Fact-checked by the onlinepaydaynews.com editorial team

Quick Answer

Getting an emergency loan with student loan debt is possible, but your debt-to-income ratio is the primary barrier, not your credit score. Lenders count student loans even when paused, deferred, or showing a $0 payment. Your best path: verify your reported payment, document your actual IDR amount, and approach campus emergency funds or credit unions before traditional banks. Most borrowers can complete this process in 2 to 7 business days depending on the lender type.

Applying for an emergency loan with student loan debt puts two pressure points in front of every lender at once: your credit history and your monthly debt obligations. The credit piece gets most of the attention, but the debt-to-income ratio is the reason most student loan borrowers hit a wall, even when their scores are solid. According to Federal Student Aid data compiled by BestColleges, the average federal student loan borrower carries $39,375 in outstanding debt, and at standard repayment terms, that translates to a monthly payment of roughly $400 to $430, claiming a significant slice of DTI capacity before rent or any other obligation is counted.

The timing makes this problem sharper than usual. The SAVE repayment plan has been legally frozen since mid-2024, federal collections on defaulted loans restarted in May 2025, and the Federal Reserve Bank of New York reported that 15.6% of federal student loans were past due by the end of the repayment on-ramp in October 2024, totaling over $250 billion in delinquent debt held by 9.7 million borrowers. Lenders are aware of this environment and are underwriting student loan borrowers more cautiously than at any point in recent memory.

This guide is for anyone carrying federal or private student loans who needs emergency cash now and wants to understand exactly how lenders evaluate their application, which options actually work given their repayment status, and where the honest limits are when adding more debt is not the right answer.

Key Takeaways

- Student loans are counted in your DTI even when deferred or in forbearance. Experian confirms that lenders may use 1% of your outstanding balance as a proxy monthly payment if your loan is paused, regardless of what you are actually paying.

- In 2024, 20% of student loan borrowers were behind on payments or in collections, according to the Federal Reserve’s 2024 SHED report, up from 16% the year before, which is prompting lenders to tighten underwriting for this borrower group.

- Delinquent student loans cause severe credit damage. The Century Foundation found that borrowers with past-due student loans saw scores drop by an average of 57 points in the first three quarters of 2025, with most pushed into subprime territory.

- Campus emergency funds bypass DTI calculations entirely because they are institutional aid, not credit-based lending. Many schools offer $500 to $3,000 interest-free with processing times of 2 to 3 business days, making them the most DTI-friendly option for enrolled borrowers.

- A 2025 Bankrate survey found that 59% of Americans cannot cover an unexpected $1,000 expense from savings, meaning most people facing an emergency are borrowing, not spending reserves, making it critical to choose the right borrowing channel.

- Borrowers whose federal loans are already in default face a practical disqualifier: federal collections restarted in May 2025, and the resulting credit damage makes most private emergency lending inaccessible. Loan rehabilitation, which requires nine consecutive on-time payments, is the prerequisite before new borrowing becomes realistic.

In This Guide

- Step 1: What Lenders Actually See When You Apply With Student Debt

- Step 2: How Your Repayment Status Changes the Math for a New Lender

- Step 3: The DTI Problem and Why Student Borrowers Hit a Wall

- Step 4: Emergency Borrowing Options That Actually Work for Student Loan Borrowers

- Step 5: How Your Student Loan History Helps or Hurts Your Application

- Step 6: Steps to Take Before You Apply That Visibly Improve How Lenders See You

- Step 7: When Emergency Borrowing Makes the Situation Worse and What to Do Instead

- Frequently Asked Questions

Step 1: What Lenders Actually See When You Apply With Student Debt

When a lender evaluates your emergency loan application, they pull two things above all else: your credit score and your debt-to-income ratio. With student debt, DTI is almost always the bigger barrier, and it affects borrowers regardless of whether they are actively repaying, deferred, or in administrative forbearance.

How Lenders Read Your Student Loan Profile

Your student loans appear on your credit report as active liabilities the moment they are disbursed, and they stay there through every repayment status: active repayment, income-driven repayment, deferment, and forbearance. A lender reviewing your file sees the outstanding balance, the payment history, and the current status. What many borrowers do not realize is that lenders rarely accept a $0 payment at face value.

According to Experian’s guidance on student loans and DTI, lenders are required to include student loan obligations in DTI calculations, and when a loan is in deferment or forbearance, they will often substitute the actual payment with a proxy figure, typically 0.5% to 1% of the outstanding balance. On a $39,375 balance, that proxy can land between $197 and $394 per month. That is a monthly obligation the borrower is not currently paying, but which a lender treats as real.

The 2025 policy environment adds another layer of complexity. With the SAVE plan frozen and interest accruing again on those balances since August 2025, borrowers who thought their payments were managed are now watching balances grow. Lenders evaluating applications from these borrowers are not looking at a static picture. They are underwriting a moving target.

What to Watch Out For

Do not assume your current monthly payment, whatever appears on your bank statement, is what a lender will plug into their DTI formula. The figure used in underwriting may be higher. Before applying anywhere, check what your student loan servicer reports as your monthly payment and compare it to your actual disbursements. If there is a gap, you have work to do before submitting an application.

The CFPB’s Student Loan Borrower Survey found that nearly 42% of federal student loan borrowers had only ever used the standard repayment plan, with many unaware that income-driven repayment options could lower their monthly obligations and improve their borrowing profile for new credit applications.

Step 2: How Your Repayment Status Changes the Math for a New Lender

Your loan repayment status directly changes the number a lender will use when calculating your DTI, and that number varies significantly depending on whether your loans are in active repayment, income-driven repayment, deferment, or forbearance. Understanding which category you fall into, and what assumption lenders will apply, is the foundation of knowing what you can actually qualify for.

How to Do This

Compare your situation to the four common scenarios:

- Active standard repayment: Lenders use your actual monthly payment as reported by your servicer. This is the most straightforward calculation.

- Income-driven repayment (IBR or active plans): Lenders can use the documented IDR payment if you provide proof from your servicer. Per Fannie Mae’s Selling Guide, this documented payment is accepted, but you must provide the documentation. If your credit report shows a different figure, the lender may use the higher one by default.

- Deferment: Competitors often treat deferment as a neutral status. It is not. A deferred loan is actively included in DTI calculations. Lenders impute 0.5% to 1% of the outstanding balance as a proxy monthly payment. A $60,000 deferred balance means a lender may assume $300 to $600 in monthly obligations you are not currently paying.

- SAVE administrative forbearance: This is the specific trap created by the 2025 policy freeze. Your payment shows as $0 on your credit report, but personal and emergency lenders routinely impute 0.5% to 1% of the balance anyway, creating a hidden DTI penalty. The borrower has no idea this is happening, and it sinks applications that would otherwise qualify.

For borrowers currently in SAVE forbearance, proactively switching to IBR before applying for an emergency loan can give a lender a documented, verified monthly payment that is lower than the imputed balance method they would otherwise use. This is one of the most concrete, actionable steps available right now, and almost no other guide mentions it.

What to Watch Out For

The SAVE plan’s interest resumption in August 2025 means that waiting also costs you money on the balance itself. Borrowers who stay in SAVE forbearance without a plan are watching their DTI assumptions grow as their balance increases. The window to switch to a stable income-driven plan, currently IBR or the incoming Repayment Assistance Plan (RAP) under the College Cost Reduction Act, is time-sensitive.

If your loans are in SAVE administrative forbearance, do not assume a $0 payment will help your emergency loan application. Many personal lenders will impute a monthly payment equal to 0.5% to 1% of your outstanding balance regardless of what your credit report shows, silently raising your DTI without any disclosure to you before the denial.

Step 3: The DTI Problem and Why Student Borrowers Hit a Wall

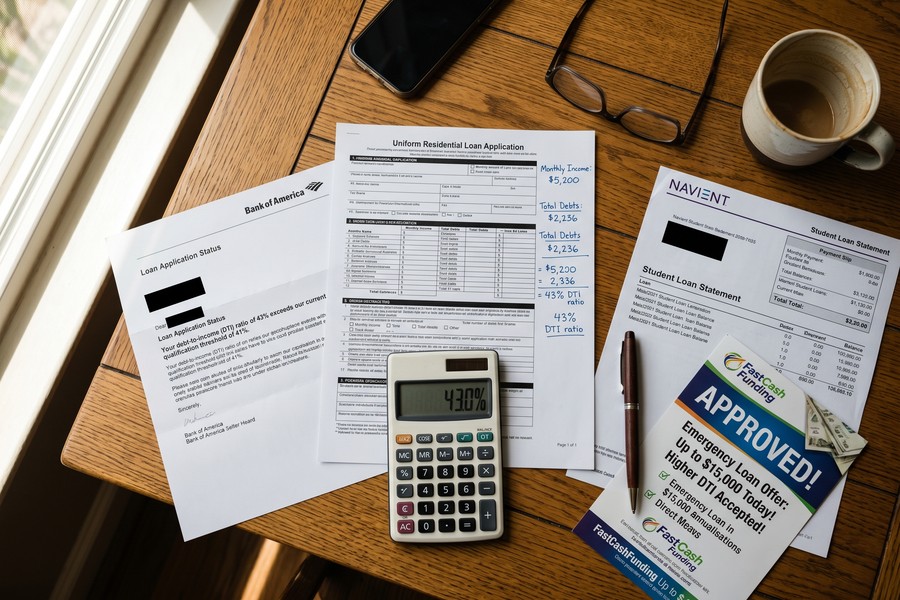

Most personal and emergency lenders cap acceptable DTI at 40% to 45%. The math for a typical student loan borrower is unforgiving, and this is where applications die even when the credit score is fine.

How to Do This

Run your own DTI calculation before any lender does. Add up all monthly debt obligations: student loan payment (or the proxy a lender will use), minimum credit card payments, auto loan, any other installment loans. Divide that total by your gross monthly income (before taxes). The result is your DTI percentage.

Consider a concrete example. A borrower earning $4,500 per month gross has $350 in student loan payments and $200 in credit card minimums. That is $550 in existing debt, or about 12% DTI. An emergency personal loan of $5,000 at a 24-month term might add another $260 per month, bringing total DTI to roughly 25%. That is manageable. Add a car payment of $400, though, and the borrower is at 34% before the new loan, and 40% after. Most lenders have approved that application at the very edge of their limit, with no cushion remaining.

The problem compounds for borrowers with larger balances. Someone with $80,000 in student debt on a 10-year standard plan carries a monthly payment near $840. On a $4,500 gross income, that single debt consumes 18.7% of DTI capacity before any other obligation is counted.

What to Watch Out For

Different lender types apply DTI thresholds differently, and this is one of the most actionable distinctions in this space. A borrower rejected by a traditional bank at 43% DTI may still qualify through a credit union or an online income-based lender that allows DTI up to 50%. The same financial profile can produce completely different outcomes depending purely on where the application is submitted first.

Borrowers with delinquent student loans saw their credit scores fall by an average of 57 points in the first three quarters of 2025, with three-quarters pushed into deep subprime territory, according to the Century Foundation’s 2025 report on student loan delinquency.

| Lender Type | Max DTI Allowed | Typical Loan Range | How Deferred Loans Are Treated | Approval Speed |

|---|---|---|---|---|

| Campus Emergency Fund | No DTI check (institutional aid) | $500 to $3,000 | Not applicable, bypasses DTI entirely | 2 to 3 business days |

| Federal Credit Union | Up to 50% | $500 to $25,000 | Uses documented IDR payment or 1% proxy | 1 to 5 business days |

| Online Income-Based Lender | Up to 50% | $1,000 to $15,000 | Uses 0.5% to 1% of balance if deferred | Same day to 2 business days |

| Traditional Bank Personal Loan | 36% to 43% | $1,000 to $50,000 | Uses 1% proxy per Fannie Mae guidelines | 1 to 7 business days |

| Payday or High-Rate Lender | No stated cap (income-verified) | $100 to $1,500 | Minimal review, but APR often 300%+ | Same day |

Step 4: Emergency Borrowing Options That Actually Work for Student Loan Borrowers

The best emergency loan option for a borrower with student debt depends on enrollment status, current repayment situation, and how much time the crisis allows. Ranked by DTI impact and cost, campus emergency funds are the clear first stop, followed by credit unions, and then online income-based lenders. Traditional banks and payday lenders sit at opposite ends of a spectrum, and neither is usually the right first choice for this borrower profile.

How to Do This

Campus emergency funds are the most underused option in this space. Schools like UC Berkeley offer up to $3,000 interest-free, while Georgia Tech caps the amount at $1,500 per semester. Processing typically runs 2 to 3 business days. Because these are institutional grants or short-term zero-interest advances, they do not trigger a credit check, carry no origination fee, and bypass the DTI calculation entirely. For an enrolled borrower with existing student debt, this is the most cost-efficient option by a wide margin. Check your school’s financial aid office or bursar’s website under “emergency funds” or “short-term loans.”

Federal credit unions are the next realistic tier. They tend to use income-based underwriting more flexibly than commercial banks and have shown willingness to approve DTIs up to 50% for borrowers with verifiable steady income. The National Credit Union Administration (NCUA) insures member deposits and provides an additional layer of consumer protection. You need to be a member to apply, but many federal credit unions allow immediate membership through a small deposit.

Online income-based lenders focus on cash flow rather than strict DTI formulas, making them viable for borrowers whom a traditional bank would decline. Some lenders in this category connect bank account data through Plaid or similar services to verify income directly, sidestepping the DTI wall that a large student loan balance creates. The trade-off is typically a higher interest rate than a credit union would offer.

For a broader look at how quickly each of these options delivers funds, the breakdown in this guide on how fast you can actually get emergency money by funding source provides useful timing benchmarks across each channel.

What to Watch Out For

Payday lenders sit at the bottom of this list for a reason. Their APRs often exceed 300%, and a short repayment window on top of an already strained budget creates a cycle of re-borrowing that worsens DTI over time. If you find yourself looking at this option, the guide on cash advance apps versus emergency personal loans walks through the real cost difference.

If a campus emergency fund is available to you, apply there first regardless of how small the amount sounds. A $1,500 interest-free advance from your school eliminates a chunk of the emergency without touching your DTI, and leaves your borrowing capacity intact if you still need a small personal loan to cover the rest.

Step 5: How Your Student Loan History Helps or Hurts Your Application

Student loans have a double-edged effect on credit scores, and their net impact on an emergency loan application depends entirely on how your repayment history looks. A clean payment record on student loans is actually a significant asset. A delinquency record is close to disqualifying.

How to Do This

Payment history accounts for 35% of a FICO score, and student loans, which often span 10 to 25 years, give lenders a long track record to evaluate. A borrower who has made consistent on-time payments for five years on a $40,000 loan has built a meaningful positive history that most other credit products cannot replicate at that scale. This actively improves emergency loan approval odds and may earn better interest rates than a borrower with a shorter payment history would receive.

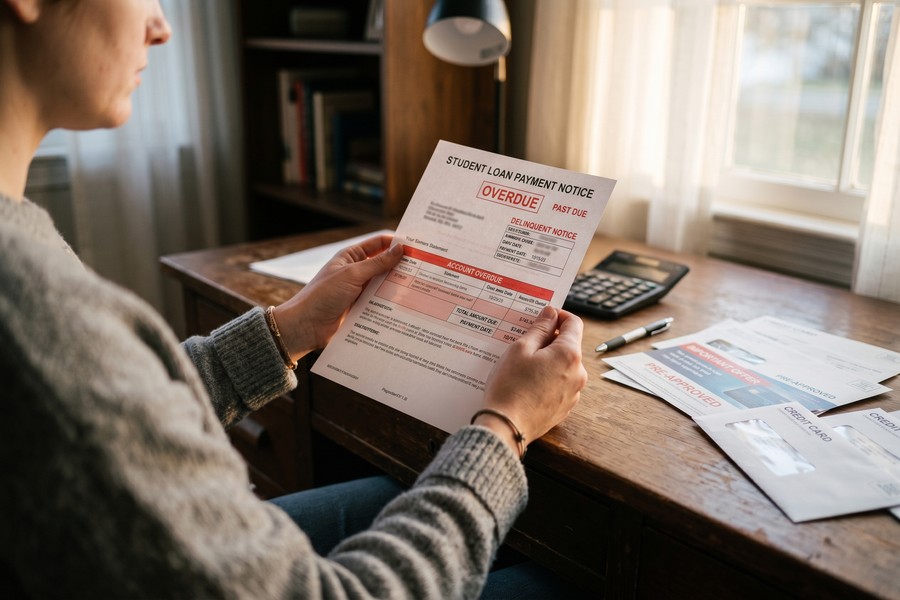

The reverse is equally sharp. According to the Federal Reserve’s 2024 SHED report, 20% of student loan borrowers were behind on payments or in collections for one or more loans in 2024, up from 16% in 2023. A single 90-day late payment on a student loan can drop a FICO score by 50 points or more, enough to push a borderline applicant out of the approval window for most personal loan products.

Default is a separate category. Borrowers whose federal loans were reported to collections after collections restarted in May 2025 face credit damage that makes most private emergency lending essentially inaccessible. At that point, loan rehabilitation through the Department of Education (not a new loan) is the prerequisite step. Rehabilitation requires nine consecutive on-time rehabilitation payments before the default notation is removed and borrowing eligibility is restored.

The Century Foundation’s 2025 analysis noted that emergency loans used responsibly can bridge temporary gaps without creating long-term financial strain, but borrowing more on top of delinquent student debt does not solve an underlying repayment problem. It defers it while adding cost.

What to Watch Out For

If you have student loans with a mixed payment history, pull your credit reports from all three bureaus through AnnualCreditReport.com before applying. Errors in how your repayment history is reported are more common than most borrowers expect, and a disputed error can sometimes be resolved within 30 to 45 days, potentially before a formal application. The guide on common mistakes borrowers make when disputing credit reporting errors covers the process in detail.

Step 6: Steps to Take Before You Apply That Visibly Improve How Lenders See You

There are concrete, documented actions that change how a lender calculates your DTI and evaluates your risk before you submit a single application. Taking these steps first can be the difference between an approval and a denial that also leaves a hard inquiry on your credit report.

How to Do This

Follow this sequence before submitting any formal application:

- Pull your credit report and verify the student loan payment figure. If your IDR payment is lower than what appears on the report, or if your loan is in deferment but the balance is large enough to generate a significant proxy payment, a lender is using an inflated number. A letter from your loan servicer on official letterhead stating your actual monthly payment can correct this in an underwriter’s file.

- Switch to an active repayment plan if you are in SAVE forbearance. IBR is currently the most stable IDR plan with a long-term future. Enrolling and documenting a verified monthly payment, even if it is $100 or $150, gives a lender something concrete to use instead of the 0.5% to 1% imputed figure. The CFPB’s repay student debt guidance tool walks through eligibility for every current repayment option.

- Use soft-pull prequalification only. Many online lenders advertise soft-pull prequalification but switch to a hard inquiry when you proceed to a formal application. Multiple hard inquiries in a short window can suppress a score that student debt may already be straining. Check each lender’s terms explicitly before proceeding past the prequalification stage.

- Calculate your DTI honestly before applying. Use the proxy payment your lender will likely apply (1% of outstanding balance if deferred), not the amount you actually pay. If your calculated DTI exceeds 45%, target credit unions or income-based lenders rather than traditional banks.

- Gather income documentation proactively. Pay stubs covering the last 60 days, tax returns for the prior year, and bank statements showing 90 days of deposits all help income-based lenders underwrite your actual cash flow rather than relying solely on the DTI formula that student debt distorts.

What to Watch Out For

Some emergency lenders advertise approvals without credit checks, which can sound appealing to a borrower already stressed about credit. These are almost always high-rate products, and several carry fee structures that obscure their true cost. Before engaging with any lender you have not researched, the guide on spotting fake loan companies before you apply provides specific red flags to check first.

If you are considering adding a co-signer to strengthen your application, know that this approach has specific conditions where it helps and others where it backfires. The detailed guide on emergency borrowing with a co-signer covers when the strategy is worth pursuing and when it creates more risk than it resolves.

Step 7: When Emergency Borrowing Makes the Situation Worse and What to Do Instead

An emergency loan layered on top of existing student debt that is already stretching DTI can create a compounding problem rather than solve one. This is the honest part of the guide that most articles skip, and it is the section most relevant to borrowers whose loans are already delinquent or whose DTI is already at its ceiling.

How to Do This

Apply a simple stress test before committing to any new loan: if you add the proposed monthly payment to your current obligations, what does your DTI become? If the answer exceeds 50%, or if you are already missing student loan payments, a new loan is not a solution. It is additional pressure on a system already under stress.

For borrowers in this position, several non-debt alternatives deserve consideration before any loan application:

- Tuition payment plans through your school’s bursar. Many institutions offer installment plans on outstanding tuition balances at no interest or minimal fees. This is a direct alternative to emergency borrowing for academic-related costs.

- Cost-of-attendance appeal for additional federal aid. If your financial circumstances have changed since the original aid package was calculated, a formal appeal to the financial aid office can unlock additional federal grant or subsidized loan eligibility.

- State and local emergency hardship funds. These are grant-based, not loan-based. They do not affect DTI, do not require repayment, and are systematically underused. State 211 networks and local nonprofit databases are the fastest way to find what is available in your area.

- Federal loan rehabilitation for defaulted borrowers. If your loans are already in default and collections have resumed, the Department of Education’s rehabilitation program is the correct first step, not an emergency loan search. Completing nine consecutive rehabilitation payments removes the default notation and restores access to income-driven repayment options.

What to Watch Out For

If your DTI is already above 45% and your student loans are delinquent, no legitimate emergency lender is a realistic option in the short term. Acknowledging this clearly is not defeatist. It directs limited time and energy toward steps that can actually change the situation: rehabilitation, IDR enrollment, and institutional aid rather than loan applications that will be declined and leave hard inquiries on an already damaged credit report.

Borrowers with defaulted federal loans who apply for private emergency loans are likely to be denied and leave hard inquiries that further suppress their scores. Federal loan rehabilitation, which restores credit standing after nine consecutive on-time payments, is the prerequisite step before private emergency borrowing becomes a realistic option for this group.

Frequently Asked Questions

Can I get an emergency personal loan if I have student loan debt and my DTI is already at 40%?

It depends on the lender type. Traditional banks typically cap DTI at 36% to 43%, so a borrower already at 40% has very little room before a new payment pushes them over the limit. Credit unions and online income-based lenders may approve DTIs up to 50%, meaning the same borrower could qualify if the new loan’s monthly payment keeps total DTI below that threshold. Calculate the new DTI first, then apply only to lenders whose limits match your actual number.

Do student loans in deferment count against me when I apply for an emergency loan?

Yes, deferred student loans are actively included in DTI calculations by virtually every lender. Rather than using a $0 payment, lenders impute a proxy monthly obligation equal to 0.5% to 1% of your outstanding balance. On a $60,000 deferred balance, that means a lender may assume a $300 to $600 monthly payment that you are not currently making, silently reducing how much new debt you can qualify for.

Will my SAVE plan forbearance hurt my emergency loan application?

It can, and in a way most borrowers do not expect. Your credit report shows a $0 monthly payment while in SAVE administrative forbearance, but personal lenders routinely override that figure with an imputed payment of 0.5% to 1% of your outstanding balance. Switching to IBR and documenting a verified monthly payment before applying gives a lender a concrete number to use that is often lower than the imputed figure, improving your DTI calculation on paper.

What happens if I apply for an emergency loan with a defaulted student loan on my credit report?

Defaulted student loans cause severe credit damage, typically pushing borrowers into subprime score territory where most private emergency lenders will not approve applications. Federal collections restarted in May 2025, compounding this damage for affected borrowers. The practical path forward is federal loan rehabilitation through the Department of Education, not a new loan search. Rehabilitation takes nine consecutive on-time payments to complete, after which the default notation is removed.

Which type of lender is most likely to approve an emergency loan when I have significant student debt?

Campus emergency funds are the most accessible for enrolled borrowers because they bypass DTI calculations entirely as institutional aid. After that, federal credit unions are the most flexible, accepting DTIs up to 50% and using income-based underwriting. Online income-based lenders also accommodate higher DTIs but typically charge more in interest. Traditional banks are the most restrictive, with hard DTI caps and less flexibility around deferred or paused loan treatment.

Should I pay off some of my student loan balance to improve my chances of getting an emergency loan approved?

Not as an emergency strategy. Using cash to pay down a large student loan balance right before applying for an emergency loan reduces the very resources you are trying to replace. The more targeted approach is correcting how your loan payment is reported to lenders, either by documenting your actual IDR payment or switching from SAVE forbearance to an active repayment plan. These steps change the DTI calculation without depleting cash reserves.

How does my student loan payment history affect my emergency loan interest rate?

A long record of on-time student loan payments actively improves your credit score and, by extension, the interest rate a lender offers on a new loan. Payment history makes up 35% of a FICO score, and student loans with multi-year clean records carry real weight with lenders. Conversely, even a single 90-day late payment on a student loan can drop a score by 50 or more points, which shifts a borrower into a higher risk tier and increases the rate offered, sometimes significantly.

Are there emergency loan options specifically for borrowers with student debt who have no savings?

A 2025 Bankrate survey found that 59% of Americans cannot cover a $1,000 emergency from savings, so this is a very common situation. Enrolled borrowers should check campus emergency funds first. Beyond that, income-based online lenders and credit unions are the most realistic options. State and local emergency hardship grants, which are non-repayable, are underused alternatives worth pursuing before taking on any new debt. The guide on what to do when your emergency loan application is denied covers additional options in this situation.

Can having student loans in good standing help me qualify for a better emergency loan rate?

Yes, meaningfully so. Lenders view a long-standing student loan with a clean payment history as evidence of responsible credit management at a significant balance. Combined with a stable income and DTI below 40%, that history can qualify a borrower for personal loan rates in the 10% to 15% range rather than the 20% to 30% range that thinner credit files typically see. Documenting your full payment history and ensuring it is accurately reported on all three credit bureaus before applying maximizes this advantage.

Sources

- Federal Reserve Board, Report on the Economic Well-Being of U.S. Households in 2024: Higher Education and Student Loans

- BestColleges, Average Student Loan Debt Statistics (Federal Student Aid Data, 2025)

- Federal Reserve Bank of New York, Liberty Street Economics, Credit Score Impacts from Past-Due Student Loan Payments (March 2025)

- Federal Reserve Board, Report on the Economic Well-Being of U.S. Households in 2024: Savings and Investments

- The Century Foundation, Trump’s Student Loan Delinquency Crisis, Unmasked (2025)

- CBS News, Bankrate Emergency Savings Report 2025: 59% of Americans Can’t Cover a $1,000 Expense

- Fannie Mae Selling Guide, Section B3-6-02: Debt-to-Income Ratios

- Experian, How Student Loans Affect Your Debt-to-Income Ratio

- Consumer Financial Protection Bureau, CFPB Survey Reveals Impacts of Student Loan Debt Relief and Repayment Challenges

- Consumer Financial Protection Bureau, Repay Student Debt Guidance Tool