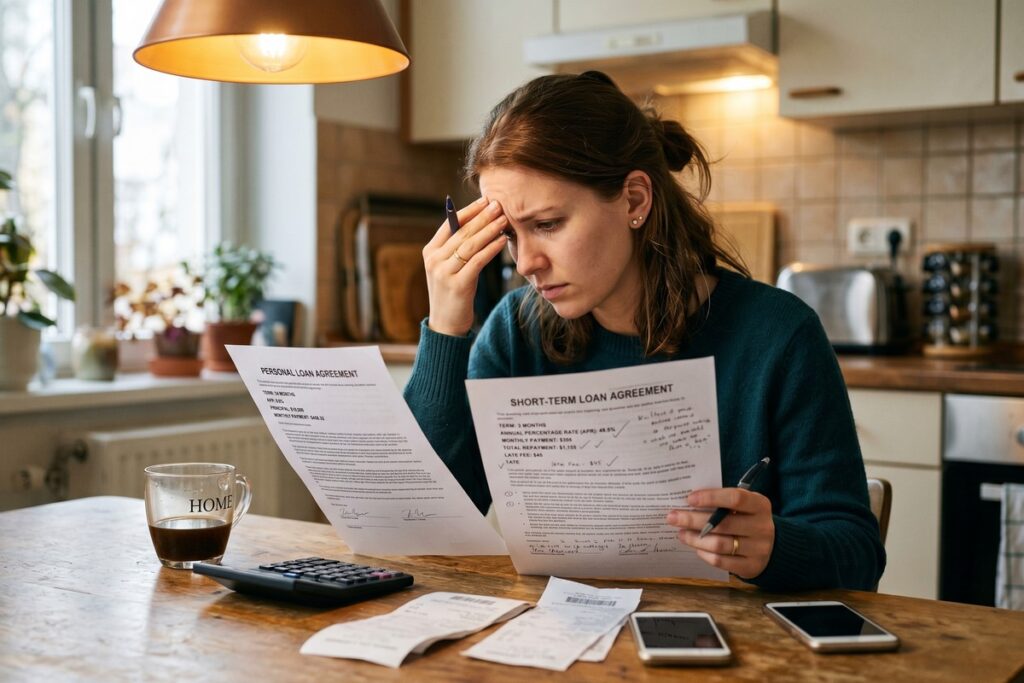

Personal loans almost always save you more money than payday loans. Personal loan APRs average 12%–36%, while payday loans carry effective APRs of 300%–400%. For any loan you cannot repay in days, a personal loan is the dramatically cheaper choice.

The cost difference between payday loans and personal loans is not marginal. According to the Consumer Financial Protection Bureau (CFPB), a typical two-week payday loan charges $15 per $100 borrowed, which translates to an annual percentage rate of nearly 400%. Personal loans from banks, credit unions, and online lenders charge a fraction of that.

With household budgets under sustained pressure, choosing the wrong loan type can trap borrowers in a debt cycle that takes months or years to escape.

Key Takeaways

- Payday loans carry effective APRs of 300%–400%, according to the CFPB, compared to 12%–36% for personal loans.

- Four out of five payday loans are rolled over or renewed within 14 days, per CFPB research, turning a short-term fee into a recurring cost.

- A $1,000 personal loan at 20% APR costs roughly $110 in interest over one year; equivalent payday loan rollovers over the same period would generate fees exceeding $3,000.

- Federal credit unions offer Payday Alternative Loans (PALs) with APRs capped at 28% under NCUA rules, providing a regulated lower-cost option for borrowers who cannot qualify for standard personal loans.

- 69% of payday loan borrowers use the funds for recurring expenses such as rent and utilities, not one-time emergencies, according to Pew Charitable Trusts research.

- Personal loans report on-time payments to Equifax, Experian, and TransUnion, building credit history; most payday loans do not report to major bureaus unless the borrower defaults.

How Do Payday Loans and Personal Loans Actually Differ?

Payday loans and personal loans are fundamentally different financial products designed for different situations. Payday loans are short-term, small-dollar loans, typically $100–$500, due in full on your next paycheck, usually within 14 days. Personal loans are installment products repaid over 12–84 months in fixed monthly payments.

Loan Structure and Approval

Payday lenders rarely check your credit score. Approval is based on proof of income and a bank account. Personal loan lenders, including banks like Wells Fargo and Chase and online lenders like LightStream and SoFi, perform a hard credit inquiry and evaluate your debt-to-income ratio.

This difference in underwriting is precisely why payday loans carry higher rates. Lenders price in the elevated default risk. Personal loan applicants with fair-to-good credit typically qualify for rates far below the payday loan threshold.

Key Takeaway: Payday loans are 14-day balloon-payment products; personal loans are installment loans spanning up to 84 months. The structural difference drives the entire cost gap. See the CFPB’s payday loan explainer for official definitions.

What Does Each Loan Actually Cost?

The cost gap between these two products is the single most important factor for any borrower. A $400 payday loan with a $60 fee sounds manageable until you cannot repay it and roll it over, adding another $60 every two weeks.

According to Federal Reserve consumer credit data, the average personal loan APR for a 24-month loan was approximately 12.35% in early 2025. By contrast, the CFPB reports that the median payday loan fee generates an APR of 391%. On a $400 loan carried for six months through rollovers, a payday borrower could pay $720 in fees alone, more than the original principal.

The Rollover Trap

The CFPB found that four out of five payday loans are rolled over or renewed within 14 days, meaning most borrowers pay repeated fees without reducing their principal. This is the mechanism that transforms a short-term bridge into a long-term debt spiral.

| Feature | Payday Loan | Personal Loan |

|---|---|---|

| Typical APR | 300%–400% | 12%–36% |

| Loan Amount | $100–$500 | $1,000–$100,000 |

| Repayment Term | 14 days (lump sum) | 12–84 months |

| Credit Check | None | Hard inquiry required |

| Funding Speed | Same day | 1–5 business days |

| Rollover Risk | High (80% roll over) | None (fixed schedule) |

| Credit Impact | Minimal (no bureau reporting) | Builds credit history |

Key Takeaway: The effective APR on payday loans is 10–30 times higher than on personal loans. The CFPB’s rollover data confirms that most borrowers pay far more than the original fee, making payday loans the costlier choice in virtually every scenario.

Who Qualifies for a Personal Loan?

Most borrowers who assume they cannot qualify for a personal loan are wrong. Credit unions and community development financial institutions (CDFIs) offer personal loans to borrowers with FICO scores as low as 580. Online lenders like Avant and Upgrade specialize in near-prime borrowers.

According to Experian’s credit score data, the average American FICO score is 715, well above the threshold most personal loan lenders require. Borrowers with scores in the 600–650 range can often secure a personal loan at rates far below payday alternatives.

Alternatives When Credit Is Poor

The National Credit Union Administration (NCUA) regulates federal credit unions, which are legally permitted to offer Payday Alternative Loans (PALs) with APRs capped at 28%. These are regulated products designed explicitly to replace payday loans. Employer-sponsored payroll advance programs and buy-now-pay-later services from providers like Earnin also offer lower-cost bridges for borrowers with limited credit options.

Research from the Pew Charitable Trusts Small-Dollar Loans Project has consistently found that consumers who turn to payday loans are often unaware that credit union payday alternative loans exist. The rate difference can mean hundreds of dollars saved on a single borrowing episode.

Key Takeaway: Federal credit union Payday Alternative Loans (PALs) cap APRs at 28% under NCUA rules, making them a regulated, accessible alternative for borrowers who cannot qualify for standard personal loans but want to avoid payday loan rates.

When Does a Payday Loan Ever Make Sense?

A payday loan is rational only in one narrow scenario: you need cash today, you are certain you can repay the full amount plus fees on your next paycheck, and you have exhausted all cheaper alternatives. This describes a very small fraction of actual payday loan users.

Pew Charitable Trusts research found that 69% of payday loan borrowers use the funds for recurring expenses like rent and utilities, not true emergencies. Most borrowers are using an extremely expensive product to fill a structural income gap, and rollovers will only deepen it. For anyone in this situation, a personal loan, a credit union PAL, or a negotiated payment plan with the creditor is the superior path.

For genuine emergencies, a personal loan funded within 24 hours by a lender like LendingClub or OneMain Financial will cost dramatically less even if your credit is imperfect. The speed gap between payday loans and online personal loans has narrowed considerably; same-day or next-day funding is now common among online installment lenders.

Key Takeaway: Payday loans are rational only for 14-day cash gaps with guaranteed repayment. Since Pew’s research shows 69% of borrowers use them for recurring expenses, a personal loan or PAL is almost always the smarter financial choice.

Which Loan Saves You Money: The Final Verdict?

Personal loans win on cost in every scenario lasting more than two weeks. The math is not close. A $1,000 personal loan at 20% APR over 12 months costs approximately $110 in total interest. The same $1,000 borrowed through sequential payday loans over 12 months, rolling over every 14 days, would generate fees exceeding $3,000.

Personal loans also build your credit profile. On-time payments are reported to Equifax, Experian, and TransUnion, improving your FICO score for future borrowing. Payday loans typically do not report to major credit bureaus unless you default, meaning they carry all the risk with none of the credit-building upside.

The Federal Trade Commission (FTC) explicitly warns consumers about payday loan fee structures and advises exploring personal loan alternatives first. That advice holds.

Key Takeaway: A $1,000 personal loan at 20% APR costs roughly $110 in interest over one year. Equivalent payday loan rollovers cost over $3,000. The FTC recommends exhausting personal loan options before turning to payday lenders.

Frequently Asked Questions

Are payday loans or personal loans easier to get approved for?

Payday loans are easier to get. They require no credit check, only proof of income and a bank account. Personal loans require a credit inquiry and review of your financial profile. However, borrowers with scores above 580 often qualify for personal loans through credit unions or online lenders.

What is the average APR for a personal loan vs a payday loan?

Personal loan APRs range from 12% to 36% depending on creditworthiness, according to Federal Reserve data. Payday loans carry effective APRs of 300%–400% when their flat fees are annualized. The gap makes payday loans one of the most expensive legal borrowing products available.

Can a payday loan hurt my credit score?

Taking out a payday loan typically does not directly affect your credit score because most payday lenders do not report to major credit bureaus. However, if you default and the account is sent to collections, it will appear on your credit report and damage your score.

How fast can I get a personal loan compared to a payday loan?

Payday loans are usually funded the same day or within hours. Personal loans from online lenders like LightStream or SoFi can fund in one to five business days. Some credit unions and online lenders offer next-day or same-day personal loan funding for qualified applicants.

What is a payday alternative loan (PAL) and how does it compare?

A Payday Alternative Loan (PAL) is offered by federal credit unions and regulated by the NCUA. PALs cap APRs at 28% and offer loan amounts from $200 to $2,000. They are specifically designed as a cheaper substitute for traditional payday loans and are available to credit union members.

Is it ever smart to choose a payday loan over a personal loan?

Only if you need cash in hours, cannot qualify for any personal loan product, and are certain you can repay the full amount by your next paycheck without rolling over. This scenario is rare. For most borrowers, a credit union PAL or even a credit card cash advance is a less costly option.