Fact-checked by the onlinepaydaynews.com editorial team

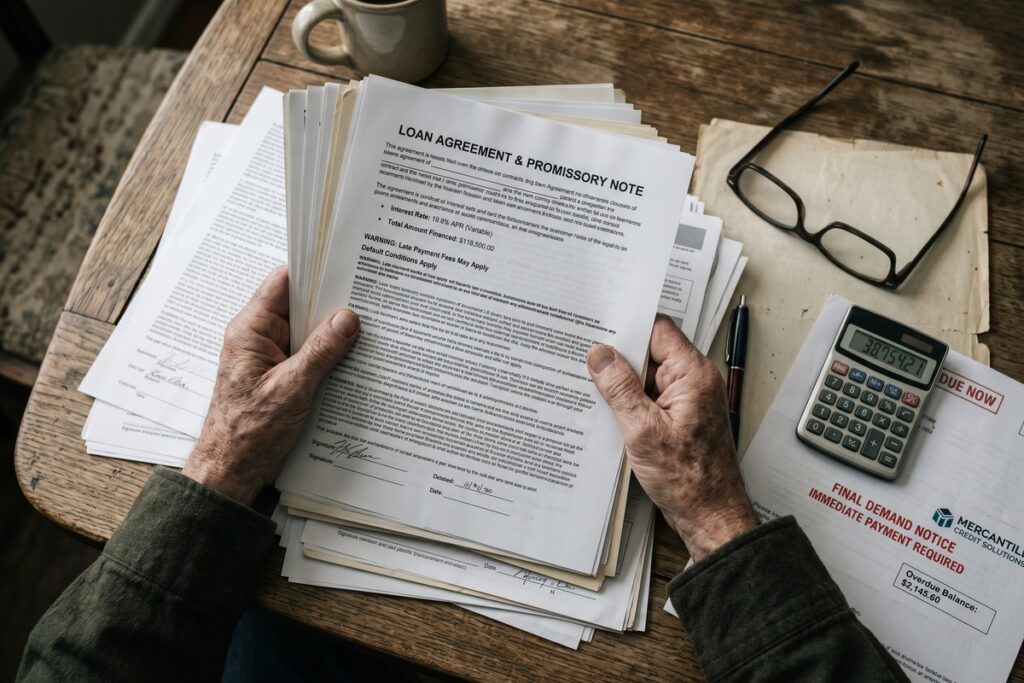

Picture a 74-year-old retired teacher who owns her home outright, lives on a fixed Social Security income, and receives a mailer promising to convert the equity in her house into cash for home repairs she genuinely needs. The loan documents are dense, the salesperson is warm and reassuring, and she signs at her kitchen table without knowing the interest rate will reset in two years or that a balloon payment is buried on page eleven. This is not a hypothetical. Predatory lending targeting seniors follows this pattern with disturbing consistency, and the people running these schemes are not operating blindly. They use commercially available databases sorted by age, homeownership status, and gender to identify exactly who is equity-rich and cash-constrained.

The scale of what older adults lose to financial exploitation is staggering. According to a December 2024 interagency statement issued jointly by the Federal Reserve, CFPB, FDIC, FinCEN, NCUA, OCC, and state financial regulators, estimated annual losses from elder financial exploitation reach $28.3 billion. When accounting for the severe underreporting that characterizes this crime, the FTC has estimated 2024 losses to adults 60 and older could be as high as $81.5 billion. Three separate federal-level datasets all point in the same direction: this crisis is large, growing, and poorly contained by the current legal framework.

By the end of this guide, you will be able to identify the specific schemes predatory lenders use against older adults, understand which federal laws offer protection and where those laws genuinely fall short, recognize the red flags before signing anything, and know exactly where to report abuse if it happens to you or someone you care for.

Key Takeaways

- Adults 60 and older reported $4.885 billion in losses to the FBI’s IC3 in 2024 across 147,127 complaints, a 43% increase in losses from the prior year.

- Elder financial exploitation causes an estimated $28.3 billion in annual losses, according to data cited in the December 2024 federal interagency statement on elder financial exploitation.

- No federal consumer protection or fair lending law contains provisions specific to elderly borrowers, meaning age-targeted predatory lending must be prosecuted under general consumer fraud statutes.

- The CFPB’s 2025–2026 rollback of ECOA fair lending enforcement has weakened practical recourse for older adults facing discriminatory loan terms.

- The surviving-spouse reverse mortgage trap is a documented scheme in which lenders encourage listing only the older spouse to maximize loan amounts, leaving the younger partner exposed to forced sale after the named borrower’s death.

- Severe underreporting means the true scale of elder financial exploitation is unknown; seniors often stay silent due to shame, fear of losing financial autonomy, or not knowing which agency to contact.

In This Guide

- Why Seniors Are the Primary Target

- The Scale of the Problem

- The Most Common Predatory Schemes

- Red Flags Every Senior and Family Should Know

- Federal Laws That Protect Seniors, and Where They Fall Short

- Reverse Mortgages: Legitimate Product, Real Risks, Active Fraud

- Why Seniors Don’t Report, and Why That Matters

- How to Report, Recover, and Get Help

Why Seniors Are the Primary Target

Predatory lenders do not target seniors by accident. They work from a calculated financial profile. Many older Americans own their homes free and clear after decades of mortgage payments, which means they carry substantial home equity. At the same time, a large share live on fixed incomes, Social Security, a pension, or modest retirement savings, that leave little cushion for emergency expenses. That combination of asset wealth and income vulnerability is exactly what certain lenders are looking for.

Unscrupulous lenders have been documented using commercially available consumer databases to sort potential targets by age, homeownership status, and gender. The resulting mailing lists are then flooded with offers for home equity loans, reverse mortgages, and refinancing products. This is a business practice, not random chance. Seniors with paid-off homes and modest monthly income represent the highest-margin opportunity for a lender whose profit depends on fees rather than long-term borrower health.

Physical and Cognitive Factors That Compound the Risk

Physical limitations reduce a senior’s ability to shop for better terms. If driving is difficult or internet access is limited, the loan offer that arrives by mail or through a contractor’s referral may feel like the only option. Cognitive decline, which exists on a spectrum and does not require a formal diagnosis to affect financial decision-making, makes dense loan documents harder to scrutinize. Hearing or vision impairments can make it difficult to catch misrepresentations during an in-person pitch.

None of these vulnerabilities reflect a lack of intelligence. They are circumstances that bad actors deliberately seek out and exploit.

The U.S. Government Accountability Office identified greater home equity, a higher likelihood of needing home repairs, and potential cognitive or physical impairments as key vulnerability factors that make seniors disproportionately attractive to predatory lenders. These are structural conditions, not personal failings.

The GAO’s review of federal consumer protection and fair lending laws found that elderly people have disproportionately been victims of predatory lending, even though no federal statute specifically addresses age-targeted lending as a distinct offense. That gap between documented harm and legal remedy runs through every part of this problem.

The Scale of the Problem

Numbers alone do not capture the full picture here, but they are still worth sitting with. The FBI’s Internet Crime Complaint Center (IC3) reported that adults age 60 and older submitted 147,127 complaints in 2024, representing total losses of $4.885 billion. That is a 43% increase in reported dollar losses and a 46% increase in complaint volume from 2023. And that figure only captures cases that were reported. Experts across federal agencies agree that elder financial fraud is among the most underreported crimes in the country.

The interagency estimate of $28.3 billion in annual elder financial exploitation losses comes from an entirely separate tracking mechanism: Bank Secrecy Act filings by financial institutions. That means it captures different activity than the IC3 data. Both figures are real. They are measuring different slices of the same crisis.

Large-Loss Cases Are Driving the Totals

The most financially damaging cases disproportionately involve real estate and lending fraud, where a single transaction can strip a homeowner of equity built over thirty years. Cases involving losses over $100,000 now drive the majority of aggregate dollar losses across elder fraud categories. A senior who loses $200,000 in home equity to a predatory refinancing scheme may not appear in FBI statistics at all if they did not file a complaint, and many do not.

Adults age 60 and older reported $4.885 billion in losses to the FBI’s IC3 in 2024 across 147,127 complaints, a 43% increase in losses from 2023. When accounting for underreporting, the FTC estimates 2024 losses to this age group could have reached as high as $81.5 billion.

The Most Common Predatory Schemes

The variety of schemes targeting older borrowers is wide, but a few patterns show up consistently across regulatory enforcement actions and advocacy reports. Understanding them as structured schemes, not isolated incidents, changes how you recognize them.

Home Equity Stripping and Loan Flipping

Home equity stripping refers to lending practices that bleed the accumulated value out of a homeowner’s property through high fees, unfavorable terms, or repeated refinancing. Loan flipping is a specific variation: a lender encourages a senior to refinance repeatedly, generating a new round of origination fees and closing costs each time, with no meaningful benefit to the borrower. After two or three flips, the equity cushion has been substantially consumed by fees while the borrower’s debt has grown.

Balloon-payment loans are a related tool. A senior may be offered manageable monthly payments for several years, only to face a large lump-sum payment at the end of the term that they have no way to meet. The lender then positions a new refinancing as the “solution,” continuing the cycle. If you want to understand what to look for before signing any short-term credit product, our guide on how to compare short-term loan offers without being misled by low APR claims covers the structural red flags that apply across product types.

The Contractor-Lender Kickback Scheme

This two-step fraud is rarely named as a distinct pattern in mainstream coverage, but it deserves to be. A home repair contractor, often reaching out unsolicited after a storm or responding to a general inquiry, identifies a senior homeowner who needs legitimate work done. The contractor then steers the homeowner to a specific lender, not because the loan is competitive, but because the contractor receives a referral commission for doing so. The senior ends up with an inflated repair contract financed by a high-cost loan, and both the contractor and lender profit at their expense.

The contractor serves as the first point of contact and the mechanism of trust. Recognizing that any contractor who introduces a specific lender or handles financing paperwork on your behalf is a potential red flag is the first line of defense against this scheme.

If a home repair contractor offers to arrange financing or recommends a specific lender, treat that as an immediate warning sign. Contractors who steer clients to lenders in exchange for commissions are participants in a documented two-step fraud scheme. Always seek financing independently from a lender you identify yourself.

Reverse Mortgage Fraud and Misrepresentation

Reverse mortgage fraud operates both within and alongside the legitimate product framework. Fraudsters may pose as HUD-approved counselors, use government-style seals in their marketing, or claim that a reverse mortgage is a government benefit rather than a loan. The consequences are severe: seniors who take lump-sum reverse mortgages based on inflated appraisals or misrepresented terms can face foreclosure when they cannot meet the property tax and insurance obligations that legitimate reverse mortgages require. This topic deserves its own section, which follows later in this guide.

Red Flags Every Senior and Family Should Know

The warning signs of predatory lending fall into two categories: behavioral signals from the lender or salesperson, and structural features buried in the loan terms themselves. Both matter.

Behavioral Warning Signs

Pressure to sign quickly is the most reliable behavioral red flag. A lender who insists that an offer expires today, or who arrives at your home and expects to leave with a signature, is not acting in your interest. Legitimate lenders give borrowers time to review documents. Refusal to provide sample documents before a closing appointment is another signal worth noting; reputable lenders have no reason to withhold standard paperwork.

Promises to “refinance later at better terms” should be treated with skepticism. If the terms offered now are not acceptable, a promise about future terms is not a commitment, and it creates the conditions for the loan-flipping cycle described above. Blank spaces left in documents are also a documented tactic; they allow terms to be altered after the borrower has signed.

Structural Loan Red Flags

- Adjustable interest rates with no downward floor (rate can rise without limit)

- Balloon payments due at the end of a seemingly affordable payment schedule

- Prepayment penalties that make it expensive to exit the loan early

- Credit insurance or other add-on products bundled into the loan without explicit, informed consent

- Origination fees or points that significantly exceed local market norms

- Negative amortization, where monthly payments do not cover the interest accruing

If you are helping a parent or older relative review a loan offer and want to know how to spot a lender that may not be legitimate in the first place, the guide on how to spot a fake loan company before you apply covers the pre-application warning signs that apply regardless of the borrower’s age.

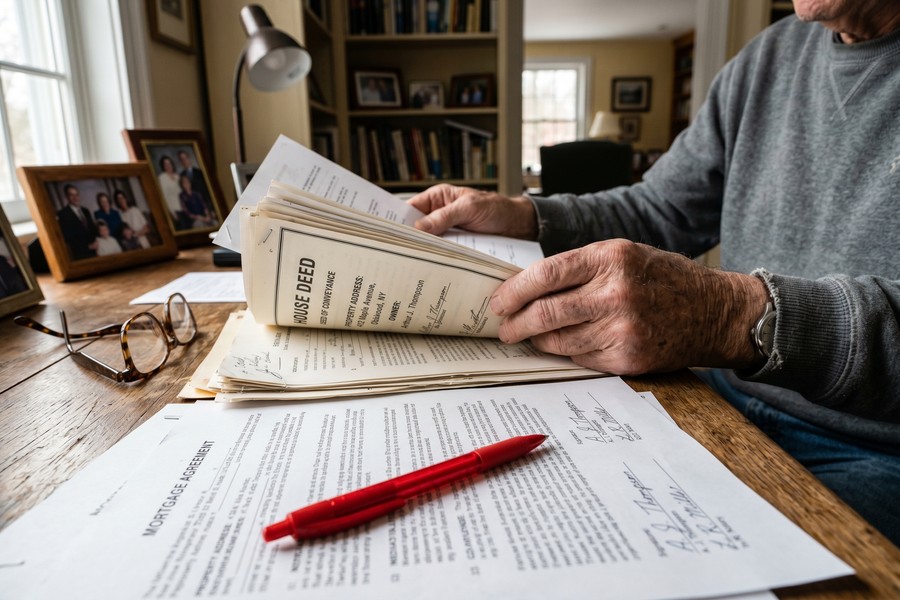

Before signing any loan document, request a complete copy at least three business days in advance. Federal law requires lenders to provide a Loan Estimate within three days of application for most mortgage products. If a lender resists this, that resistance is itself a red flag worth taking seriously.

Federal Laws That Protect Seniors, and Where They Fall Short

Several federal statutes form the backbone of consumer protection in lending. Understanding what they actually cover, and what they do not, is essential, because the gap between what the law promises and what it delivers for older adults is real and significant.

The Core Legal Framework

| Law | What It Covers | Key Limitation for Seniors |

|---|---|---|

| Truth in Lending Act (TILA) | Requires disclosure of APR, total cost of credit, and payment schedules | Disclosure only; does not prohibit unfair terms |

| Home Ownership and Equity Protection Act (HOEPA) | Sets limits on high-cost mortgage fees and restricts certain loan features | Applies to a narrow category of high-cost loans; many predatory products fall below the threshold |

| Equal Credit Opportunity Act (ECOA) | Prohibits lending discrimination based on age, among other characteristics | Enforcement significantly weakened by CFPB rollbacks in 2025 |

| Fair Debt Collection Practices Act (FDCPA) | Restricts abusive debt collection behavior | Applies after default, not at the point of origination |

| Senior Safe Act (2018) | Allows bank employees to report suspected elder financial exploitation without liability | Voluntary training; does not mandate reporting or delay suspicious transactions |

The Critical Protection Gap

Here is the honest assessment that most coverage of this topic avoids: the GAO found that existing federal consumer protection and fair lending laws do not generally contain provisions specific to elderly borrowers. A senior who was targeted precisely because of their age, their home equity, and their cognitive vulnerability must be protected under the same general consumer fraud statutes that apply to any adult borrower. There is no federal law that makes age-targeted predatory lending a distinct and separately prosecutable offense.

That gap has grown more consequential in the current environment. The CFPB’s rollback of ECOA fair lending enforcement provisions in 2025–2026 reduced the practical toolkit available to older adults seeking recourse for discriminatory loan terms. The agency that was most active in prosecuting lending discrimination has pulled back from a key enforcement posture, and that change has real consequences for people who were targeted because of who they are.

The GAO has also been direct about the limits of what consumer education alone can accomplish. Its review concluded that consumer education by itself has limits as a tool for deterring predatory lending. That is an important concession. Guides like this one are genuinely useful, but they are not sufficient. The structural and legal conditions that allow predatory lending to persist require regulatory responses that education cannot substitute for.

Understanding your right to dispute a loan after signing is a separate but related protection. Our overview of what most borrowers get wrong about their right to dispute a loan explains the procedural options that exist under current law regardless of lender behavior.

The AARP Legal Counsel for the Elderly provides direct legal representation to senior clients on predatory lending and real property fraud. They have litigated key cases for over two decades with the goal of protecting clients’ homes and sources of income, one of the few legal resources specifically designed for this population.

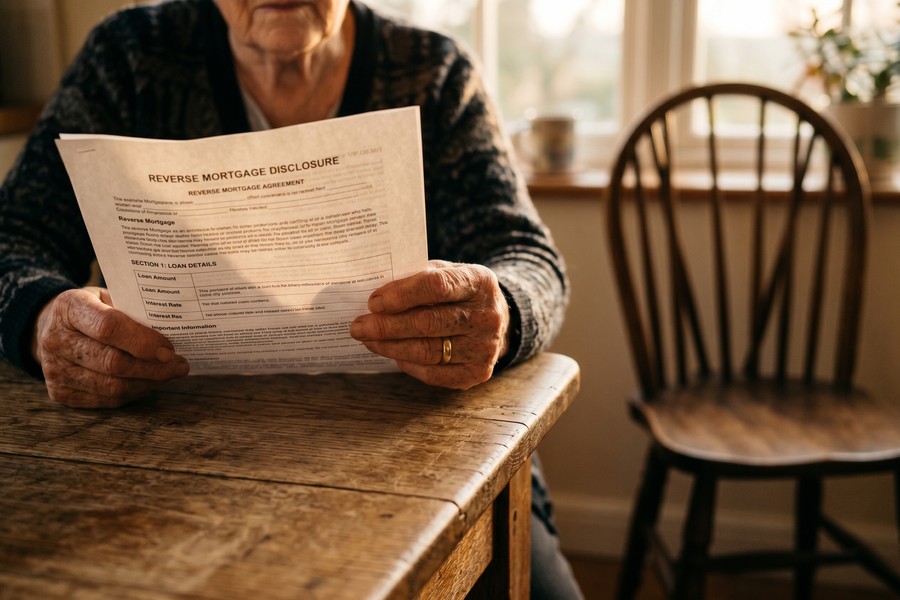

Reverse Mortgages: Legitimate Product, Real Risks, Active Fraud

A Home Equity Conversion Mortgage (HECM) is a federally insured reverse mortgage product backed by the FHA. When structured properly, it allows older homeowners to convert home equity into income without making monthly mortgage payments. The product is real, legal, and can be appropriate in specific circumstances. The problem is that it is also being actively weaponized by fraudsters, and even a fully compliant HECM carries risks that the marketing materials rarely acknowledge honestly.

What the Legitimate Product Actually Requires

Federally insured HECMs require the borrower to receive independent counseling from a HUD-approved counselor before the loan closes. The property must be appraised by an FHA-assigned appraiser. Lenders must conduct a financial assessment to evaluate the borrower’s ability to pay ongoing property taxes and insurance. Borrowers have a three-day right of rescission after closing. These protections exist and they matter, but they can still be undermined by bad-faith actors who coach borrowers through counseling sessions or use inflated appraisals.

The honest concession about even compliant products: over ten years, the interest and fees on a lump-sum HECM can exceed $100,000. Residency requirements mean that if a borrower’s health requires a move to assisted living, the loan becomes due and the home may need to be sold. These are not fraud scenarios. They are the predictable, disclosed consequences of a product that is often sold without adequate emphasis on its long-term cost structure.

The Surviving-Spouse Trap

This is the reverse mortgage risk that most coverage omits entirely, and it deserves direct attention. Lenders sometimes encourage couples to list only the older spouse on a reverse mortgage, because a higher age produces a larger loan amount. The younger spouse is left off the loan documents. When the named borrower dies or moves to a care facility, the loan becomes due. The surviving spouse, who was not on the loan, can face forced sale of the home they have lived in for decades.

HUD issued regulations in 2014 and 2021 that extended certain protections to non-borrowing spouses, but those protections have conditions and do not apply in all scenarios. The safest course is for both spouses to be listed as co-borrowers, even if that reduces the total loan amount. A smaller loan amount is a trade-off worth accepting.

Why Seniors Don’t Report, and Why That Matters

The underreporting of elder financial exploitation is not simply a measurement problem. It is a structural feature of this type of abuse, and understanding why it happens changes how families, banks, and policymakers should respond.

The Reasons Seniors Stay Silent

Shame is the most commonly cited reason. Many older adults feel they should have known better, particularly if they received a formal education or held professional careers. Admitting to financial victimization can feel like admitting a personal failure rather than recognizing that a professional scheme was deployed against them.

Fear of losing financial independence is a closely related barrier. A senior who reports fraud to Adult Protective Services may worry that the investigation will lead to questions about their capacity to manage their own finances, potentially triggering conservatorship discussions they did not invite. That fear is not irrational, and it keeps many victims silent.

A third factor is structural: many seniors genuinely do not know which agency handles which type of abuse. The FTC, CFPB, FBI, HUD-OIG, state attorneys general, and Adult Protective Services all have overlapping but distinct jurisdictions. Without knowing where to go, the path of least resistance is to do nothing. The section below maps each agency to the type of abuse it handles.

CFPB research shows elder financial exploitation survivors frequently experience fear, shame, anxiety, and depression in its aftermath. Financial recovery depends heavily on health status, the survivor’s relationship to the perpetrator, and how quickly the exploitation was reported. The harm compounds over time rather than resolving on its own.

How to Report, Recover, and Get Help

Knowing which agency handles which type of fraud is practical knowledge that significantly improves the outcome of a report. Filing with the wrong agency does not mean your complaint disappears, but it does slow the process.

Where to File a Report

- CFPB: For complaints against banks, mortgage servicers, and other financial institutions. File at consumerfinance.gov/complaint.

- FTC: For deceptive marketing, deceptive mortgage advertising, and identity theft. Report at reportfraud.ftc.gov.

- HUD-OIG: For fraud specifically involving FHA-insured mortgages or reverse mortgage misrepresentation. Report at hudoig.gov.

- FBI IC3: For internet-based or wire fraud schemes. File at ic3.gov.

- State Adult Protective Services (APS): For exploitation by a caregiver, family member, or trusted individual who used their position to influence financial decisions.

- State Attorney General: For predatory lenders operating within the state, particularly for enforcement under state consumer protection statutes.

Filing reports with multiple agencies is not redundant. Different agencies have different legal tools, and a complaint that the CFPB cannot act on may be exactly what a state attorney general needs to pursue an enforcement action against a lender operating locally.

Institutional Safeguards Worth Knowing

The Senior Safe Act allows bank and credit union employees who complete qualifying training to report suspected elder financial exploitation to authorities without facing civil or criminal liability for the disclosure. This is a meaningful protection for financial institution employees who observe suspicious transactions. FINRA rules require brokerage firms to make reasonable efforts to obtain a trusted contact person for customers who are 65 or older, creating an additional check against exploitation of investment accounts.

For seniors carrying debt from an exploitative lending situation alongside other financial pressures, understanding the comparative legal protections across different debt types is useful. Our breakdown of medical debt versus personal loan debt legal protections explains where the law gives borrowers more and less leverage depending on what they owe. And if you have already discovered that a lender charged illegal fees, the account of how one borrower successfully recovered illegal lending fees walks through the specific dispute process that resulted in a full refund.

For checking a lender’s complaint history before engaging with them, the CFPB complaint database guide explains how to search the database for any lender’s track record with consumers, a step worth taking before any older adult signs a loan application.

Your Action Plan

-

Verify any lender independently before engaging

Before responding to any mailer, phone call, or contractor referral involving a loan, look up the lender in the CFPB complaint database and your state’s financial regulator license lookup. A legitimate lender will be licensed in your state and will have a traceable complaint history. Avoid any lender who cannot be verified through these channels.

-

Request all loan documents at least three days before signing

Federal law requires Loan Estimates for most mortgage products within three days of application. Insist on receiving the full closing disclosure at least three business days before any signing appointment. Read every page, or have a trusted family member, attorney, or HUD-approved housing counselor review it with you. Any lender who resists this request is not working in your interest.

-

Separate your home repair contractor from your financing

If you need home repairs, obtain contractor bids and financing offers independently. Never let a contractor arrange or recommend your lender. Seek financing through your own bank or credit union, a HUD-approved housing counselor, or a state housing finance agency. The contractor-lender kickback scheme begins with allowing these two roles to merge.

-

If considering a reverse mortgage, require both spouses to be named as co-borrowers

Even if naming a younger spouse reduces the loan amount, both partners should be listed as co-borrowers on any reverse mortgage. Consult independently with a HUD-approved HECM counselor, not one referred by the lender, before agreeing to any terms. Understand the full cost projection over ten years, including compounding interest and fees.

-

Designate a trusted contact with your financial institutions

Ask your bank, credit union, and any brokerage accounts to add a trusted contact person to your file. This is different from a power of attorney. It gives the institution someone to contact if they observe suspicious activity, without giving that person authority over your accounts. FINRA requires brokerages to ask for this information; your bank can add it voluntarily.

-

Know which agency to call before you need to call one

Write down the relevant contacts now: CFPB (consumerfinance.gov/complaint), FTC (reportfraud.ftc.gov), your state attorney general’s consumer protection office, your state Adult Protective Services hotline, and HUD-OIG (hudoig.gov). Store them where a family member can also find them. Delayed reporting significantly reduces the chance of financial recovery.

-

Consider a consultation with a legal aid attorney before signing any high-cost loan

AARP Legal Counsel for the Elderly provides direct representation to seniors in predatory lending and real property fraud cases. Many states also have legal aid organizations with elder law units that provide free consultations. A one-hour legal review before signing costs nothing and could prevent losses that take years to litigate.

Frequently Asked Questions

What makes a loan “predatory” rather than just expensive?

A predatory loan is not simply one with a high interest rate. Predatory lending involves a combination of unfair, deceptive, or abusive practices: misrepresenting loan terms, targeting borrowers who cannot realistically repay, structuring loans in ways that strip equity through fees, or using high-pressure tactics to prevent comparison shopping. Cost alone does not define predatory; the combination of cost, intent, and targeting does.

Are reverse mortgages inherently predatory?

No. A federally insured HECM, structured properly and entered into with full information, is a legal product that can be appropriate for some homeowners. The concern is twofold: legitimate products are frequently misrepresented by bad actors, and even compliant reverse mortgages carry significant long-term costs and risks that marketing materials routinely underemphasize. An informed decision is possible; an uninformed one is dangerous.

Does Medicare or Social Security income factor into predatory lending risk?

Yes, in a specific way. Federal law generally protects certain federal benefit payments, including Social Security and SSI, from garnishment by most creditors. However, once those funds are deposited into a bank account and commingled with other money, the protection becomes harder to enforce. Predatory lenders may not be deterred by this protection if they can use other collection mechanisms, such as placing liens on property.

What is the three-day right of rescission, and does it apply to all loans?

The right of rescission under the Truth in Lending Act allows borrowers three business days to cancel certain types of loans secured by their primary residence, this includes home equity loans and refinancing with a new lender, but it does not apply to purchase mortgages. If you sign and then realize the terms were misrepresented, the rescission period gives you a window to walk away without penalty. Use it if something feels wrong after signing.

Can a family member report elder financial exploitation on behalf of a senior?

Yes. Adult Protective Services accepts reports from family members, neighbors, or any person who suspects exploitation. The CFPB and FTC also accept third-party complaints. If a senior is unwilling to report due to shame or fear, a family member can initiate the process. That said, APS investigations are independent, and the agency’s response will depend on its own assessment of the situation.

What does the CFPB rollback actually mean for seniors in practice?

The CFPB’s 2025–2026 reduction in ECOA fair lending enforcement means the agency is less actively pursuing cases where lenders discriminate based on demographic characteristics, including age. In practice, this reduces the chance that a complaint about age-targeted predatory lending will result in a formal enforcement action against the lender. State attorneys general and private litigation become more important as federal enforcement pulls back. This is a real change, not a theoretical one.

How do I check if a lender is licensed in my state?

Most states require mortgage lenders and loan brokers to hold a state license, which is searchable through the Nationwide Multistate Licensing System (NMLS) consumer access portal at nmlsconsumeraccess.org. You can search by company name or individual loan officer name to verify licensing status. A lender who cannot be found in this database should not be trusted with a mortgage application.

Is the contractor-lender kickback scheme illegal?

Kickback arrangements between contractors and lenders for mortgage referrals are prohibited under the Real Estate Settlement Procedures Act (RESPA) when they involve federally related mortgage loans. However, enforcement requires someone to report it, investigate it, and prosecute it, a process that takes time and often requires evidence that is difficult for individual borrowers to gather. Prevention, by keeping contractors and lenders completely separate, is more reliable than relying on after-the-fact enforcement.

What happens if a predatory lender goes out of business after I’ve been victimized?

The loan obligation typically does not disappear, it is sold or transferred to another servicer or debt collector. If the lender’s conduct was fraudulent, you may have claims against individual principals even if the company has dissolved. Filing complaints with state regulators and consulting with a consumer attorney quickly is important in this scenario, because time limits (statutes of limitations) apply to legal claims. For context on how loan agreements behave when a lender exits the market, our guide on what happens to your loan agreement when a lender goes bankrupt explains borrower rights in that situation.

Are there specific financial products seniors should avoid entirely?

No product is universally off-limits, but certain products carry elevated risk for older borrowers on fixed incomes: adjustable-rate mortgages with no rate floor, interest-only loans, balloon-payment structures, and any loan that requires liquidating retirement assets to service the debt. The FTC’s guidance on mortgage products for older homeowners outlines which product features warrant the most scrutiny.

Before any older adult signs a loan secured by their home, a one-time consultation with a HUD-approved housing counselor is free and carries no obligation. Find one at the HUD counselor locator at hud.gov. This single step has prevented more predatory loans than any after-the-fact legal remedy.

Sources

- NCUA / Federal Interagency, December 2024 Interagency Statement on Elder Financial Exploitation

- FBI Boston Division, FBI Highlights Growing Number of Reported Elder Fraud Cases (2025)

- U.S. Government Accountability Office, GAO Report GAO-04-280: Consumer Protection and Fair Lending Laws Used to Address Predatory Lending

- Consumer Financial Protection Bureau, Reporting Suspected Elder Financial Exploitation: Update to 2016 Advisory and Recommendations

- Federal Trade Commission, Business Guidance on Mortgages and Consumer Protection

- AARP Legal Counsel for the Elderly, Consumer Fraud and Financial Abuse

- Woodstock Community Policy Institute, Senate Committee Hears Testimony on Predatory Lending (David Wood, GAO)

- Consumer Financial Protection Bureau, Reverse Mortgages Consumer Information

- Federal Trade Commission, Mortgages and Consumer Lending Protections