Fact-checked by the onlinepaydaynews.com editorial team

Marcus had been driving for two rideshare platforms and doing weekend furniture deliveries for about three years when his transmission gave out on a Tuesday morning. The repair estimate came back at $3,200. His checking account held $340. His credit card, the one he’d been leaning on during slow weeks, was maxed. And without that car, he had exactly zero income. Searching for a gig worker emergency loan that would actually approve a 1099 earner with no W-2 and a blown credit utilization ratio sent him down a rabbit hole that most financial guides don’t bother to map accurately.

The stakes for gig workers in this situation are genuinely high, and the numbers back that up. Research published by Commonwealth found that 70–80% of gig workers had $1,000 or less in savings, more than 40% had no savings at all, and three in four had experienced a financial hardship exceeding $1,000. That’s not a fringe problem. For millions of people who depend entirely on 1099 income, a single large expense can shut down their ability to earn at all.

This guide lays out exactly how to cover a large emergency when you have no W-2, a maxed card, and variable gig income. You’ll understand why banks decline you even when you’re actually earning well, which loan types are genuinely worth pursuing for a $3,200 need, which ones fall short and why, and what documents will give you the best shot at approval. By the end, you’ll have a ranked list of options and a step-by-step plan to act on today.

Key Takeaways

- Research from Commonwealth found that more than 40% of gig workers have zero savings, making a $3,200 emergency a realistic crisis, not an edge case.

- The Federal Reserve’s 2024 SHED report found that 37% of U.S. adults could not cover a $400 emergency from savings or a paid-off credit card, and gig workers fared worse than average.

- Cash advance apps typically cap first-time users at $200–$500, making them insufficient for a $3,200 need; most articles skip this detail entirely.

- Credit union Payday Alternative Loans (PALs) are federally capped at 28% APR and can be a serious first-stop option before turning to fintech lenders charging 36%.

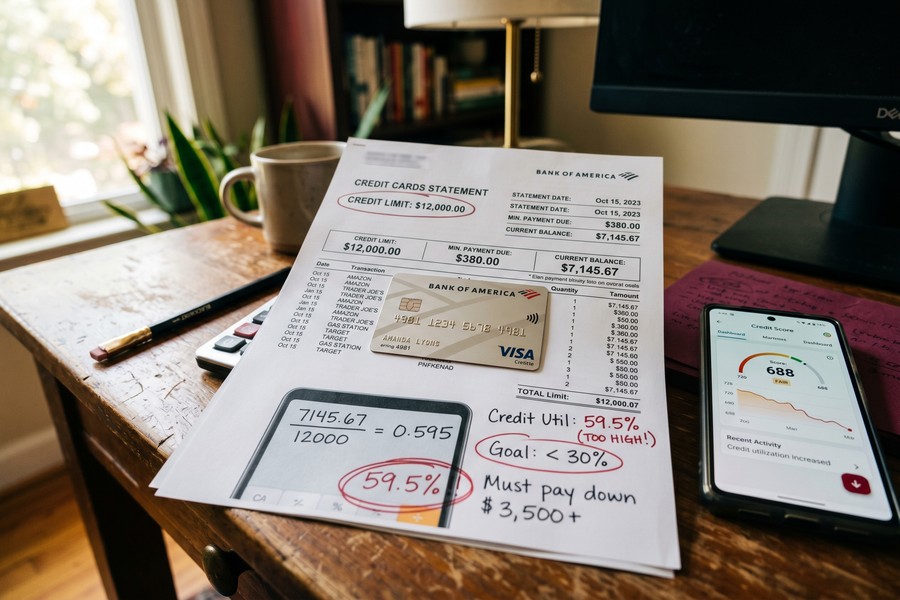

- A maxed credit card can drop a FICO score by 50–100 points through high utilization alone, even when every payment has been made on time.

- Online personal loans through bank-statement underwriters typically run 29–36% APR for fair-credit borrowers, versus the ~391% APR the CFPB documents for payday loans.

In This Guide

- Why a $3,200 Emergency Hits Differently When You’re a Gig Worker

- The Real Reason Banks Say No (It’s Not Personal)

- The Document Package That Actually Gets You Approved

- Your Real Loan Options When You Have No W-2 and a Maxed Card

- The Payday Loan Trap: Why Easy Approval Is the Most Dangerous Route

- How to Apply and Maximize Your Approval Odds Right Now

- After the Emergency: Building a Buffer So This Doesn’t Happen Again

Why a $3,200 Emergency Hits Differently When You’re a Gig Worker

A $3,200 emergency is painful for anyone. For a gig worker, it’s structurally different from the same crisis hitting a salaried employee. There’s no employer-sponsored sick leave to tap. There’s no unemployment insurance available if you can’t work for two weeks. Self-employment taxes eat 15.3% of net income off the top. And if the emergency involves your car, your earning tool is gone at the same moment the bills arrive.

The Federal Reserve’s 2024 Survey of Household Economics and Decisionmaking confirmed that gig workers were less likely than other adults to have paid all their bills the prior month, less likely to have three months of emergency savings, and nearly half wished their pay was more consistent. This isn’t a character flaw. It’s the design of gig work: maximum flexibility, minimum financial safety net.

The Compounding Problem Nobody Explains

What makes the situation compound quickly is that losing income and needing money happen simultaneously. A W-2 worker with a medical bill still gets a paycheck Friday. A rideshare driver with a broken transmission gets nothing until the car is fixed. That means the loan needs to cover both the emergency cost and the income gap during the repair period, which is why $3,200 can turn into a $4,500 problem in under two weeks.

According to Commonwealth’s research, three in four gig workers have experienced a financial hardship exceeding $1,000, and 79% said that hardship actually prevented them from working. The income loss from the emergency itself is often larger than the emergency expense. That’s the cycle that makes standard “build an emergency fund” advice feel tone-deaf when you’re in the middle of it.

The Federal Reserve’s 2024 household survey found that 31% of gig workers said they would have trouble making ends meet without their gig income, confirming that for a significant share of the gig workforce, this work is a financial necessity, not a side hustle. Source: Federal Reserve SHED 2024

The Real Reason Banks Say No (It’s Not Personal)

Traditional lenders built their underwriting systems around one assumption: income arrives as a predictable, employer-verified paycheck. W-2 earners fit cleanly into that model. Gig workers don’t, and the automated systems that review most loan applications aren’t designed to handle irregular deposits from multiple sources. The rejection often happens before a human ever looks at the file.

When a bank sees fluctuating deposits from three different platforms plus an occasional Venmo payment from a client, its system flags the account as high risk. There’s no employer to call. No HR department to verify employment. No consistent deposit schedule to model repayment from. The lender isn’t being unfair; it’s applying a framework that was built for a different kind of worker.

The Schedule C Trap Most Articles Ignore

Here’s something almost no guide mentions: gig workers who do their taxes correctly and aggressively write off business expenses, mileage, phone, platform fees, car maintenance, legally reduce their taxable income. That’s smart. But lenders calculating qualifying loan amounts use net Schedule C income, not gross deposits. A driver earning $60,000 in platform payouts who writes off $20,000 in legitimate expenses looks like a $40,000 earner to most lenders. The loan amount they qualify for shrinks accordingly, even though their actual cash flow supports much more.

This creates a direct conflict between good tax strategy and loan eligibility. It’s not fixable overnight, but knowing it explains why your application might get approved for $1,800 when you needed $3,200. The workaround is targeting lenders who underwrite on bank deposits rather than tax returns, which is covered in detail in the options section below.

What a Maxed Card Does to Your Score Beyond the Obvious

Credit utilization is the ratio of your current balances to your total available credit. A card at its limit pushes that ratio to 100% on that account. Credit scoring models penalize utilization above 30% significantly, and a maxed card can drop a FICO score by 50–100 points on its own, completely independent of whether you’ve ever missed a payment. So a gig worker with a spotless payment history but one maxed card can easily slide from “fair credit” into “poor credit” territory, which changes the loan products available and the interest rates attached to them.

Gig workers who are approved for personal loans face a notable approval gap. People with 1099 income are approved at roughly a 45% rate even with a 620+ credit score, compared to 67% for W-2 employees with equivalent scores. The income documentation problem, not creditworthiness itself, is rejecting nearly a third of otherwise qualified applicants. Choosing the right lender type matters more than waiting to improve your credit.

The Document Package That Actually Gets You Approved

If you walk into a loan application with only a tax return and hope, you’re likely to get declined. The document package that actually moves applications forward with 1099-friendly lenders is more specific than most guides describe, and assembling it before you apply rather than scrambling during the process can be the difference between a same-day approval and a week of back-and-forth.

What to Gather Before You Apply

The core documents most bank-statement lenders want are: three to twelve months of bank statements showing consistent deposits, 1099 forms from each platform you work with, in-app earnings summaries (Uber and Lyft both generate these directly in the driver app under earnings history), and your most recent Schedule C from your tax return. Freelancers with client relationships should also include any invoices showing recurring work.

One practical tip that makes a real difference: if your gig income flows through one dedicated checking account, lenders can read your deposit history cleanly. Mixed personal and business deposits in the same account create noise that slows underwriting and can raise questions about your actual gig income amount. If you haven’t separated accounts yet, it’s worth doing for future applications even if it doesn’t help this one.

Time your application strategically. Lenders typically analyze the most recent three to six months of bank deposits, not your annual average. If you’re a rideshare driver, summer months often produce higher volume. If you do retail delivery, Q4 peaks. Applying right after your strongest earning period gives the lender the most favorable recent picture of your income.

The CFPB advises borrowers to shop around and compare offers between multiple lenders before agreeing to any loan, advice that matters even more for 1099 earners, since eligibility and rates vary widely depending on how a given lender underwrites self-employed income.

Your Real Loan Options When You Have No W-2 and a Maxed Card

Not every borrowing option is built for a $3,200 need. Understanding which tools cover which dollar ranges, and at what cost, saves a lot of failed applications and wasted time. Here’s an honest stack-ranking by total cost and suitability for this specific situation.

Options That Can Actually Cover $3,200

Online personal loans from fintech lenders are the most practical path for most gig workers. Companies like Upstart, LendingPoint, and Prosper accept 1099 income documentation and bank statements in place of W-2s. APRs typically run 7–36% depending on credit profile, and funding can happen within one to three business days. For fair-credit borrowers in the 580–650 range with a maxed card, expect offers in the 29–36% range, but that’s dramatically better than the alternatives.

Revenue-based advances from gig-focused lenders like Giggle Finance and Fundo underwrite primarily on bank deposit history through Plaid connections rather than credit scores. A driver with consistent $4,000–$5,000 monthly deposits but a 580 credit score due to high utilization can qualify where a traditional lender auto-rejects. The honest trade-off here is that factor rates and fees on these products can be higher than a personal loan APR, so read terms carefully. For a genuinely fast funding need where credit score is the blocker, they’re a real option, but not a cheap one.

Credit union Payday Alternative Loans (PALs) are underused and genuinely underrated. Federally regulated and capped at 28% APR, PALs are available through most credit unions up to $2,000 in some cases. They don’t cover the full $3,200, but combining a PAL with another source might. Some credit unions also offer small personal loans to members with a history of direct deposits, even with poor credit. If you’re not already a credit union member, joining takes a few days but can be worth it for the rate difference alone.

If you want a sense of how fast each of these sources can actually deliver money, the breakdown by funding source at OnlinePaydayNews maps out realistic timelines for each borrowing type.

What Won’t Cover $3,200 (and Why Most Articles Skip This)

Cash advance apps like Dave, Brigit, and EarnIn are frequently listed as emergency solutions, but first-time users typically qualify for $200–$500 maximum. Even regular users rarely access more than $750. These apps are genuinely useful for small gaps, but they cannot cover a $3,200 repair bill. Applying and being declined wastes time you probably don’t have. Standard payday loans are similarly capped, often at $1,000 in most states, and come with costs that make them dangerous at any amount.

For a deeper look at how cash advance apps compare to personal loans for larger needs, this comparison of cash advance apps vs. emergency personal loans covers the numbers in detail.

| Option | Typical Amount Available | Typical APR | W-2 Required? |

|---|---|---|---|

| Online Personal Loan (fintech) | $1,000–$50,000 | 7–36% | No (bank statements accepted) |

| Revenue-Based Advance (gig lender) | $500–$25,000 | Varies (factor rates) | No (deposit history used) |

| Credit Union PAL | Up to $2,000 | Capped at 28% | No (membership required) |

| Cash Advance App | $200–$750 | 0% (tips/fees apply) | No (bank link required) |

| Payday Loan | $100–$1,000 | ~391% | No |

| Traditional Bank Personal Loan | $2,000–$50,000 | 6–25% | Usually yes |

The AFCPE recommends that gig workers maintain an emergency fund of 6–12 months of expenses rather than the standard 3–6 months recommended for salaried workers, specifically because of income volatility. Their guidance also cites Pew Research data that approximately 60% of gig workers call their earnings essential for meeting basic needs, which means the emergency fund target is higher, but the ability to save is also harder.

The Payday Loan Trap: Why Easy Approval Is the Most Dangerous Route

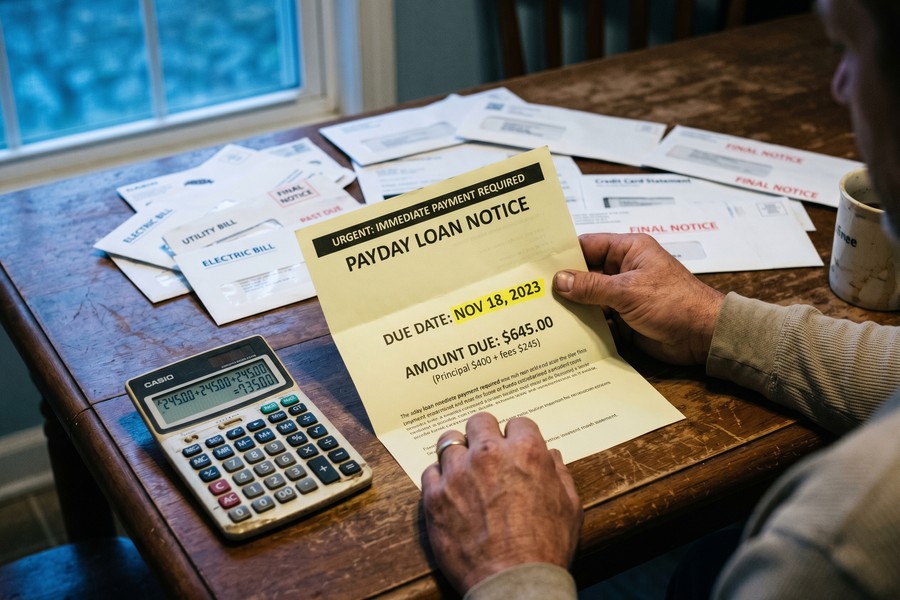

When you have a maxed card and a $3,200 problem, the appeal of any lender who says yes immediately is obvious. Payday lenders are often that lender. They don’t ask for W-2s. They don’t require a credit check in many cases. They sometimes fund the same day. And they are, by a wide margin, the most expensive money most people will ever borrow.

The CFPB’s examination of short-term, small-dollar lending documents that fees of $15–$20 per $100 borrowed translate to APRs of 391%–521% for typical two-week loans. On a $500 payday loan, that’s $75–$100 in fees due in two weeks. For a gig worker with variable income, clearing the full balance that fast is rarely realistic, which leads to rollovers.

How the Rollover Cycle Works Against You

A rollover means you pay the fee to extend the loan for another two weeks, but the principal doesn’t go down. The next fee is due again in two weeks. This cycle is how a $300 payday loan becomes $570 in fees over a few months without ever eliminating the original debt. Most payday lenders don’t report on-time payments to credit bureaus, so unlike a personal loan, you get no credit-building benefit from paying on time. There’s almost no upside.

The other issue specific to gig workers: payday loans are typically capped at $1,000 or less, which doesn’t solve a $3,200 problem anyway. So a borrower in this situation might take two or three separate payday loans from different lenders, stacking obligations that all come due within two weeks of each other during a period when they still may not have a working car. That scenario is how a manageable emergency becomes a multi-month financial crisis.

Before applying anywhere that promises easy approval, it’s worth checking lender legitimacy. The guide to spotting fake loan companies before you apply covers the specific red flags that distinguish predatory lenders from legitimate ones.

Some lenders market themselves as “gig worker friendly” while charging factor rates or fees that translate to triple-digit effective APRs. Revenue-based advances and merchant cash advance-style products for gig workers can be legitimate, but always ask for the total repayment amount and calculate the effective rate before signing. A product charging a “1.3 factor rate” on $3,200 means you repay $4,160, an effective APR that depends entirely on how quickly they withdraw from your earnings.

How to Apply and Maximize Your Approval Odds Right Now

The order in which you approach lenders matters. Applying to the wrong lender first can result in a hard credit inquiry that drops your score, reducing your odds at the next lender. A more deliberate sequence protects your credit while you find the right fit.

The Application Sequence That Protects Your Credit

Start with pre-qualification checks at online personal loan lenders. Pre-qualification uses a soft credit pull, which has no impact on your score. Upstart, LendingPoint, and Prosper all offer soft-pull pre-qual. You’ll see approximate rates and amounts without any credit score consequence. If pre-qual results look viable, then proceed with the full application, which involves a hard pull. Do this at one or two lenders at most, not five or six.

If your Schedule C net income is significantly lower than your actual deposits due to business write-offs, specifically target lenders that use bank-statement underwriting rather than tax-return income. This is worth confirming with the lender before applying, a quick chat with customer service asking “do you use bank statements or tax returns to verify self-employment income?” tells you whether it’s worth your time.

Consider asking for a slightly smaller amount than you think you need. Requesting $3,000 instead of $3,500 changes the lender’s risk calculation at the margin and can flip a decline into an approval, particularly if your debt-to-income ratio is close to the threshold. You can supplement the gap with a PAL from a credit union if needed.

The Co-Signer and Secured Loan Paths

Adding a creditworthy co-signer to a personal loan application can unlock approval when your credit score or income documentation alone wouldn’t qualify. For 1099 borrowers, this is a real option, but it puts the co-signer’s credit at risk if you miss payments, and that’s a fact to be honest about with anyone you ask. Only pursue this when you have a clear repayment plan and genuine confidence in your ability to follow through.

A secured personal loan, backed by a savings account or certificate of deposit, is close to a guaranteed approval path even with poor credit metrics. If you have $500–$1,000 sitting in savings somewhere, some credit unions will let you borrow against it at low rates with nearly no underwriting requirements. It’s not a solution if you have truly zero assets, but it’s underused by people who do have something to leverage without calling it that.

If your application gets denied despite good preparation, this guide on next steps after an emergency loan denial walks through exactly what to do rather than starting over from scratch.

Only 9% of U.S. adults earned money doing short-term gig tasks in 2024 according to the Federal Reserve’s annual household survey, but that’s roughly 23 million people, and a disproportionate share of them face the income documentation barriers described in this article when they try to borrow. Source: Federal Reserve SHED 2024

After the Emergency: Building a Buffer So This Doesn’t Happen Again

Getting through a $3,200 emergency with a loan is the short-term fix. The longer goal is making sure the next car repair, medical bill, or equipment failure doesn’t land the same way. That requires approaching savings differently than most general financial advice suggests.

Why “Three Months of Expenses” Isn’t Enough

Standard emergency fund advice targets three to six months of expenses. For gig workers, the AFCPE recommends six to twelve months, specifically because income volatility means slow periods can coincide with unexpected expenses. A slow December combined with a January car problem looks exactly like the scenario described above. The target is higher, which makes it harder to hit, but there’s a savings approach that fits the gig income pattern better than a fixed monthly transfer.

Automating a fixed percentage of every deposit, rather than a fixed dollar amount, fits the feast-or-famine income pattern. If you transfer 10% of every platform payout to a separate high-yield savings account, you save more in good months and less in slow ones without ever having to manually adjust or skip a transfer. A fixed $200/month fails in a $1,200 earnings month; 10% of $1,200 is $120, which is still progress without creating a shortfall.

The Protection Gap Nobody Warns You About

Only around 19% of gig workers carry disability insurance. Yet a single month of being unable to work, from illness, injury, or a broken-down car, is precisely the scenario that creates a multi-thousand-dollar emergency. Income protection insurance for self-employed workers is available through organizations like the Freelancers Union and some professional associations, often at lower cost than most gig workers expect.

Building credit during stable periods also expands your options when the next emergency hits. If you have a thin or damaged credit file, the comparison of credit builder loans versus secured cards for thin files gives a clear-eyed look at which approach builds a usable score faster. And if you’re trying to understand the full picture of how fees and lending terms affect you as a self-employed borrower, this guide on how freelancers can catch illegal lending fees is worth reading before you sign anything.

If your car is your earning tool, treat it like business equipment and build a dedicated vehicle repair fund separate from your general emergency savings. Even $50 per week adds up to $2,600 over a year, enough to cover most transmission repairs without borrowing at all. Name the account something specific so it doesn’t get raided for other expenses.

Your Action Plan

-

Assess your actual income documentation

Pull together three to six months of bank statements, your most recent 1099s, any in-app earnings summaries from your platforms, and your Schedule C from last year’s return. Knowing exactly what you have before you apply tells you which lenders to target and prevents surprises during underwriting.

-

Check your credit score and utilization

Get a free credit report from AnnualCreditReport.com and check your current utilization ratio. If your score has dropped specifically because of a maxed card, you’ll know that’s the primary issue, not your overall credit history, and you can target lenders who weight bank deposits more heavily than credit score in their approval decisions.

-

Start with soft-pull pre-qualifications at fintech lenders

Use the pre-qualification tools at two or three online personal loan lenders that accept self-employment income. This takes about ten minutes per lender, has zero impact on your credit, and tells you what rates and amounts are actually on the table before you commit to any hard inquiry.

-

Check credit union membership and PAL availability

If you’re already a credit union member, call and ask about Payday Alternative Loans or small personal loans for existing members. If you’re not a member, look for a local credit union with open membership requirements, some accept any resident of a particular city or state. A PAL at 28% APR for part of the amount is worth combining with a fintech loan for the remainder.

-

Target bank-statement underwriters if your Schedule C shows low net income

If you write off significant business expenses and your tax return net income is much lower than your actual deposits, specifically look for lenders that underwrite on deposit history rather than tax returns. Ask customer service directly before submitting an application. This single targeting adjustment can change a likely decline into an approval.

-

Apply to your best match and request only what you need

Submit a full application (with a hard pull) to the one or two lenders most likely to approve you based on your pre-qual results. Ask for the specific amount you need rather than rounding up. A smaller request is easier to approve and costs less in interest over the loan term.

-

Set up a percentage-based savings automation immediately after funding

The day you receive the loan and resolve the emergency, open a separate high-yield savings account if you don’t have one and automate a percentage-based transfer from every platform deposit. Start at 5% if 10% feels too aggressive. The goal is a system that runs without requiring willpower during slow months.

-

Verify any lender you use and know your borrower rights

Before signing any loan agreement, confirm the lender is licensed in your state and check for complaints in the CFPB database. If something about the terms seems off, this beginner’s guide to using the CFPB complaint database shows you exactly how to research a lender before you commit.

Frequently Asked Questions

Can I really get a loan with only 1099 income and no W-2?

Yes, though not from every lender. A growing number of online lenders and fintech companies accept bank statements, 1099 forms, and platform earnings summaries as income documentation in place of W-2s and pay stubs. The key is targeting lenders explicitly designed for self-employed or gig worker borrowers rather than applying to traditional banks that built their systems around employer-verified income.

Does a maxed credit card automatically disqualify me?

It doesn’t automatically disqualify you, but it affects your credit score significantly through high utilization, which can move you from “fair credit” to “poor credit” territory. Some lenders weigh bank deposit history more heavily than credit score, which can compensate for this. Being transparent about the situation and targeting the right lender type matters more than trying to quickly pay down the card before applying, you may not have time for that score to recover.

What’s the maximum a cash advance app will give me?

Most cash advance apps cap first-time users at $200–$500. Even with a long account history, most apps max out between $500 and $750. These apps are useful for small shortfalls between paydays but cannot cover a $3,200 emergency. Plan your application accordingly and don’t waste time on options that structurally can’t meet the need.

How long does it take to get funded through an online personal loan lender?

Most fintech personal loan lenders fund within one to three business days after approval. Some offer same-day or next-morning funding for applications submitted before a certain cutoff time. Approval itself can take minutes to a few hours for automated decisions, though lenders requiring manual review of self-employment income may take a day or two longer.

Are Payday Alternative Loans (PALs) actually accessible, or is it hard to join a credit union?

Credit union membership requirements have loosened considerably. Many credit unions accept members based on geographic location, employer, or even a small donation to an affiliated charity. Joining typically takes a few days and an opening deposit of $5–$25. Once you’re a member, PALs are genuinely available, federally capped at 28% APR, and much more consumer-friendly than most alternatives. They’re worth the minor effort to access.

What if my loan application gets denied?

A denial isn’t the end of the road, but your next move should be deliberate. Request the specific reason for denial in writing, lenders are required to provide this. If it was income documentation, gather better paperwork and apply to a lender with different underwriting criteria. If it was credit score, look at secured loan options or adding a co-signer. Rushing to apply at multiple lenders simultaneously risks multiple hard pulls and a further score drop.

Will a gig worker loan build my credit?

A personal installment loan from a reputable lender does report to the major credit bureaus and can build credit when paid on time. This is one concrete advantage over payday loans, which typically don’t report on-time payments. Making consistent, on-time payments on a personal loan while reducing your credit card balance can improve your score over the loan term, leaving you in a stronger position for the next emergency.

Is there any downside to using a bank-statement lender or revenue-based advance?

Yes, and it’s worth naming directly. Lenders who underwrite on deposits rather than credit scores often charge higher rates or factor fees to compensate for the additional risk they’re accepting. A revenue-based advance through a gig-focused lender might be approved quickly when a personal loan wouldn’t be, but the effective cost can be significantly higher. Always ask for the total repayment amount and calculate what percentage of your earnings the lender will take back and over what period.

Should I tell the lender why I need the money?

For most personal loans, lenders ask for a purpose (debt consolidation, emergency, car repair, medical) but don’t require documentation to verify it. Being straightforward about a car repair or emergency expense is fine and sometimes helps the lender understand the context. Avoid saying you’ll use the funds to pay off the same credit card you’re borrowing against, as some lenders treat that as a debt consolidation and apply different criteria.

How can I compare loan offers without getting fooled by low APR claims?

Focus on the total repayment amount and the monthly payment, not just the APR headline. Some lenders advertise a low starting rate that applies only to excellent credit borrowers, while the actual offer for fair-credit borrowers is much higher. Get the full loan terms in writing before agreeing. For a detailed breakdown of how to evaluate loan offers accurately, this guide on comparing short-term loan offers without getting misled by APR claims covers the specific tactics lenders use and how to see through them.

Sources

- Federal Reserve Board, Report on the Economic Well-Being of U.S. Households in 2024: Employment and Gig Work

- Federal Reserve Board, Report on the Economic Well-Being of U.S. Households in 2024: Savings and Investments

- Commonwealth, New Study Reveals Gig Workers Need Unique Benefits to Reduce Financial Challenges

- Consumer Financial Protection Bureau, What Is a Personal Installment Loan?

- Consumer Financial Protection Bureau, Short-Term, Small-Dollar Lending Examination Procedures

- Association for Financial Counseling and Planning Education (AFCPE), Financial Wellness in the Gig Economy: Empowering Flexibility With Stability

- Internal Revenue Service, Self-Employment Tax (Social Security and Medicare Taxes)

- Consumer Financial Protection Bureau, Consumer Complaint Database